29/08/2024

- Navigating the New Digital Platform Tax Landscape in the UK

- What are the New Digital Platform Reporting Rules?

- Key Dates and Scope of the Rules

- Defining a Digital Platform Under the Rules

- Who Needs to Register and Report?

- Information to be Reported

- Due Diligence and Reporting Deadlines

- Implications for Sellers (Including Taxi Drivers)

- Potential Penalties

- The Broader Impact and Objective

- Frequently Asked Questions

- What if I operate on multiple digital platforms?

- What if I am a UK resident but earn money on a platform based outside the UK?

- Do these rules apply to renting out my car when I'm not driving it?

- What constitutes an 'active seller'?

- Will my bank details be shared with HMRC?

- What should I do if the information reported by the platform is incorrect?

The modern economy is increasingly shaped by digital platforms, acting as crucial intermediaries for everything from taxi rides and food deliveries to freelance work and the sale of goods. While these platforms offer unprecedented convenience and opportunity, they also present a significant challenge for tax authorities worldwide. The ability for individuals and businesses to generate income across different jurisdictions without immediate or transparent reporting has created a gap that governments are now actively working to close. In the UK, this has led to the introduction of new, comprehensive reporting rules for digital platforms, designed to enhance tax compliance and combat evasion.

What are the New Digital Platform Reporting Rules?

Building upon the Organisation for Economic Co-operation and Development (OECD) model rules, the UK government has implemented new regulations requiring digital platforms to report information about the income earned by sellers operating through their services. This means that companies like Uber, FREENOW, Bolt, and Gett, among others, will now be obligated to share data on their sellers' earnings with HM Revenue and Customs (HMRC). Crucially, a copy of this information will also be provided to the sellers themselves, aiming to assist them in accurately declaring their income. HMRC, in turn, will exchange this data with tax authorities in other participating countries where sellers might be tax residents, fostering greater international cooperation in tax matters.

Key Dates and Scope of the Rules

These new reporting obligations came into effect on 1 January 2024. The first reporting deadline for the 2024 calendar year is 31 January 2025. The rules apply broadly to:

- UK-resident platforms facilitating the provision of services or the sale of goods.

- Non-UK platforms with a UK permanent establishment or those registered for UK VAT.

However, there are specific exclusions. The rules will not cover the rental of transport, such as car-sharing or bike-sharing platforms. Furthermore, sellers who only occasionally sell a few goods, for instance, on general online marketplaces, may also be excluded.

Defining a Digital Platform Under the Rules

To determine if an app or website falls under these reporting requirements, two key criteria must be met:

- The platform must connect sellers with customers to supply goods or services. This includes sectors like taxi hire, food delivery, freelance work, and short-term accommodation letting.

- The platform operator must know, or be able to easily ascertain, the amount paid to the sellers for these goods or services.

Examples of qualifying digital platforms include online marketplaces for clothing or websites connecting guests with accommodation owners where payments are processed. Conversely, platforms that merely list or advertise products, redirect users to other sites, process payments solely, or assist with website design and maintenance are generally not considered digital platforms for these reporting purposes.

Who Needs to Register and Report?

If you operate a digital platform in the UK that meets the definition, you may need to register with HMRC. This requirement applies if:

- You reside in the UK.

- Your platform is managed under UK laws.

- Your business operations are managed in the UK.

You are generally not required to register if you only sell on a platform, manage a platform as a sole trader, or sell your own goods or services directly through your own website or app.

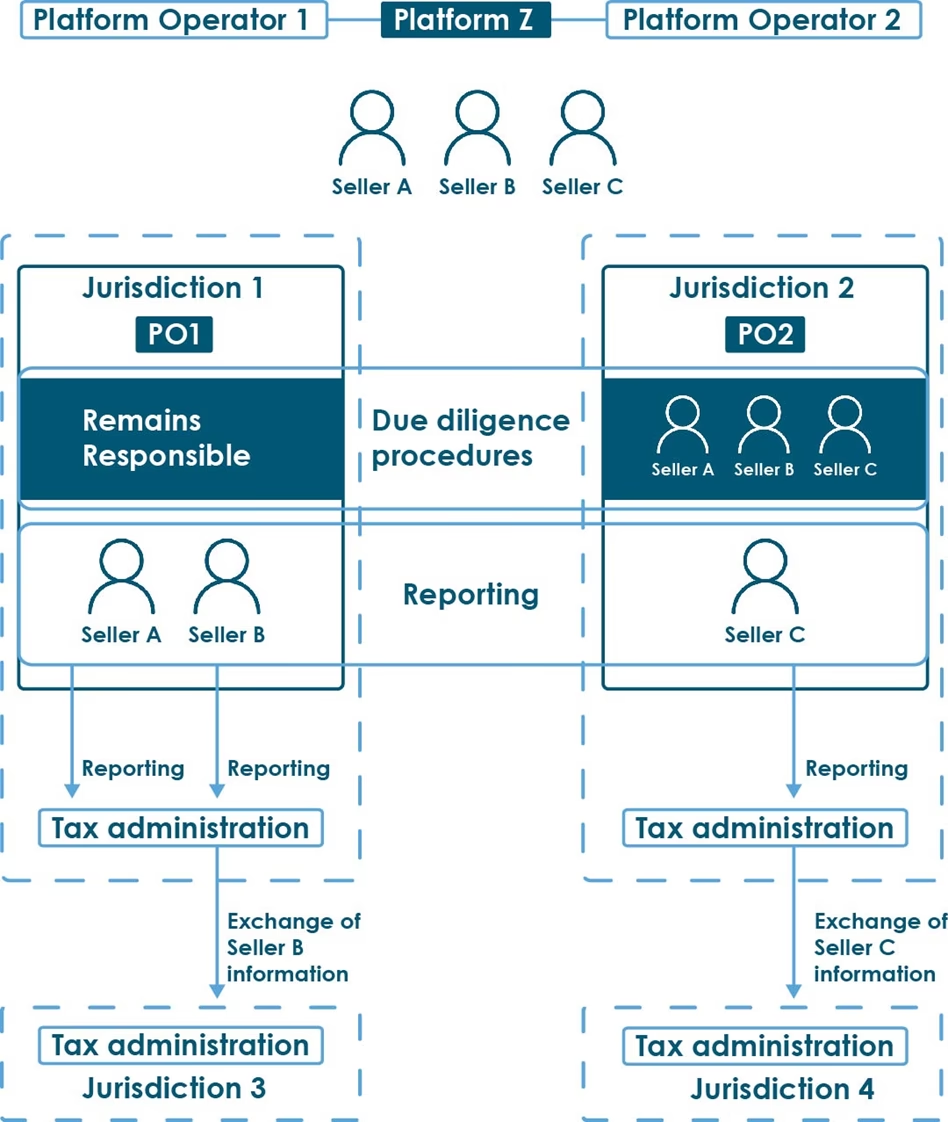

Platform operators must inform HMRC whether they are a 'reporting platform operator' or an 'excluded platform operator'. An excluded operator is one whose business model either does not allow sellers to profit from received payments or has no 'reportable sellers'. Reportable sellers are those who actively supply or are paid for goods/services on the platform and are tax resident in the UK or another 'Reportable Jurisdiction'.

Information to be Reported

Reporting platform operators must collect and verify specific information about their sellers. This process is known as 'due diligence'. The information required includes:

- Seller's Country of Residence: Essential for international data exchange.

- Total Amount Paid: The gross amount paid to the seller for the reporting year.

- Number of Transactions: The volume of payments received by the seller.

- Fees, Commissions, or Taxes Withheld: Any deductions made by the platform.

- Bank Account Details: Where payments were made, including account holder name and identifying details if different from the seller.

For individual sellers, the following personal details are needed:

- Full Name

- Home Address

- Date of Birth

- National Insurance Number (for UK residents) or Tax Identification Number and issuing country (for non-UK residents)

- Other tax identification numbers (e.g., VAT number) and their issuing countries, if available.

For entities (companies, partnerships, trusts, charities), the required information includes:

- Legal Business Name

- Main Business Address

- Company Registration Number (for UK companies) or Tax Identification Number and issuing country (for non-UK entities)

- Other tax identification numbers (e.g., VAT number) and their issuing countries, if available.

- For UK partnerships, the Unique Taxpayer Reference (UTR) is also required.

Due Diligence and Reporting Deadlines

Carrying out due diligence is a critical responsibility, even if outsourced to a third party. Platforms can opt to conduct due diligence only on 'active sellers' (those receiving payments during the reportable period). For platforms newly subject to these rules, there are extended time limits for conducting due diligence on 'pre-existing sellers' (those registered before the reporting obligation began). This typically means an additional year to collect and verify information for these long-standing users.

For example, if a platform becomes subject to the rules on 1 July 2024, its first reportable period is 2024. Due diligence must be completed by 31 December 2024 for sellers who registered on or after 1 July 2024, and by 31 December 2025 for those who registered before 1 July 2024. Failure to meet these deadlines can result in penalties.

The annual report must be submitted to HMRC by 11:59 pm on 31 January of the following year. This report must be submitted using the specified XML schema. It's crucial to ensure the report passes HMRC's checks by this deadline to avoid penalties for late reporting. A copy of the reported information must also be provided to the seller by the same deadline.

Implications for Sellers (Including Taxi Drivers)

These new rules are designed to help sellers, including taxi drivers, get their tax right from the outset and simplify tax compliance. By receiving a copy of the data reported by the platform, sellers can more easily reconcile this with their own records and ensure accurate declarations on their tax returns.

Best Practices for Sellers:

- Keep Meticulous Records: Track all income received from digital platforms and any other sources. Compare this with the information provided by the platforms. Maintain detailed records of all eligible expenses and deductions (e.g., platform fees, commissions, vehicle running costs for taxi drivers) as these can reduce your taxable income.

- Report Accurately: The reporting rules do not alter your fundamental tax obligations. Ensure you declare all your income on your tax return and pay the tax due. If you are tax resident in multiple jurisdictions, report your income accordingly and claim any applicable double taxation relief.

- Understand Your Tax Position: Depending on your residency and other factors, these rules might affect your tax status. Check if you need to register for specific taxes like income tax or VAT. Familiarise yourself with any available allowances or reliefs. Online tools or professional advice can be invaluable here.

- Update Your Information Promptly: Platforms are required to collect and verify your personal and tax identification details. Provide accurate and complete information when requested, and ensure any changes (like a new address or tax number) are updated immediately. Respond promptly to any queries from platforms or HMRC.

Potential Penalties

Non-compliance with these regulations can lead to significant penalties for platform operators, including:

- Up to £1,000 for failing to notify HMRC about their status as a reporting or excluded operator.

- An initial penalty of up to £5,000, plus a continuing penalty of up to £600 per day for failing to report by the 31 January deadline.

- Up to £100 for each inaccurate, incomplete, or unverified seller record.

Platforms may also need to take action if sellers do not cooperate, such as limiting access or preventing new registrations until the required information is provided.

The Broader Impact and Objective

The overarching goal of these regulations is to create a level playing field between digital businesses and traditional ones, ensuring that income generated through the digital economy is taxed fairly. By enhancing transparency and facilitating data exchange, HMRC aims to make it easier for taxpayers to comply with their obligations and to more effectively detect and tackle tax evasion. While these changes introduce new responsibilities for platforms and sellers, they are a necessary step towards a more equitable and robust tax system in the digital age. For taxi drivers and other gig economy workers, understanding these changes and proactively managing their tax affairs will be key to smooth compliance.

Frequently Asked Questions

What if I operate on multiple digital platforms?

You will need to ensure you comply with the reporting requirements for each platform you use. Each platform will report your earnings from their service to HMRC, and you should ensure your tax return accurately reflects your total income from all sources.

What if I am a UK resident but earn money on a platform based outside the UK?

If the platform is considered a 'reporting platform' under the OECD model rules and operates in a participating jurisdiction, your income may still be reported to HMRC through international data exchange. It is essential to declare all worldwide income where you are tax resident.

Do these rules apply to renting out my car when I'm not driving it?

No, the rules specifically exclude the rental of transport, such as car-sharing or bike-sharing platforms.

What constitutes an 'active seller'?

An active seller is someone who actively supplies or is paid for goods or services during the reportable period (1 January to 31 December).

Yes, if the platform holds your bank account details and makes payments to them, this information may be reported to HMRC as part of the due diligence process.

What should I do if the information reported by the platform is incorrect?

You should first contact the platform operator to request a correction. If the issue is not resolved, you should report the correct information to HMRC on your tax return and provide any supporting evidence.

If you want to read more articles similar to UK Digital Platform Tax Reporting Explained, you can visit the Taxis category.