15/09/2016

For UK businesses, navigating the complexities of tax legislation can often feel like a daunting task. Yet, hidden within these rules are powerful mechanisms designed to encourage investment and foster growth. One such invaluable tool is the Annual Investment Allowance (AIA). If your business is considering investing in new equipment or machinery, understanding the AIA is not just beneficial – it's absolutely essential for effective tax planning. This guide will meticulously break down the AIA rules for 2025/26 and beyond, demonstrating how your UK business can leverage this significant tax relief to reduce its liabilities and free up capital for further development.

- What Exactly is the Annual Investment Allowance (AIA)?

- Who is Eligible to Claim AIA?

- What Assets Qualify for AIA?

- Understanding the Timing of Your AIA Claim

- How to Effectively Claim AIA

- AIA Versus Full Expensing: A Key Distinction

- Practical AIA Planning Tips for Your Business

- Common Questions About the Annual Investment Allowance

- Final Thoughts on the Annual Investment Allowance

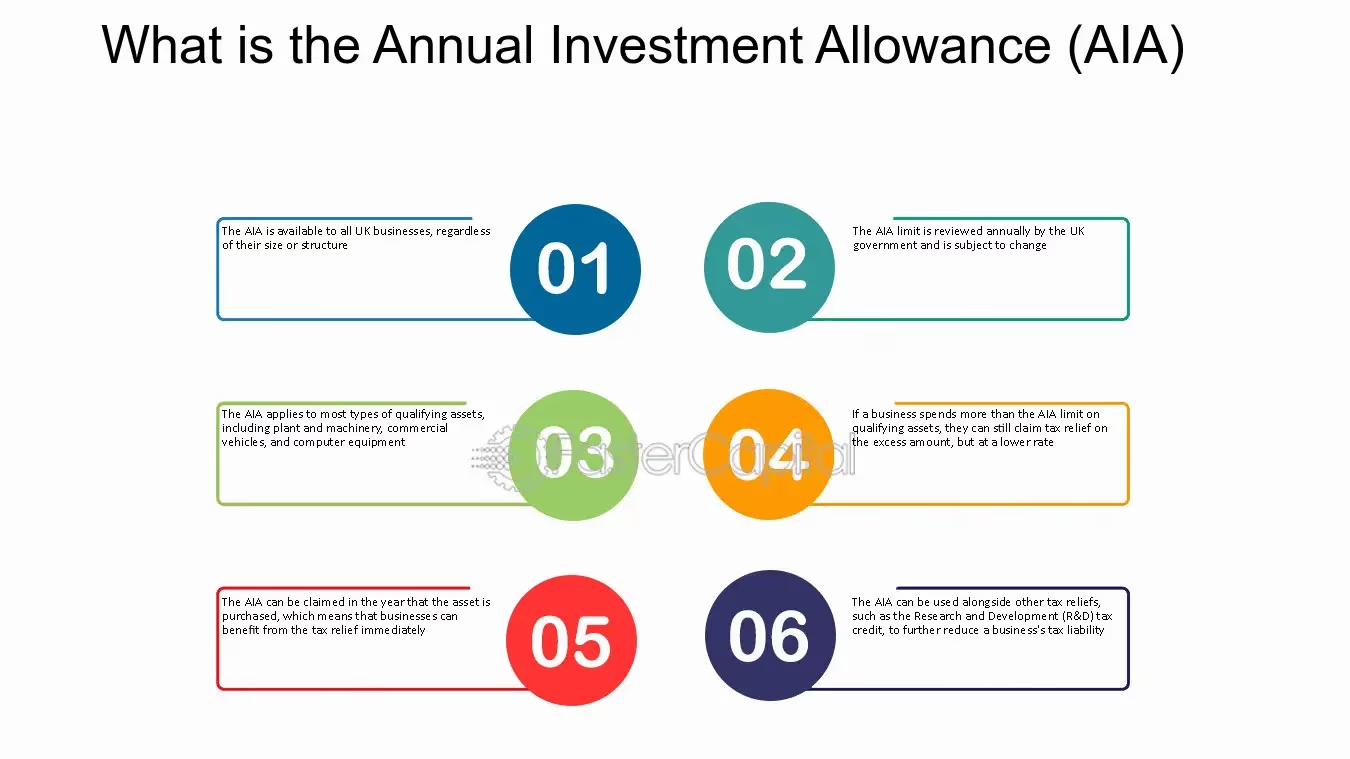

What Exactly is the Annual Investment Allowance (AIA)?

The Annual Investment Allowance (AIA) is a crucial tax relief that permits businesses to deduct the entire cost of eligible capital purchases from their profits before tax. This means that instead of deducting a small percentage of the asset's value each year (as is the case with Writing Down Allowances), you can claim 100% of the cost in the year you buy it, up to a specific limit. This immediate relief provides a substantial cash flow advantage, making it more attractive for businesses to invest in their future.

Since its introduction, the AIA limit has fluctuated, but it has been consistently set at a generous level to stimulate economic activity. For the 2025/26 tax year, the AIA limit remains at a substantial £1 million. This means that for most small to medium-sized businesses, the vast majority, if not all, of their annual qualifying capital expenditure can be offset against their taxable profits, leading to a direct reduction in their tax bill.

Who is Eligible to Claim AIA?

One of the strengths of the AIA is its broad applicability across various business structures in the UK. Unlike some other tax reliefs that are exclusive to large corporations, AIA is designed to benefit a wide spectrum of enterprises. Specifically, AIA is available to:

- Sole traders: Individuals running their own business.

- Partnerships: Groups of individuals or companies working together, though notably, partnerships with corporate partners have specific rules and may not qualify in the same way.

- Limited companies: The most common form of incorporated business in the UK.

Crucially, businesses of all sizes can claim the AIA, from a small independent consultant purchasing a new laptop to a manufacturing firm investing in significant machinery. The primary condition is that the assets purchased must be used for genuine business purposes. This broad eligibility ensures that a wide array of UK businesses can benefit from this valuable relief, fostering investment across the economy.

What Assets Qualify for AIA?

Understanding which assets are eligible for AIA is paramount for effective planning. The relief primarily applies to what HMRC classifies as "plant and machinery." This category is broader than many might initially assume and encompasses a wide range of tangible assets essential for business operations. Here’s a breakdown of common qualifying items:

- Office equipment: This includes everything from desks, chairs, and filing cabinets to computers, printers, servers, and telecommunication systems. Essential for any modern office environment.

- Machinery and tools: For manufacturing, construction, or trade businesses, this covers production machinery, power tools, workshop equipment, and specialist apparatus.

- Vans, lorries, and some commercial vehicles: Vehicles used purely for business purposes, such as delivery vans, lorries, and even certain types of commercial cars (e.g., taxis, driving school cars, or pool cars not available for private use) can qualify. However, standard company cars or cars available for private use are generally excluded.

- Fixtures: These are items that are part of the building but are considered plant and machinery for tax purposes. Examples include kitchen or bathroom fittings within a commercial building, electrical systems, heating and ventilation systems, lifts, and even alarm systems.

- Agricultural machinery: Tractors, harvesters, and other farming equipment.

- Computer software: Certain types of software, particularly those embedded in qualifying hardware or purchased as a capital asset, can also qualify.

However, it's equally important to be aware of items that are typically excluded from AIA claims:

- Cars: Most cars are excluded from AIA, even if used solely for business. There are limited exceptions, such as specific low-emission vehicles or those not available for private use (e.g., taxis, driving school cars) which might qualify for different capital allowances or, in very specific circumstances, the AIA. Always verify with current HMRC guidance.

- Items gifted to the business: Assets received without payment do not qualify for AIA.

- Assets used before being acquired for the business: If you acquire an asset that was already in use by you or a connected party before it was formally brought into the business, it generally won't qualify.

- Land and buildings: These are not considered plant and machinery.

- Expenditure on intangible assets: Such as patents, trademarks, or goodwill, generally do not qualify.

Careful categorisation of assets is crucial to ensure compliance and maximise your claim.

Understanding the Timing of Your AIA Claim

The timing of your capital purchases is not just a logistical consideration; it has direct implications for your AIA claim. The AIA can only be claimed in the accounting period when the asset was purchased and, critically, made available for use. This means that if you buy a piece of machinery in the last month of your financial year, but it isn't installed and ready for operation until the next financial year, the AIA claim would typically fall into that subsequent period.

This "made available for use" rule is particularly important for large projects or assets requiring installation. Businesses should plan their purchases strategically to ensure they fall within the desired accounting period for maximum tax relief. If your business has a short or extended accounting period (i.e., less or more than 12 months), the AIA limit of £1 million is apportioned accordingly. For example, a six-month accounting period would typically have an AIA limit of £500,000 (£1 million / 12 * 6).

Consider the example of a business whose accounting period ends on 31 March. If they purchase a qualifying asset on 15 March and it's available for use by 30 March, they can claim the AIA in that accounting period. However, if the asset isn't available for use until 5 April, the claim would be deferred to the next accounting period. Strategic timing can therefore significantly impact when your business benefits from the tax relief.

How to Effectively Claim AIA

Claiming the Annual Investment Allowance is an integral part of your annual tax compliance. The process is straightforward, but accuracy and meticulous record-keeping are paramount:

- Via your annual tax return: For limited companies, the claim is made through the Corporation Tax return (CT600). For sole traders and partnerships, it's declared on the self-assessment tax return. There are specific sections within these forms to report capital allowances, including AIA.

- Maintain clear records and invoices: HMRC requires businesses to keep comprehensive records of all capital purchases. This includes original invoices, proof of payment, and details of when the asset was purchased and made available for use. These records are vital for substantiating your claim in the event of an HMRC enquiry.

- Understanding excess expenditure: If your total qualifying capital expenditure in an accounting period exceeds the AIA limit (currently £1 million), the remainder does not simply disappear. Instead, any expenditure above the AIA limit may qualify for Writing Down Allowances (WDA). WDA allows you to claim a percentage of the asset's value each year over its useful life, typically at 18% or 6% depending on the asset pool. While not as immediate as AIA, WDA still provides valuable ongoing tax relief.

It's crucial to correctly identify and categorise your assets to ensure they meet the AIA criteria. Incorrect claims can lead to penalties, so when in doubt, seeking professional advice is always recommended.

AIA Versus Full Expensing: A Key Distinction

For many businesses, particularly limited companies, there’s another significant capital allowance regime to consider: Full Expensing. Introduced more recently, Full Expensing allows companies to deduct 100% of the cost of qualifying new plant and machinery from their taxable profits in the year of purchase. While this sounds very similar to AIA, there are key differences:

| Feature | Annual Investment Allowance (AIA) | Full Expensing |

|---|---|---|

| Eligibility | Sole traders, partnerships (excl. corporate), limited companies. | Limited companies only. |

| Asset Type | Most new and used plant and machinery. | New (not used) plant and machinery only. |

| Limit | £1 million per year. | No monetary limit for qualifying assets. |

| Disposal Charge | If asset sold for more than tax written down value, a balancing charge may arise. | If asset sold, a balancing charge equal to 100% of disposal proceeds applies (up to original cost). |

| Benefit | Immediate 100% relief up to limit. | Immediate 100% relief (or 50% for special rate assets) with no limit. |

The primary advantage of AIA is its accessibility to sole traders and partnerships who do not qualify for Full Expensing. For limited companies, Full Expensing offers an unlimited 100% deduction for new plant and machinery, which can be more beneficial for very large investments exceeding the £1 million AIA limit. However, AIA remains highly relevant even for limited companies, particularly for purchases of second-hand assets which qualify for AIA but not for Full Expensing, or for smaller investments where the simplicity of AIA is preferred.

Practical AIA Planning Tips for Your Business

Strategic planning is key to maximising the benefits of the Annual Investment Allowance. Here are some actionable tips:

- Time purchases strategically: If you anticipate making significant capital expenditures that might push you close to or over the AIA limit, consider timing your purchases to fall within the same accounting year. This ensures you maximise the 100% immediate relief. Conversely, if you have multiple businesses under common control, the £1 million AIA limit must be shared amongst them, so careful planning across entities is vital.

- Monitor your AIA usage: Keep a running tally of your capital expenditure throughout the year. This allows you to track how much of your AIA limit you have utilised and helps in making informed decisions about further investments.

- Combine AIA with other capital allowances: Don't view AIA in isolation. For expenditure exceeding the AIA limit, or for assets that don't qualify for AIA (like certain cars), ensure you claim Writing Down Allowances (WDA). For example, if you spend £1.2 million on qualifying plant and machinery, you can claim £1 million under AIA, and the remaining £200,000 would typically go into the main pool for WDA at 18% per annum. Combining these allowances ensures maximum tax efficiency.

- Review group structures: If your business is part of a group, the £1 million AIA limit is shared across all qualifying companies within that group. Proper allocation and planning are essential to avoid missing out on relief or making incorrect claims.

Common Questions About the Annual Investment Allowance

Can I claim AIA if I buy a second-hand asset?

Yes, unlike Full Expensing, AIA can generally be claimed on both new and qualifying second-hand plant and machinery. This makes it a highly flexible relief for businesses looking for cost-effective equipment solutions.

What happens if I sell an asset I claimed AIA on?

If you sell an asset for which you claimed AIA, a "balancing charge" may arise. This means that the proceeds from the sale (up to the original cost of the asset) will be added back to your taxable profits in the year of disposal. This effectively claws back the tax relief you received, ensuring fairness in the system. If the sale proceeds are less than the tax written down value (which would be zero if you claimed 100% AIA), there is no balancing allowance, only a balancing charge if you sell it for more than zero.

Is AIA compulsory? Do I have to claim it?

No, claiming AIA is not compulsory. You can choose to claim less than the full amount or not claim it at all, opting instead to claim Writing Down Allowances. However, for most businesses, claiming the full AIA is the most tax-efficient option due to the immediate 100% relief it provides. There might be niche scenarios where deferring relief makes sense, but these are rare.

How does AIA affect my cash flow?

By allowing you to deduct the full cost of an asset immediately, AIA significantly reduces your taxable profits in the year of purchase. This directly translates to a lower tax bill, which means your business retains more cash. This improved cash flow can then be reinvested into the business, used to pay down debt, or support other operational needs, effectively making capital investment more affordable.

Can I claim AIA on a car used for business?

Generally, no. Most cars, even if used solely for business, are excluded from AIA. There are very limited exceptions for cars that are specifically designed for commercial purposes and not suitable for private use, or certain low-emission vehicles that might qualify under other capital allowance rules. Always check specific HMRC guidance for vehicles.

What if my accounting period is shorter or longer than 12 months?

If your accounting period is shorter or longer than 12 months, the £1 million AIA limit is proportionately reduced or increased. For example, for a 6-month period, the limit would be £500,000. For an 18-month period, it would be £1.5 million. This ensures the relief is applied fairly regardless of your financial year length.

Final Thoughts on the Annual Investment Allowance

The Annual Investment Allowance is undeniably one of the most powerful tax reliefs available to UK businesses investing in their future. Its ability to provide 100% immediate relief on significant capital expenditure, up to £1 million, makes it an indispensable tool for managing tax liabilities and enhancing cash flow. Whether you are a sole trader purchasing essential office equipment or a growing limited company investing in cutting-edge machinery, understanding and strategically applying AIA can have a profound positive impact on your bottom line. By meticulously planning your asset purchases, maintaining diligent records, and understanding how AIA interacts with other capital allowances like Writing Down Allowances and Full Expensing, your business can truly maximise its tax efficiency and foster sustainable growth. Don't let this valuable relief go unclaimed; proactive tax planning is the cornerstone of a financially robust business.

If you want to read more articles similar to Maximising Your Business Tax Relief with AIA, you can visit the Taxis category.