30/07/2017

For anyone involved in the taxi industry in the United Kingdom, understanding the financial intricacies of licensing and operational costs is paramount. Whether you're a seasoned driver, a new entrant, or considering selling your taxi license, navigating the associated financial and regulatory landscape can be complex. This article aims to shed light on these critical aspects, covering everything from the tax implications of selling a license to the components that make up a typical taxi fare. While specific financial figures and city examples provided herein are drawn from the Spanish context for illustrative purposes, the underlying principles of taxation, asset valuation, and fare calculation offer valuable insights applicable to the broader taxi industry, including the UK.

A taxi license is far more than just a piece of paper; it represents a fundamental permission granted by a local authority, such as a council in the UK, allowing an individual to legally operate a taxi service within a specified area. This license is indispensable for offering transport services to passengers. The sale of such a license, while potentially lucrative, is an operation with significant financial implications that must be thoroughly understood, particularly concerning taxation.

Understanding the Sale of a Taxi License: Tax Implications

When a taxi license is sold, it is typically considered a capital asset, and its sale often triggers tax obligations. While specific tax laws vary significantly by country and even within regions, the general principle involves taxing the gain made from the sale. In the context of the information provided, which details the Spanish tax system, the sale of a taxi license is subject to Personal Income Tax (IRPF) and Value Added Tax (IVA). It’s crucial for UK operators to understand that their specific tax liabilities would fall under His Majesty's Revenue and Customs (HMRC) regulations, which may include Capital Gains Tax and VAT, depending on their individual circumstances and business structure.

For illustrative purposes, let's delve into the Spanish tax framework as described in the source material. In Spain, the amount payable to the tax authorities on the sale of a taxi license depends on various factors, such as the license's age and its sale price. This highlights a universal truth: the specifics of taxation are highly dependent on local regulations.

Personal Income Tax (IRPF) in Spain

In Spain, the seller of a taxi license must declare the capital gain obtained from its sale for IRPF purposes. This capital gain is calculated by subtracting the acquisition value of the license from its sale price. The resulting gain is then taxed under the savings tax base of the IRPF. The tax rates applied increase progressively with the amount of the gain. This concept of taxing capital gains is common across many jurisdictions, including the UK, though the specific rates and thresholds will differ.

Below is an example of the IRPF tax rates on capital gains in Spain, as provided:

| Capital Gain (Euros) | Tax Rate |

|---|---|

| Up to 6,000 | 19% |

| Between 6,000 and 50,000 | 21% |

| Between 50,000 and 200,000 | 23% |

| Between 200,000 and 600,000 | 24% |

| Between 600,000 and 1,000,000 | 25% |

| Between 1,000,000 and 2,000,000 | 26% |

| Above 2,000,000 | 27% |

It is important to reiterate that these are Spanish tax rates. In the UK, Capital Gains Tax rates vary depending on the asset and the taxpayer's income bracket, often being 10% or 20% for most assets for basic and higher rate taxpayers respectively, with different rates for residential property.

Value Added Tax (IVA) in Spain

In Spain, the sale of a taxi license is also subject to Value Added Tax (IVA), with a general rate of 21% mentioned in one part of the text, and a reduced rate of 10% in another, specifically for entrepreneurs or professionals engaged in economic activity. This discrepancy highlights the complexity and potential for different interpretations or specific conditions within a tax system. For UK taxi operators, VAT implications on the sale of business assets would depend on whether they are VAT registered and the specific nature of the asset being sold.

Municipal Capital Gains Tax (Plusvalía Municipal) in Spain

Another tax mentioned in the Spanish context is the "Plusvalía Municipal," which taxes the increase in value of the land where the taxi license is located. Its calculation depends on municipal regulations and the license's age. This is a highly localised tax, and while UK councils may levy various fees, a direct equivalent taxing the land value associated with a taxi license in this manner is not standard.

Calculating Taxes on Sale (Spanish Example)

To calculate the taxes payable on the sale of a taxi license in Spain, the following steps are generally outlined:

- Determine the sale price of the taxi license.

- Subtract the acquisition value (original cost) from the sale price to find the profit.

- Apply the corresponding IRPF tax rate to the profit.

- Calculate the IVA (VAT) on the sale price of the license.

- Calculate the Plusvalía Municipal according to local municipal regulations.

- Sum all calculated taxes to get the total amount payable.

For UK individuals considering selling a taxi license, it is paramount to consult with a qualified accountant or tax advisor who specialises in UK tax law to understand their specific obligations regarding Capital Gains Tax, VAT, and any other relevant local taxes or fees.

Exceptions and Reductions in Spain

The Spanish tax system also allows for certain exceptions and reductions. For instance, if the seller is an individual and has owned the license for at least 3 years, a 15% reduction in IRPF might apply. For legal entities, a 5% reduction in corporate tax might be applicable if the license has been owned for at least 1 year. Furthermore, if a license was obtained through inheritance or donation, the inheritance/donation tax (ITP) might not apply. Some Spanish autonomous communities may also offer deductions for licenses adapted for disabled persons or those using electric/less polluting vehicles. These examples underscore the complexity and nuance of tax legislation, which makes professional advice indispensable.

Consequences of Non-Payment

Regardless of the country, failing to meet tax obligations has serious consequences. In Spain, as detailed, these can include:

- Surcharges and Interest: Late payments incur additional charges.

- Fines: Non-declaration or non-payment can lead to significant penalties, ranging from 50% to 150% of the amount owed.

- Asset Seizure: The tax authority may initiate procedures to seize assets to recover the outstanding amount.

- Legal Problems: Non-payment can escalate to criminal charges for tax evasion.

These consequences are broadly similar in the UK, where HMRC has significant powers to impose penalties, charge interest, and pursue legal action for unpaid taxes. This highlights the universal importance of compliance and seeking expert advice to ensure all obligations are met.

Strategies to Potentially Minimise Tax (General Principles)

While specific strategies depend heavily on local tax laws, the general idea of tax planning is to legally minimise one's tax burden. The Spanish text mentions a few interesting concepts:

- Selling the License in Parts: Suggesting separating components like the vehicle, the permit, and the operating right to sell them separately. This is a complex strategy and would require careful consideration of how each component is valued and taxed in the UK.

- Reinvestment Exemption (Spanish Example): Using an exemption for reinvestment in a primary residence. In Spain, if a new primary residence is purchased within two years of selling the license, it might be possible to avoid tax on the gain. The UK has its own rules regarding capital gains relief, such as Principal Private Residence Relief, but these do not typically apply to business asset sales unless the asset is directly linked to the residence in specific ways.

- Advance Planning: Consulting with a tax advisor well in advance of the sale is crucial. This allows for strategic planning to minimise tax liabilities within legal frameworks. This principle is universally applicable and highly recommended for UK taxi operators.

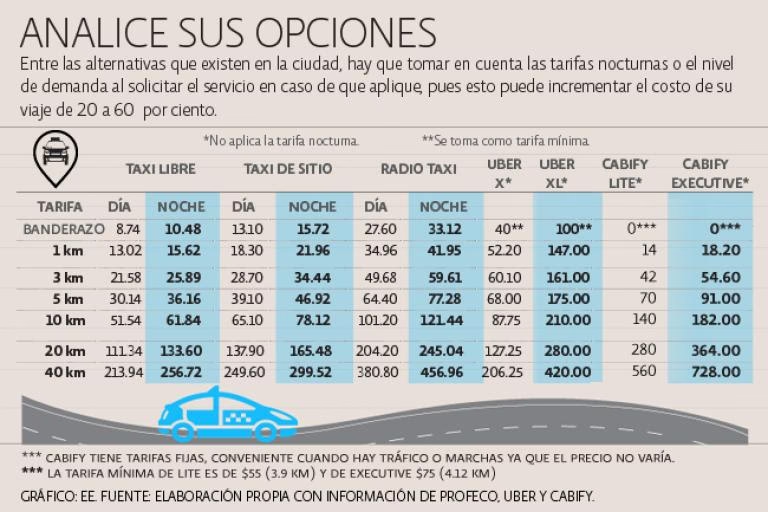

Understanding Taxi Fares in the UK

Beyond licensing, the daily operation of a taxi business revolves around fares. Taxi fares in the UK, like in Spain, are regulated by local authorities and consist of several components. While the specific rates and structures differ from city to city, the underlying elements are largely consistent. The provided information offers a detailed look at how fares are structured in Spain, which provides a valuable conceptual framework.

Una empresa de taxis tiene la siguiente tarifa: un costo fijo de S/. 2 más S/. 1.5 por cada kilómetro recorrido. ¿Cuál es la representación gráfica de esa tarifa? ¿Cuánto se pagará por un recorrido de 20 km? Components of a Taxi Fare (Spanish Examples)

In Spain, a taxi fare typically combines three main concepts:

- Kilometres (Distance): A charge per kilometre travelled. The cost per kilometre varies significantly between cities. For instance, in Spain, cities like Santa Cruz de Tenerife (0.54 euros/km) and Las Palmas de Gran Canaria (0.60 euros/km) are among the cheapest, while Tarragona (1.04 euros/km) and Castellón (1.02 euros/km) are among the most expensive. In the UK, each council sets its own maximum fares per mile or kilometre.

- Time (Waiting/Slow Travel): A charge for the time the taxi is stationary (e.g., at traffic lights, in congestion) or moving very slowly. This compensates the driver for their time when not covering distance efficiently. Spanish examples show Las Palmas (11 euros/hour) and Santa Cruz de Tenerife (11.5 euros/hour) as cheapest for waiting time, with Orense (21 euros/hour) and Gijón (20.82 euros/hour) being among the most expensive. UK taxi meters also typically incorporate a time element, particularly when the vehicle is stationary or moving below a certain speed.

- Minimum Fare (Flag Drop/"Bajada de Bandera"): A fixed charge applied simply for getting into the taxi, regardless of the distance or time. This is often referred to as the "flag drop" in the UK. Spanish examples indicate Las Palmas (1.65 euros) as having the cheapest minimum fare, while San Sebastián (4.93 euros) has one of the most expensive. In the UK, minimum fares are standard and vary by council.

Night and Holiday Rates

It's common for taxi fares to be higher during specific times, such as late nights or public holidays, to compensate drivers for working unsocial hours. In Spain, the source material indicates that taking a taxi late at night on a public holiday can be 33% more expensive than a daytime weekday fare. Málaga is cited as a special case where a night-time journey can be 60% more expensive than a daytime equivalent. Similar surcharges for night-time, weekend, or holiday travel are also common practice across the UK, reflecting higher demand and operational costs.

Fare Increases and Local Variations

Taxi fares are not static and are subject to periodic increases, often due to rising fuel costs, inflation, or operational expenses. The provided text notes that in Spain, daytime fares increased by 2.5% and night-time fares by 2% in the preceding year. It also highlights specific instances like Madrid's fare increase, including a new supplement for phone bookings. While UK fare increases are also common, the specific percentages and introduction of new supplements would be determined by local licensing authorities.

For a conceptual understanding, here’s an example of how a typical fare calculation might be presented, using the Spanish context as provided:

City (Spain) Daytime Fare (3km, 5min wait) Night/Holiday Fare (3km, 5min wait) Madrid 6.78 euros 8.53 euros (Figures based on provided text, subject to change) This table is illustrative of how such information might be presented for any city, with the understanding that UK specific figures would need to be obtained from relevant local council websites or taxi associations.

Important Considerations for UK Taxi Operators

While the detailed financial figures in this article pertain to Spain, the overarching message for UK taxi operators is clear: financial literacy and professional guidance are essential. Understanding your local council's licensing requirements, fees, and fare structures is critical for daily operations. When it comes to significant transactions like selling a taxi license, the complexity of tax law necessitates consulting with UK-based tax advisors or accountants. They can provide tailored advice on Capital Gains Tax, VAT, and any other relevant UK taxes, ensuring compliance and helping to navigate potential tax liabilities effectively.

Frequently Asked Questions (FAQs)

Q: What is a taxi license?

A: A taxi license is a permit granted by a local authority that allows an individual to legally operate a taxi service within a specific area. It's essential for providing passenger transport services.Q: Is selling a taxi license a taxable event?

A: Yes, in many jurisdictions, including the UK and Spain, selling a taxi license is considered a taxable event. The profit made from the sale (capital gain) is typically subject to taxation, such as Capital Gains Tax in the UK or IRPF in Spain.Q: Why do taxi fares vary between cities?

A: Taxi fares vary due to different local regulations, operating costs (like fuel, vehicle maintenance, insurance), local demand, and economic conditions in each city. Local councils set maximum fare tariffs, leading to these variations.Q: What happens if I don't pay the taxes on selling my taxi license?

A: Failing to pay taxes on time can lead to severe consequences, including surcharges, interest, significant fines, and potentially legal action or asset seizure by tax authorities. It is crucial to comply with all tax obligations.Q: Is the tax and fare information in this article applicable to the UK?

A: The general principles regarding licensing, selling assets, and fare components are universal. However, the specific tax rates (like IRPF, IVA, Plusvalía) and precise fare amounts/city examples detailed in this article are based on information from Spain. For UK-specific information, you must consult HMRC guidelines and your local council's taxi licensing department.Q: How can I minimise my tax burden when selling a taxi license in the UK?

A: To legally minimise your tax burden in the UK, it is highly recommended to consult with a qualified UK tax advisor or accountant. They can provide bespoke advice based on your individual circumstances, exploring options such as reliefs, allowances, and strategic planning.

If you want to read more articles similar to UK Taxi Business: Licensing & Fare Insights, you can visit the Taxis category.