09/09/2025

In an evolving automotive landscape, the traditional path of outright car ownership is no longer the sole, or even preferred, route for many UK motorists. A significant shift has occurred, with an increasing number of individuals and businesses exploring alternative avenues such as financing or leasing their new vehicles. This guide aims to cut through the complexity, offering a clear, comprehensive comparison to help you determine whether buying or leasing is the most advantageous option for your specific circumstances here in the United Kingdom.

- How Long Do You Intend to Keep Your Vehicle?

- Upfront Costs: Do You Have Readily Available Cash?

- The Ownership Question: Do You Prefer to 'Own' Your Car?

- Understanding Depreciation: A Silent Cost of Ownership

- Value for Money: What Truly Represents the Best for You?

- PCH vs. PCP: Unravelling the Popular Finance Options

- Making Your Informed Decision: Buying vs. Leasing

- Frequently Asked Questions About Car Leasing

How Long Do You Intend to Keep Your Vehicle?

One of the most crucial factors in deciding between purchasing and leasing a car hinges on your typical vehicle retention period. If you are someone who buys a new car with the intention of keeping it for its entire operational life, perhaps running it until it's no longer economically viable, then a traditional cash purchase or long-term finance agreement might indeed be the most sensible approach. This allows you to maximise the value derived from your initial investment over many years.

However, if your preference leans towards regularly upgrading to a newer model every few years, perhaps desiring a vehicle that consistently remains under the manufacturer's warranty for peace of mind and reduced maintenance worries, then leasing presents a far more compelling proposition. Most standard lease agreements, particularly Personal Contract Hire (PCH) deals, are structured over periods ranging typically from 24 to 48 months. This fixed term ensures you always have access to a modern vehicle equipped with the latest technology and safety features, without the commitment of long-term ownership. It also means you avoid the hassle of selling an older car, a process that can often be time-consuming and fraught with negotiation.

Upfront Costs: Do You Have Readily Available Cash?

Acquiring a brand-new car outright with cash represents a substantial financial outlay for most individuals and businesses. Even what might be considered an "entry-level" vehicle today commands a significant sum; for instance, a popular Ford Fiesta or Volkswagen Golf can easily cost upwards of £17,000 and £23,000 respectively. This immediate, lump-sum payment ties up a considerable amount of capital that could potentially be used for other investments or operational expenses.

Conversely, choosing to lease your vehicle significantly mitigates the burden of a large initial payment. The overall cost of the vehicle's usage is meticulously spread out over the duration of the lease term through manageable monthly payments. While there is almost always an upfront contribution required, known as an initial payment, this sum is considerably less than the full purchase price. This initial payment is typically calculated as a multiple of your monthly instalments, commonly 3, 6, or 9 months' worth, and its size can often be adjusted to suit your budget, though a larger initial payment will naturally result in lower subsequent monthly fees.

Consider this simplified comparison of initial outlays:

| Option | Typical Initial Outlay | Impact on Capital |

|---|---|---|

| Buying Outright | Full Purchase Price (e.g., £20,000+) | Significant immediate capital drain |

| Leasing (PCH) | 3-9 months of monthly payments (e.g., £500-£1,500) | Lower initial capital requirement, capital retained for other uses |

The Ownership Question: Do You Prefer to 'Own' Your Car?

A fundamental distinction that often sways potential buyers is the concept of ownership itself. It is paramount to understand that with a leasing agreement, you never truly 'own' the vehicle. Instead, it functions as a long-term hire agreement, where the car legally remains the property of the leasing company throughout the contract duration. At the end of the term, you simply return the vehicle.

For many, particularly those focused on the utility and functionality of a vehicle rather than its status as a personal asset, this distinction holds little importance. They value the convenience, predictability of costs, and the ability to regularly drive a new car more than the title of ownership. However, if the psychological or practical aspect of 'owning' your car – having full control, the ability to modify it freely, or view it as an appreciating (or at least tangible) asset – is important to you, then leasing might not align with your preferences. In such cases, exploring other financing options such as a traditional hire purchase (HP) agreement or a Personal Contract Purchase (PCP) might be more suitable, as these pathways can lead to eventual ownership.

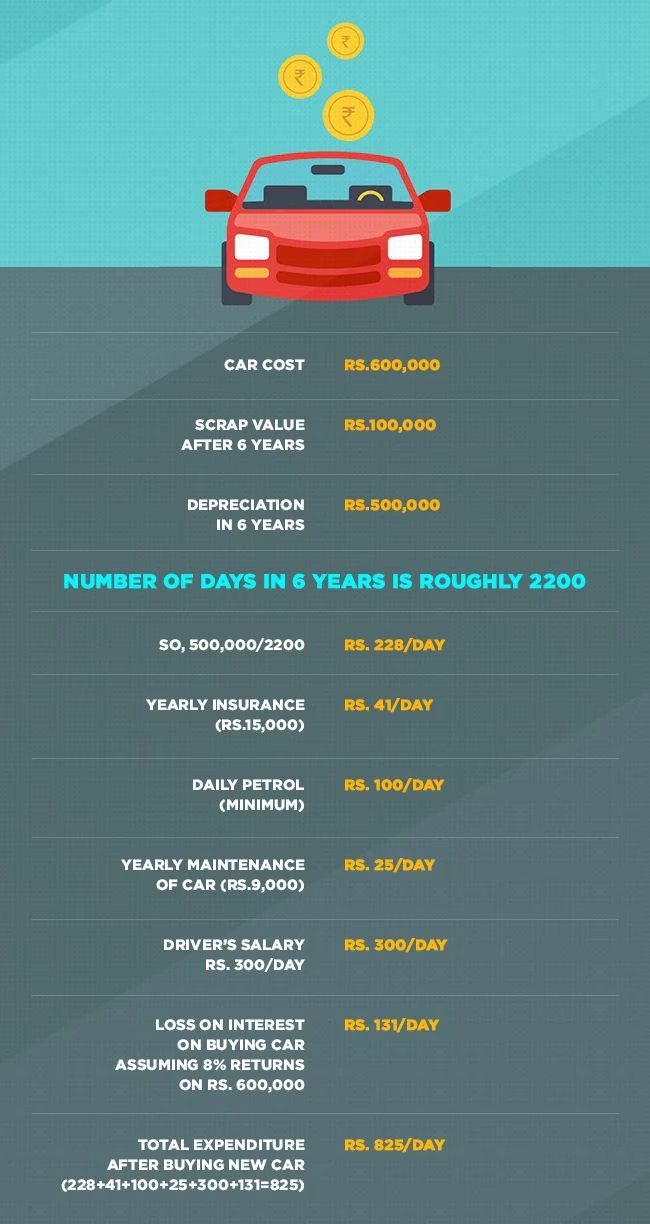

Understanding Depreciation: A Silent Cost of Ownership

When you opt to purchase a car outright, depreciation stands as one of the most significant, yet often overlooked, financial concerns. The moment a new car leaves the showroom, its value invariably begins to decline. This decline can be quite steep in the initial years, meaning that if you are someone who likes to change cars every few years, you could find yourself substantially out of pocket when it comes to selling or part-exchanging your previous vehicle. The difference between what you paid and what you sell it for is your depreciation cost, a real financial loss.

One of the most attractive benefits of leasing is that you are shielded from the impact of depreciation. The leasing company, as the legal owner, absorbs this financial risk. The monthly lease payments are fundamentally calculated based on the expected depreciation of the vehicle over the term of your contract, plus interest and fees. This means you are essentially paying for the portion of the car's value that it is projected to lose while you are driving it, rather than its full purchase price.

It's interesting to note that while depreciation affects all cars, you might observe that cars from more premium or luxury brands, which traditionally boast stronger residual values (their projected value at the end of a fixed term), are sometimes not significantly more expensive to lease on a monthly basis than certain mainstream models. This is precisely because their higher residual value means the leasing company anticipates a greater return on the vehicle when it is returned, enabling them to offer more competitive monthly rates to the consumer. This makes premium vehicles more accessible via leasing than outright purchase for many.

Value for Money: What Truly Represents the Best for You?

Defining "value for money" is inherently subjective and largely depends on your individual priorities and financial perspective. On paper, leasing often appears to be the more financially efficient option in terms of monthly outgoings, as you are only paying for the depreciation and usage, not the full capital cost. However, it is crucial to reiterate that leasing is not an investment in the traditional sense, as the vehicle never becomes your asset. You are paying for the privilege of using a new car, not building equity.

Nevertheless, if the concept of actual vehicle ownership is not a primary concern for you, and your main objective is to drive a new, reliable car every few years without the burden of large upfront costs, the risks of depreciation, or the hassle of selling, then leasing is unequivocally an incredibly affordable and convenient way to achieve this. It offers predictable budgeting and access to the latest models without the long-term commitment of ownership.

Conversely, for those who value having a tangible asset, even a depreciating one, and who plan to keep their vehicle for many years, buying outright or using a finance product that leads to ownership could represent better long-term value. While the initial outlay and ongoing depreciation are significant, the eventual absence of monthly payments (after finance is paid off) and the ability to recoup some value upon sale can be appealing.

PCH vs. PCP: Unravelling the Popular Finance Options

The world of car finance can often seem like a labyrinth of acronyms, and two of the most prevalent terms you'll encounter are Personal Contract Hire (PCH) and Personal Contract Purchase (PCP). While both involve making monthly payments for a specified period and are often confused, they serve fundamentally different purposes.

| Feature | Personal Contract Hire (PCH) | Personal Contract Purchase (PCP) |

|---|---|---|

| Nature of Agreement | Long-term rental/lease | Conditional sale agreement (finance) |

| Ownership | Never own the car; it belongs to the leasing company. | Option to own the car at the end of the agreement. |

| Initial Payment | Called an 'initial payment' (e.g., 3, 6, 9 months of payments). | Called a 'deposit'. |

| Monthly Payments | Covers depreciation and fees. Often lower than PCP for similar cars. | Covers depreciation and interest. |

| End of Agreement Options | Return the car. No option to buy. | Return the car, part-exchange for a new car, or pay a final 'balloon payment' to own it. |

| Mileage Limits | Strict limits apply; excess mileage charges. | Strict limits apply; excess mileage charges. |

| Vehicle Condition | Must be returned in good condition (fair wear and tear accepted). | Must be returned in good condition if not purchased. |

Both PCH and PCP agreements share similarities in their structure: you make an upfront payment (an initial payment for PCH, a deposit for PCP), followed by a series of fixed monthly payments over a predetermined period, and both come with an agreed annual mileage limit. Exceeding this limit in either agreement will incur additional charges.

The pivotal difference, however, lies in what happens at the conclusion of the contract. With PCH, your options are straightforward: you simply return the vehicle to the leasing company. There is no provision or option for you to purchase the car at the end of the term; it's purely a rental.

PCP, on the other hand, provides significantly more flexibility at the end of the agreement. You have three primary choices:

- Return the car: Similar to a lease, you can hand the car back to the finance company, provided it's within the agreed mileage and condition.

- Part-exchange for a new vehicle: You can use any "equity" you might have in the car (if its actual market value is higher than the outstanding balloon payment) towards the deposit for a new PCP agreement.

- Pay the 'optional final payment': This is a pre-agreed lump sum, also known as a 'balloon payment', which, if paid, transfers ownership of the vehicle to you. This is the pathway to ownership with PCP.

Making Your Informed Decision: Buying vs. Leasing

Ultimately, there is no single "best" option when it comes to acquiring a vehicle; the ideal choice is deeply personal and contingent upon your individual financial situation, driving habits, and priorities. The decline in traditional car ownership merely reflects a greater diversity in consumer needs and preferences.

If you are someone who cherishes the idea of long-term ownership, intends to keep a vehicle for many years, and is comfortable with the upfront capital expenditure and the eventual depreciation, then buying your car outright or via a traditional HP agreement remains the most suitable path. You gain full control over the vehicle, including modifications, and eventually, the absence of monthly payments.

However, if your preference is to consistently drive a new, reliable vehicle that benefits from manufacturer warranty coverage, to avoid the significant upfront costs and the financial impact of depreciation, and to change your car every few years with minimal fuss, then a leasing agreement, particularly PCH, emerges as the more appropriate and often more financially sensible choice. It offers predictability, lower monthly costs for access to new vehicles, and a hassle-free end-of-contract process.

Consider the following summary to help weigh your decision:

| Factor | Buying Outright/HP | Leasing (PCH/PCP) |

|---|---|---|

| Ownership | Yes (eventually with HP) | No (PCH), Option (PCP) |

| Upfront Cost | High (full price) | Low (initial payment/deposit) |

| Monthly Payments | Higher (HP), None (Outright after purchase) | Lower, predictable |

| Depreciation Risk | Borne by you | Borne by leasing company |

| New Car Frequency | Infrequent, involves selling/part-exchanging | Frequent (every 2-4 years) |

| Maintenance/Warranty | Your responsibility after warranty expires | Often covered by manufacturer warranty throughout lease |

| Flexibility | Full control, can sell anytime | Fixed term, mileage limits, return conditions |

Frequently Asked Questions About Car Leasing

Understanding the nuances of car leasing can raise several questions. Here are some of the most common queries:

Can I end a lease agreement early?

While it is technically possible to terminate a lease agreement before its scheduled end date, it is generally not advisable and can be quite costly. Leasing companies will typically charge early termination fees, which can amount to several months of payments or a significant portion of the remaining balance. It's crucial to review your contract's terms regarding early termination before committing to a lease, as these fees are designed to compensate the leasing company for the vehicle's lost value and administrative costs.

What happens if I exceed my agreed mileage limit?

All lease agreements, whether PCH or PCP, come with a strict annual mileage limit, which you agree upon at the outset. This limit directly influences your monthly payments, as higher mileage typically leads to greater depreciation. If you exceed this agreed limit, you will be charged an excess mileage fee for every mile over. These fees can vary significantly between providers and vehicles, often ranging from a few pence to over 50 pence per mile. It is vital to accurately estimate your annual mileage before signing a contract to avoid unexpected charges at the end of the term. If your driving habits change, it's sometimes possible to adjust the mileage limit mid-contract, though this may alter your monthly payments.

Is maintenance and servicing included in a lease?

Generally, a standard lease agreement (PCH) will not include routine maintenance and servicing costs. These will typically be your responsibility, just as they would be if you owned the car. However, many leasing companies offer optional "maintenance packages" or "full-service leases" that can be added to your monthly payments. These packages usually cover scheduled servicing, MOTs, and sometimes even tyre replacements or breakdowns. While adding to your monthly outlay, they provide a comprehensive, fixed-cost solution for vehicle upkeep, offering peace of mind and predictable budgeting.

Can I modify a leased car?

As the car belongs to the leasing company, any modifications to a leased vehicle are generally prohibited without explicit prior written consent. This includes both aesthetic changes (like custom paint jobs or aftermarket wheels) and performance enhancements. Even minor alterations could be deemed a breach of contract and might result in charges when the car is returned, to restore it to its original condition. If you wish to personalise your vehicle, ownership is typically the more appropriate route.

What condition must the car be in when I return it?

When returning a leased vehicle, it is expected to be in a condition that reflects "fair wear and tear," as defined by the British Vehicle Rental and Leasing Association (BVRLA) guidelines. These guidelines specify what constitutes acceptable deterioration through normal use (e.g., minor stone chips, small scratches). Anything beyond fair wear and tear, such as significant dents, deep scratches, interior damage, or unapproved modifications, will be classified as "excessive damage" and will incur repair charges. It is always advisable to thoroughly inspect the car a few weeks before its return date and address any potential issues to avoid unexpected costs.

Making the right choice between buying and leasing is a significant financial decision. By carefully considering your personal circumstances, financial capacity, and driving preferences, you can confidently select the option that best suits your needs and keeps you on the road efficiently and affordably.

If you want to read more articles similar to Leasing vs. Buying: Your UK Motoring Guide, you can visit the Taxis category.