13/08/2017

Value Added Tax (VAT) in the UK can often feel like navigating a complex labyrinth, especially when distinguishing between different categories of supplies. A common point of confusion for many businesses and consumers alike revolves around zero-rated goods and services. Are they truly taxable? And how do they differ from VAT-exempt items? Understanding these distinctions is not merely an academic exercise; it's fundamental to ensuring your business remains compliant with HMRC regulations, manages its cash flow effectively, and avoids costly penalties. This comprehensive guide aims to demystify zero-rated VAT, clarify its relationship with taxable supplies, and highlight the critical differences from VAT-exempt provisions, providing you with the essential knowledge to confidently navigate the UK's VAT landscape.

At its core, VAT is a consumption tax levied on most goods and services in the UK. While the standard rate currently stands at 20%, various other rates and categories exist to cater to different economic activities and societal needs. Among these, zero-rated and exempt supplies often cause the most head-scratching. Let's dive into what zero-rated VAT truly means and why its classification is so crucial.

- Understanding Zero-Rated VAT: A Taxable Supply at 0%

- VAT Exemption: Outside the Scope of VAT

- Key Differences: Zero-Rated vs. VAT-Exempt Supplies

- Impact on Businesses: Registration, Partial Exemption, and More

- The Importance of Accurate Classification and Record-Keeping

- Frequently Asked Questions About Zero-Rated and Exempt VAT

- Conclusion: Mastering VAT for Business Success

Understanding Zero-Rated VAT: A Taxable Supply at 0%

The immediate answer to the question, "Are zero-rated goods taxable for VAT?" is a resounding yes, but with a crucial caveat: they are taxable at a rate of 0%. This might seem contradictory at first glance, but the distinction is vital. When a supply is zero-rated, it means that while it falls within the scope of VAT, no VAT is actually charged to the customer on the sale. The significant benefit for businesses making zero-rated supplies is that they are still entitled to reclaim any input VAT they have incurred on purchases and expenses related to those supplies.

This ability to reclaim input VAT is the cornerstone of why zero-rated status is so advantageous for businesses. It effectively means that the business doesn't bear the cost of VAT on its purchases, even though it doesn't charge VAT on its sales. This can significantly improve a business's cash flow and competitiveness, as the VAT element of their operational costs can be recovered from HMRC.

Common Examples of Zero-Rated Supplies in the UK:

- Most Food and Drink: A wide range of everyday foodstuffs, excluding certain items like confectionery, crisps, alcoholic drinks, and hot takeaways, are zero-rated. This ensures essential food items remain affordable for consumers.

- Books and Newspapers: Printed books, brochures, leaflets, and newspapers are typically zero-rated, promoting education and access to information.

- Children's Clothes and Footwear: To support families, most clothing and footwear designed for children are zero-rated.

- Prescription Medicines: As highlighted in the provided information, most medicines dispensed on prescription are zero-rated, making essential healthcare more accessible.

- Public Transport: Fares for most forms of public transport, such as bus and train travel, are zero-rated.

- Exports: Goods and services exported from the UK to non-UK destinations are generally zero-rated, supporting international trade.

- Certain Building Works: Some specific building works, particularly those related to new residential dwellings or conversions, can be zero-rated.

For businesses dealing in these categories, careful record-keeping is paramount. Even though no VAT is charged, these transactions must be accurately reported on VAT returns to ensure correct input VAT recovery.

VAT Exemption: Outside the Scope of VAT

In stark contrast to zero-rated supplies are VAT-exempt supplies. If a good or service is VAT-exempt, it means it falls entirely outside the scope of VAT. No VAT is charged on the sale to the customer, and crucially, the business supplying the exempt good or service cannot reclaim any input VAT incurred on purchases related to that exempt supply. This distinction is perhaps the most important one to grasp when navigating VAT complexities.

When a business makes only exempt supplies, it is considered an exempt business and cannot register for VAT. This means it cannot recover any VAT on its purchases or expenses, leading to those VAT costs becoming an irrecoverable expense for the business. This can impact pricing strategies and overall profitability, as the VAT paid on inputs cannot be offset.

Common Examples of VAT-Exempt Supplies in the UK:

- Insurance, Finance, and Credit: Most financial services, including banking, loans, and insurance, are exempt from VAT.

- Education and Training: Services provided by eligible bodies, such as schools, universities, and certain vocational training, are typically exempt.

- Healthcare Services: Medical care provided by doctors, dentists, and other healthcare professionals is generally exempt, as are certain medical products.

- Charitable Fundraising Events: Specific fundraising activities undertaken by charities can be exempt.

- Subscriptions to Membership Organisations: Subscriptions to certain professional or trade bodies may be exempt.

- Selling, Leasing, and Letting of Commercial Land and Buildings: This is generally exempt, although businesses have the option to "opt to tax" these supplies, which then makes them taxable at the standard rate and allows for input VAT recovery.

- Postal Services: Services provided by the government or state-owned postal companies.

The key takeaway here is the inability to reclaim input VAT. If your business primarily deals in exempt supplies, the VAT you pay on your business purchases becomes a direct cost, potentially making your operations more expensive than if you were dealing in zero-rated or standard-rated supplies.

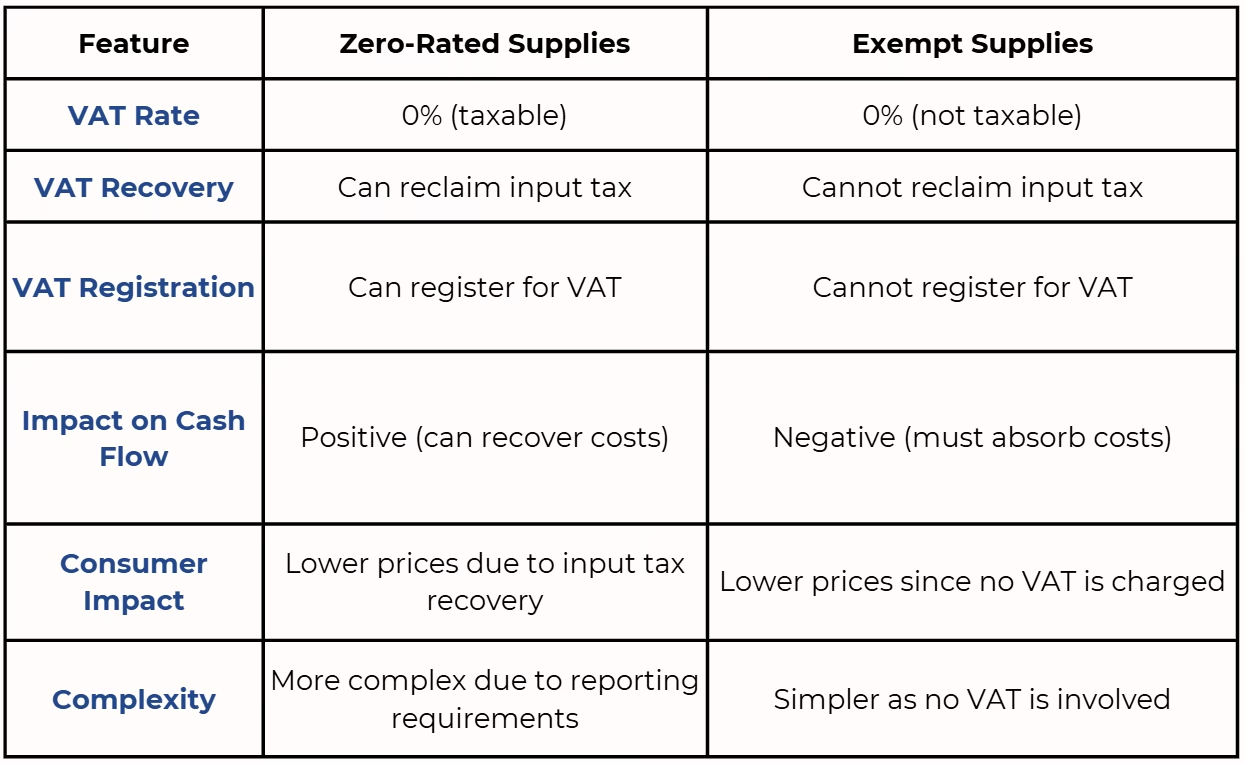

Key Differences: Zero-Rated vs. VAT-Exempt Supplies

To crystallise the distinctions, let's compare zero-rated and VAT-exempt supplies side-by-side:

| Feature | Zero-Rated Supplies | VAT-Exempt Supplies |

|---|---|---|

| VAT Rate Applied | 0% | No VAT is charged (outside the scope) |

| Taxable for VAT? | Yes, they are taxable supplies at 0% | No, they are non-taxable supplies |

| Input VAT Recovery | Yes, VAT on related purchases can be reclaimed | No, VAT on related purchases cannot be reclaimed |

| Included in Taxable Turnover? | Yes, included for VAT registration threshold calculation | No, not included in taxable turnover for registration |

| Impact on Business Costs | Can lower costs as input VAT is recoverable | Can lead to higher irrecoverable costs (hidden VAT) |

| HMRC Reporting | Must be reported on VAT returns | Not reported as VAT (but records still required) |

This table clearly illustrates the fundamental difference: the ability to reclaim input VAT. This is why understanding the correct classification of your goods and services is not just about compliance, but also about financial efficiency.

Impact on Businesses: Registration, Partial Exemption, and More

The nature of your supplies – whether zero-rated, exempt, or standard-rated – significantly impacts your business's VAT obligations and opportunities.

VAT Registration Threshold

If your business's taxable turnover (which includes zero-rated supplies but not exempt supplies) exceeds the VAT registration threshold (currently £90,000 for 2024/25, though this can change), you must register for VAT with HMRC. Businesses dealing mainly or only in zero-rated items can apply for an exemption from VAT registration if their input VAT is consistently less than their output VAT (which would be zero), though this means giving up the ability to reclaim VAT.

Partly Exempt Businesses

Many businesses provide a mix of taxable (standard-rated and zero-rated) and exempt supplies. If you incur VAT on purchases that relate to your exempt supplies, your business is considered "partly exempt." Generally, you cannot reclaim this "exempt input tax." However, there are de minimis limits: if the amount of exempt input tax is below a certain threshold, it can be recovered in full. This involves complex calculations known as partial exemption methods, often requiring careful record-keeping and potentially professional advice to ensure compliance and maximise recovery.

Capital Goods Scheme

For businesses that acquire or create expensive capital assets (e.g., land and buildings over £250,000, or single computers/equipment over £50,000), the Capital Goods Scheme might apply. This scheme requires businesses to adjust the amount of input VAT initially reclaimed over a period of 5 or 10 years, depending on the asset, if the proportion of taxable vs. exempt use of the asset changes. This adds another layer of complexity for partly exempt businesses with significant capital expenditure.

Moving Goods Between Great Britain and Northern Ireland

A specific scenario that highlights the complexities of VAT recovery arises when moving your own goods from Great Britain (England, Scotland, and Wales) to Northern Ireland. While typically the full VAT can be recovered as if it were a taxable supply, if you make exempt supplies, you may not have been able to recover some or all of the VAT on the original purchase of those goods. Moving these goods to Northern Ireland can incur a VAT charge, potentially leading to a double restriction on input tax recovery. HMRC provides a mechanism to reattribute the previously unrecovered input VAT on the original purchase to prevent this, treating the movement as a fully taxable supply for recovery purposes during your annual adjustment.

The Importance of Accurate Classification and Record-Keeping

Given the significant financial implications, accurate classification of your goods and services is paramount. Misclassifying a zero-rated supply as exempt (or vice versa) can lead to errors in your VAT returns, potential under- or over-payment of VAT, and ultimately, penalties from HMRC. For example, if you incorrectly treat a zero-rated sale as exempt, you might fail to reclaim input VAT you're entitled to, costing your business money. Conversely, incorrectly charging 0% VAT on a standard-rated item could lead to an assessment for underpaid VAT.

Maintaining meticulous records of all your sales and purchases, clearly identifying their VAT status, is not just good practice but a legal requirement. This includes invoices, receipts, and detailed breakdowns of how you've calculated your reclaimable VAT, especially if you are a partly exempt business.

Frequently Asked Questions About Zero-Rated and Exempt VAT

Navigating VAT can be challenging, so here are answers to some commonly asked questions to further clarify these concepts:

What is zero VAT?

Zero-rated VAT means that certain goods and services are technically taxable but at a rate of 0%. This means customers do not pay any VAT on these items, but the suppliers can still reclaim any VAT they paid on costs associated with providing these goods or services (input VAT).

What goods are VAT zero-rated in the UK?

Common examples of zero-rated goods in the UK include most basic foodstuffs, prescription medicines, books and educational materials, children's clothing and footwear, public transport fares, and exports. The exact list can be found in HMRC VAT notices.

What does exempt VAT mean?

Exempt VAT means that certain goods and services are not subject to Value Added Tax at all; they fall outside the scope of VAT. The seller does not charge their customers any VAT, and critically, they also cannot reclaim any VAT paid on costs directly related to providing these exempt goods or services.

What is the key difference between VAT-exempt and zero-rated?

The fundamental difference lies in input VAT recovery. Zero-rated supplies are taxable at 0%, allowing businesses to reclaim VAT on related purchases. Exempt supplies are not subject to VAT at all, meaning businesses cannot reclaim VAT paid on inputs related to these supplies.

Can you reclaim VAT on zero-rated supplies?

Yes, absolutely. Businesses can and should reclaim VAT on purchases and expenses related to zero-rated supplies. This is a key benefit of zero-rating and helps businesses reduce their overall tax liability and operating costs.

Do you charge VAT on zero-rated items?

No, you do not charge VAT on zero-rated items to your customers. The VAT rate applied is 0%, meaning the customer pays no VAT on the purchase. However, these sales must still be recorded and reported on your VAT return.

Conclusion: Mastering VAT for Business Success

Understanding the distinctions between zero-rated and VAT-exempt supplies is not just a matter of compliance; it's a strategic imperative for any business operating in the UK. While both categories mean no VAT is added to the selling price, the crucial difference in input VAT recovery can significantly impact your business's financial health, cash flow, and pricing strategy.

Zero-rated supplies, being taxable at 0%, offer the distinct advantage of allowing businesses to reclaim input VAT, effectively reducing their operating costs. Conversely, VAT-exempt supplies, being outside the scope of VAT, mean that any input VAT incurred becomes an irrecoverable cost, potentially making operations more expensive. For businesses that deal in a mix of supplies, navigating the complexities of partial exemption rules becomes essential.

The intricate nature of VAT rules, particularly when dealing with mixed supplies or specific scenarios like the Capital Goods Scheme or movements to Northern Ireland, often necessitates expert guidance. Staying informed about HMRC guidelines and seeking professional advice when in doubt can help prevent costly errors, ensure accurate VAT treatment, and ultimately contribute to the smooth and financially sound operation of your business.

If you want to read more articles similar to Zero-Rated VAT: Is It Taxable in the UK?, you can visit the Taxis category.