03/02/2016

For self-employed taxi drivers across the UK, the roar of the engine and the satisfaction of a fare well-delivered are daily realities. However, beyond the journey itself lies the crucial, albeit less glamorous, task of managing your business finances and tax obligations. Understanding how long and what types of records you need to keep for HM Revenue and Customs (HMRC) is not just a bureaucratic chore; it's a fundamental part of running a successful, compliant business and avoiding unwelcome penalties. Whether you're a seasoned black cab driver or a private hire operator, mastering your record-keeping ensures you're ready for any HMRC query and that you're paying the right amount of tax, no more, no less.

- Why Accurate Record-Keeping is Non-Negotiable for Taxi Drivers

- How Long Must You Keep Your Records?

- What Records Should a Self-Employed Taxi Driver Keep?

- How to Keep Your Records: Methods and Best Practices

- Understanding Accounting Methods: Cash Basis vs. Traditional Accounting

- What If Your Records Are Lost or Destroyed?

- Frequently Asked Questions for Self-Employed Taxi Drivers

- Do I need to keep records if I'm self-employed?

- What happens if my records are inaccurate or incomplete?

- Can I use software to keep my records?

- What's the difference between cash basis and traditional accounting?

- What should I do if I lose my records?

- Do I need to keep records of personal income too?

- When does the tax year run in the UK?

Why Accurate Record-Keeping is Non-Negotiable for Taxi Drivers

As a self-employed individual, you are personally responsible for declaring your income and expenses through a Self Assessment tax return. This isn't just a formality; it's how HMRC determines your tax liability. Accurate and complete records are the bedrock of this process. Without them, filling in your tax return correctly becomes a guessing game, and that's a game you don't want to play with the taxman.

HMRC has the authority to check your records to ensure that the figures you've submitted are correct. If they find discrepancies or a lack of supporting documentation, you could face penalties and interest on underpaid tax. For a taxi driver, this means meticulously tracking every fare earned, every tank of fuel purchased, and every repair bill paid. These records serve as your evidence, providing a clear audit trail of your financial activities and demonstrating that you've fulfilled your tax obligations.

How Long Must You Keep Your Records?

The length of time you need to retain your business records is a critical piece of information for all self-employed individuals, including taxi drivers. It primarily depends on one factor: when you submit your Self Assessment tax return.

Tax Returns Submitted On or Before the Deadline

If you are organised and manage to send your tax return to HMRC by the official deadline (typically 31 January following the end of the tax year), you must keep your records for at least 22 months after the end of the tax year the return is for. Let's break this down with an example pertinent to your taxi business:

- The tax year runs from 6 April to 5 April.

- For the 2024 to 2025 tax year, the deadline for sending your online Self Assessment tax return is 31 January 2026.

- If you send it by this date, you must keep all your records for that tax year until at least the end of January 2027.

This period allows HMRC sufficient time to open an enquiry into your tax return if they deem it necessary. Being able to readily provide the requested documentation during such an enquiry is paramount.

Tax Returns Sent After the Deadline

Life happens, and sometimes, despite best intentions, a tax return might be submitted late. If you send your tax return after the deadline, the rules for record retention change slightly. In this scenario, you should keep your records for at least 15 months after the date you actually sent the tax return. This means if you submit your 2024 to 2025 tax return in March 2027 (late), you would need to keep those records until at least June 2028.

Summary of Record Retention Periods

To make it clearer, here's a table summarising the record-keeping durations:

| Tax Return Submission Time | Minimum Record Retention Period |

|---|---|

| On or Before the Deadline | At least 22 months after the end of the tax year the return is for |

| After the Deadline | At least 15 months after the date the tax return was sent |

It's always advisable to keep records for longer if you have space and it's practical, especially for significant purchases or long-term assets related to your taxi business.

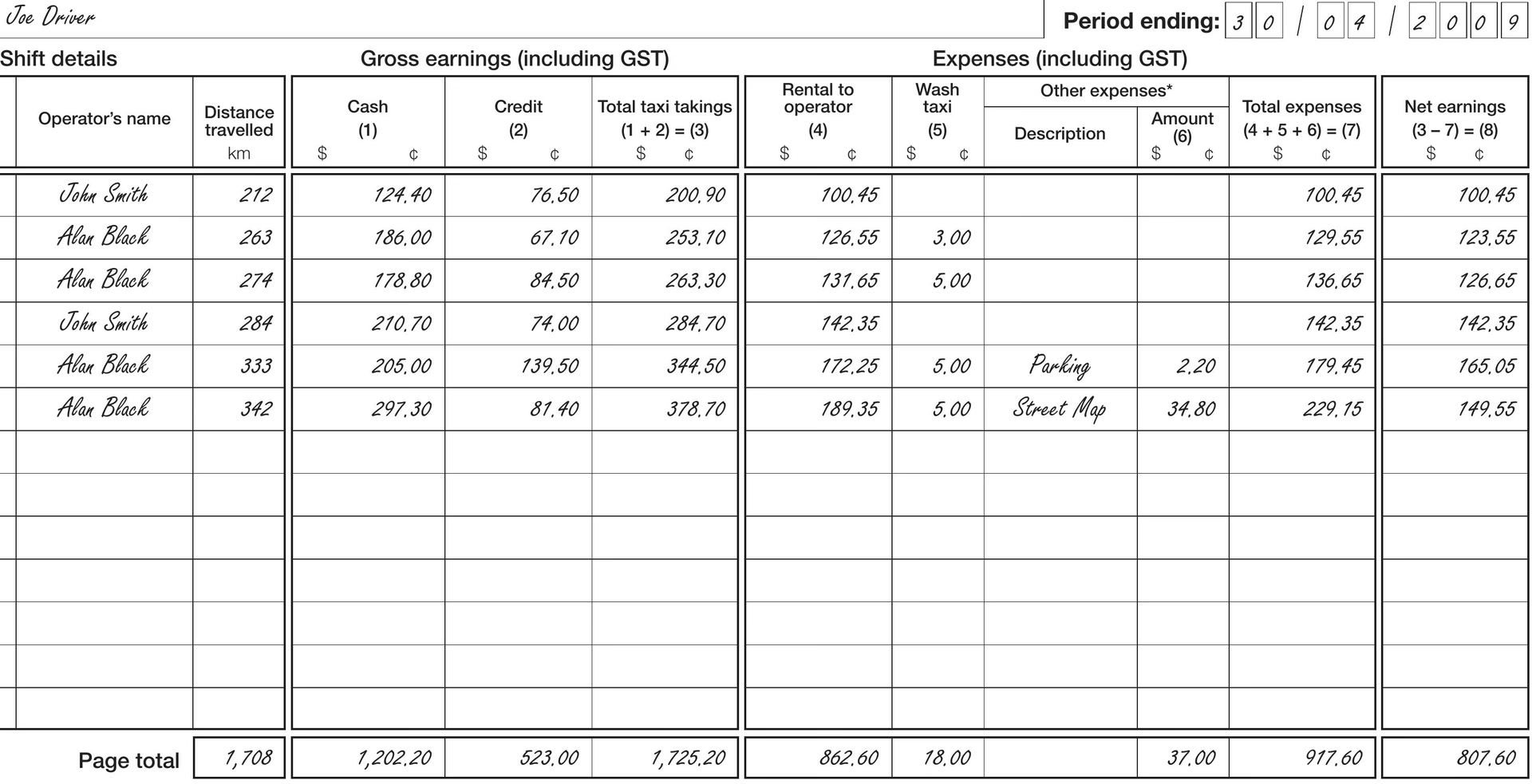

What Records Should a Self-Employed Taxi Driver Keep?

For your Self Assessment tax return, you must keep comprehensive records of both your business income and your expenses. This applies whether you operate as a sole trader or are a partner in a business partnership. If you are the nominated partner in a partnership, you also bear the responsibility for keeping records for the partnership as a whole.

Beyond your business finances, you'll also need to keep records of your personal income from all sources, as this contributes to your overall tax assessment.

Recording Your Income

Your income as a taxi driver typically includes:

- Fares received (cash, card payments, app-based payments)

- Tips (if applicable and declared)

- Any other income generated through your taxi business (e.g., advertising on your vehicle if you're paid for it).

It's vital to record the date, amount, and source of all income received.

Recording Your Expenses

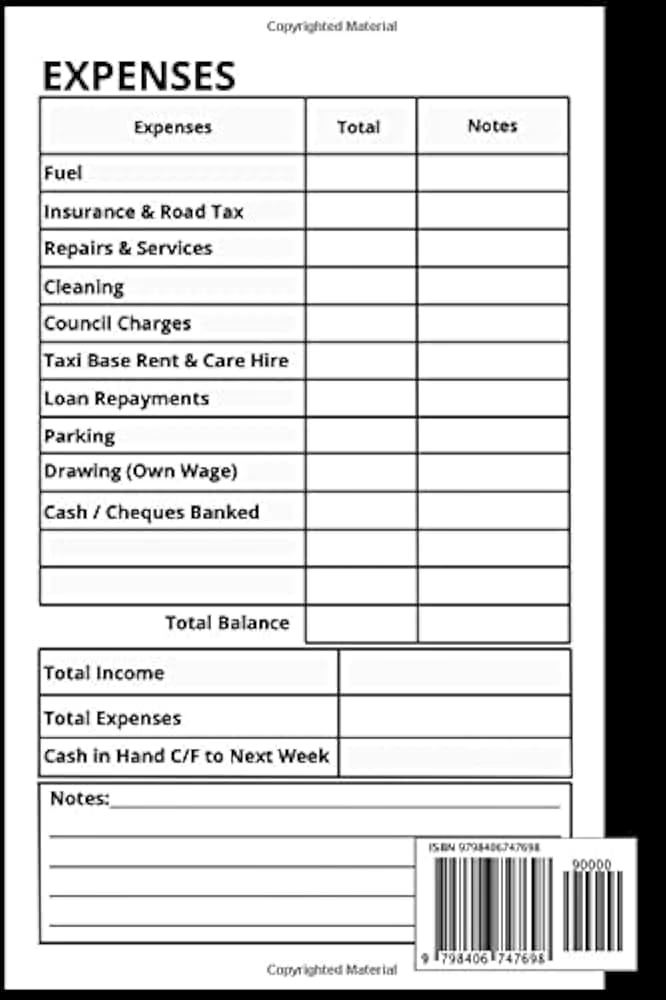

This is where many self-employed individuals can save money on their tax bill, by claiming legitimate business expenses. For a taxi driver, common allowable expenses include:

- Vehicle Costs: Fuel, oil, repairs and maintenance, servicing, MOTs, insurance, road tax (VED), vehicle licensing fees (e.g., Hackney Carriage or private hire licence).

- Running Costs: Car wash and cleaning supplies, parking fees, tolls, breakdown cover.

- Equipment: Taxi meter purchase and calibration, payment terminal fees and charges, two-way radio equipment.

- Professional Fees: Accountancy fees, legal fees related to your business.

- Licensing & Training: Driver's licence fees (the portion attributable to business use if it's a professional licence), taxi driver badge fees, any mandatory training courses.

- Office & Admin: Mobile phone bills (the business portion), stationery, small office supplies if you manage your bookings from home.

- Finance Costs: Interest on loans used for business purposes (e.g., to purchase your taxi).

For each expense, you should record the date, amount, what it was for, and keep the receipt or invoice as proof. Remember, expenses must be "wholly and exclusively" for the purpose of your trade.

How to Keep Your Records: Methods and Best Practices

HMRC is quite flexible when it comes to the method you use for record-keeping. There are no strict rules on whether you must use paper, digital files, or specific software. You can choose what works best for you and your taxi business:

- Paper Records: Keeping physical receipts, invoices, and bank statements in organised folders. While traditional, this method requires secure storage and can be prone to loss or damage.

- Digital Records: Scanning and saving documents as PDFs, using spreadsheets (like Excel) to log income and expenses. This is often more organised and can be backed up easily.

- Software Programs: Utilising bookkeeping software (e.g., QuickBooks, Xero, FreeAgent) specifically designed for small businesses. These often automate much of the process, link to your bank accounts, and can generate reports and even help prepare your Self Assessment.

Regardless of the method you choose, the absolute essentials are that your records must be accurate, complete, and readable. HMRC can levy a penalty if your records fail to meet these standards. Ensure that all figures are correct, nothing is missing, and that the information can be clearly understood by anyone reviewing it, including yourself and HMRC.

Many self-employed individuals choose to align their record-keeping dates with the tax year (6 April to 5 April). This can significantly simplify the process of completing your tax return, as HMRC calculates tax based on this specific period. If your accounting period doesn't match the tax year, you'll need to allocate profits across different accounting periods, which can add complexity.

Understanding Accounting Methods: Cash Basis vs. Traditional Accounting

When recording your income and expenses, you'll need to choose an accounting method. From the 2024 to 2025 tax year, there's been a significant change: cash basis is now the default method for most businesses. However, you can opt out if you prefer to use traditional accounting or if your business is not eligible for cash basis.

Cash Basis Accounting

This method is generally simpler and designed for smaller businesses. With cash basis accounting, you only record income or expenses when you actually receive the money or pay a bill. This means you don't pay Income Tax on money you haven't yet received.

Example for a Taxi Driver: You complete a job on 20 March 2025, but the customer pays you via a booking app on 10 April 2025. Under cash basis, you would record this income as received on 10 April 2025, placing it in the 2025 to 2026 tax year, not the 2024 to 2025 tax year.

Traditional Accounting (Accrual Basis)

Many businesses, particularly larger ones or those with more complex finances, use traditional accounting. With this method, you record income and expenses by the date you invoiced or were billed, regardless of when the money actually changed hands.

Example for a Taxi Driver: Using the previous example, if you completed the job on 20 March 2025, you would record that income on 20 March 2025, placing it in the 2024 to 2025 tax year, even if the payment wasn't received until April.

Comparison of Accounting Methods

| Feature | Cash Basis Accounting | Traditional Accounting |

|---|---|---|

| When Income is Recorded | When money is physically received | When invoiced or earned (regardless of payment) |

| When Expenses are Recorded | When money is physically paid out | When billed or incurred (regardless of payment) |

| Default from 2024-25 | Yes, for most businesses | No, you must opt out of cash basis |

| Tax on Unreceived Income | No, you don't pay tax until payment is received | Yes, you pay tax on income when earned, even if not yet received |

| Complexity | Generally simpler | Can be more complex, especially with debtors/creditors |

For most self-employed taxi drivers, the cash basis method will likely be the simpler and more appropriate choice, especially given its new default status. However, it's always worth discussing your specific situation with an accountant if you're unsure.

What If Your Records Are Lost or Destroyed?

Losing or destroying your financial records can be a daunting prospect, but it's not the end of the world. HMRC understands that accidents happen. Your first step should be to try and get copies of as much as you can. This might involve:

- Contacting your bank for copies of statements.

- Asking suppliers (e.g., fuel stations, garages, insurance providers) for duplicate invoices or receipts.

- Requesting payment summaries from booking apps or card payment providers.

If, despite your best efforts, you cannot recreate all your records, you are allowed to use 'provisional' or 'estimated' figures when completing your tax return. However, this comes with important caveats:

- Provisional Figures: Use this if you expect to be able to get the paperwork to confirm your figures later. For example, you're waiting for a bank statement that covers a specific period.

- Estimated Figures: Use this if you genuinely believe you will not be able to confirm the figures with actual paperwork at any point. This should be a last resort.

Crucially, if you use either provisional or estimated figures, you must state this clearly in the 'Any other information' box on your Self Assessment tax return. This informs HMRC that your figures are not fully supported by original documents.

Be aware that if your figures turn out to be wrong and you have not paid enough tax, you may still have to pay interest and penalties, even if you notified HMRC that you used estimated figures. The onus is still on you to be as accurate as possible, even in difficult circumstances. Always keep meticulous records to avoid this situation entirely.

Frequently Asked Questions for Self-Employed Taxi Drivers

Do I need to keep records if I'm self-employed?

Yes, absolutely. If you are self-employed and need to send a Self Assessment tax return to HMRC, you are legally required to keep records of all your business income and expenses. These records are essential for accurately filling in your tax return and for providing evidence if HMRC decides to check your return.

What happens if my records are inaccurate or incomplete?

HMRC can charge you a penalty if your records are not accurate, complete, and readable. Inaccurate records can lead to an incorrect tax calculation, potentially resulting in underpaid tax, which will then incur interest and further penalties.

Can I use software to keep my records?

Yes, you can. HMRC allows you to keep your records on paper, digitally (e.g., spreadsheets), or as part of a software program, such as bookkeeping software. Many self-employed taxi drivers find software to be an efficient way to manage their finances, especially with the move towards Making Tax Digital (MTD) in the future.

What's the difference between cash basis and traditional accounting?

With cash basis accounting, you record income and expenses only when money is actually received or paid out. With traditional (accrual) accounting, you record income and expenses when they are earned or incurred, regardless of when the money changes hands. From the 2024 to 2025 tax year, cash basis is the default method for most self-employed businesses.

What should I do if I lose my records?

Firstly, try your best to get copies of any lost documents from banks, suppliers, or other sources. If you still can't recreate all records, you can use 'provisional' or 'estimated' figures on your tax return, but you must declare this in the 'Any other information' box. Be aware that you could still face penalties if your estimated figures lead to underpaid tax.

Do I need to keep records of personal income too?

Yes, in addition to your business income and expenses, you should also keep records of any other personal income you receive (e.g., from employment, property, or investments). This is because all your income sources contribute to your overall Self Assessment tax calculation.

When does the tax year run in the UK?

The UK tax year runs from 6 April of one year to 5 April of the following year. For example, the 2024 to 2025 tax year runs from 6 April 2024 to 5 April 2025.

In conclusion, keeping accurate and organised tax records is a cornerstone of responsible self-employment for taxi drivers. By understanding the retention periods, knowing what to record, and choosing an appropriate accounting method, you can navigate your tax obligations with confidence, ensuring compliance with HMRC and ultimately, a smoother ride for your taxi business.

If you want to read more articles similar to Taxi Drivers: How Long to Keep Your Tax Records?, you can visit the Taxis category.