30/10/2021

For the dedicated taxi driver, navigating the open roads is a daily routine, but navigating the intricacies of tax can often feel like a far more challenging journey. One of the most significant areas of confusion and potential savings lies within capital allowances, particularly when it comes to the purchase of your vehicle. Understanding what you can claim, and under what conditions, is crucial for optimising your tax position and ensuring you don't pay more than you owe. This comprehensive guide aims to shed light on these complexities, offering clarity on whether your taxi purchase qualifies for substantial tax relief, including the coveted 100% allowances.

Understanding Capital Allowances for Taxis

Capital allowances are a form of tax relief that businesses can claim on certain purchases, known as 'plant and machinery'. These allowances enable you to deduct a portion of the cost of these assets from your taxable profits, thereby reducing your overall tax bill. For a taxi driver, the vehicle itself is often the most significant asset, making its capital allowance treatment a key consideration.

What are Capital Allowances?

When you buy assets for your business that you intend to keep and use for a long time, such as a taxi, you generally cannot deduct the full cost as an expense in the year of purchase. Instead, the tax system provides for capital allowances, which allow you to spread the relief over several years or, in some cases, claim a significant portion upfront. This is vital for balancing your books and accurately reflecting the wear and tear and depreciation of your business assets.

Annual Investment Allowance (AIA) vs. Writing Down Allowances (WDA)

The primary allowance many businesses aim for is the Annual Investment Allowance (AIA). This is highly attractive because it offers a 100% initial allowance on qualifying plant and machinery expenditure, up to certain monetary limits. This means you can deduct the full cost of the asset from your profits in the year you buy it, leading to a substantial immediate tax saving.

However, there's a significant catch: the Capital Allowances Act 2001 (CAA 2001, s38B) specifically excludes 'cars' from being eligible for AIA. If an asset is defined as a 'car' for capital allowances purposes, you typically have to claim Writing Down Allowances (WDA) instead. WDAs provide relief at a much slower rate, usually a percentage of the remaining value each year, making the tax benefit far less immediate.

The capital allowances treatment for cars acquired on or after 1/6 April 2009 is determined by their carbon dioxide (CO2) emissions. Cars with lower emissions may qualify for a higher WDA rate, while those with higher emissions receive a lower rate. This distinction is crucial for non-electric vehicles.

Here’s a comparison:

| Allowance Type | Key Feature | Eligibility (General) | Benefit |

|---|---|---|---|

| Annual Investment Allowance (AIA) | 100% initial allowance | Most plant and machinery, but specifically excludes 'cars' | Immediate, significant tax reduction in year of purchase |

| Writing Down Allowances (WDA) | Annual percentage deduction | Assets not eligible for AIA, including most 'cars' | Spreads tax relief over several years, less immediate impact |

The 'Car' Conundrum: HMRC's Definition

The definition of a 'car' for capital allowances purposes is not always intuitive and is central to whether you can claim AIA or are limited to WDA. CAA 2001, S268A defines a car as a mechanically propelled road vehicle other than:

- a motor cycle

- a vehicle of a construction primarily suited for the conveyance of goods or burden of any description (e.g., certain vans or pick-up trucks designed for heavy loads)

- a vehicle of a type not commonly used as a private vehicle and unsuitable for such use

It's important to note that a vehicle capable of being used as a private vehicle will be treated as a car for capital allowances purposes, regardless of how the taxpayer actually uses it. This principle was established in cases like Roberts v Granada TV Rental Ltd. Even small limousines, while not commonly used privately, are generally considered 'cars' because they are suitable for private use.

Mini-cabs and Private Hire Vehicles: The AIA Challenge

The vast majority of mini-cabs, including many multi-purpose vehicles (MPVs) often used for private hire, typically fall under the HMRC definition of a 'car'. This is primarily due to the third exclusion mentioned above: while they may not be *commonly* used as private vehicles, they are generally *suitable* for such use. For instance, an MPV used as a mini-cab can easily function as a family car. As a result, these vehicles are generally not eligible for AIA, and taxi drivers purchasing them can usually only claim Writing Down Allowances. This means the tax relief is spread out over several years rather than being available in full upfront.

The Special Case of Hackney Carriages (Black Cabs)

This is where the rules diverge significantly and offer a substantial advantage for certain taxi drivers. A traditional 'London black cab' or Hackney carriage is a unique vehicle. While it is certainly "of a type not commonly used as a private vehicle," the crucial distinction lies in whether it is also "unsuitable for such use." HMRC's manual CA23510 provides explicit guidance on this, stating that Hackney carriages should not be treated as cars for capital allowances purposes.

The design of a black cab, with its distinct turning circle, separate passenger compartment, and specific construction, makes it genuinely unsuitable for common private use. Consequently, Hackney carriages are eligible for AIA, meaning that a taxi driver who purchases a new or used black cab can claim 100% of its cost against their taxable profits in the year of purchase (up to the AIA limit). This is a substantial benefit compared to purchasing a standard car for taxi work.

Similar exclusions from the 'car' definition (and thus eligibility for AIA) apply to specific other vehicles, such as driving school cars fitted with dual controls and certain double-cab pick-up trucks that meet specific payload criteria.

Your Client's Taxi: A Practical Application

Considering your client's situation – having bought a car six months ago that is not electric – the key question is whether their vehicle qualifies as a 'Hackney carriage' in the eyes of HMRC. If their vehicle is a standard mini-cab, an MPV, or any other vehicle that could reasonably be considered 'suitable for private use', then it is highly likely to be classified as a 'car' for capital allowances purposes. In this scenario, they would typically not be eligible for AIA or any First Year Allowances (which are often reserved for new, low-emission, or electric vehicles), and would instead claim Writing Down Allowances based on the vehicle's CO2 emissions.

However, if their taxi is a traditional 'black cab' or a vehicle that explicitly meets the HMRC criteria for a Hackney carriage (i.e., not suitable for private use), then they absolutely can claim Annual Investment Allowance. This would allow them to claim 100% of the expenditure against their profits in the year of purchase, offering significant tax relief.

It is paramount for your client to determine the exact classification of their vehicle based on its design and HMRC's specific guidance to ascertain their eligibility for AIA or if they must rely on WDA.

Beyond Vehicle Purchase: Other Allowable Expenses for Taxi Drivers

While capital allowances on your vehicle are a major consideration, taxi drivers can claim a wide range of other business expenses to reduce their taxable profits. These are broadly categorised into 'simplified expenses' and 'actual expenses'.

Simplified vs. Actual Expenses: Choosing Your Path

Self-employed taxi drivers have the option to choose between two methods for claiming vehicle running costs:

- Simplified Expenses: This method allows you to claim a set amount for every mile travelled for business purposes. For the 2020-21 tax year, this was 45p per mile for the first 10,000 miles and 25p per mile for miles over 10,000. This simplifies record-keeping as it covers costs like fuel, insurance, servicing, and repairs. However, if you opt for simplified expenses for a vehicle, you cannot also claim capital allowances for that same vehicle.

- Actual Expenses: This involves meticulously recording all your actual costs related to running your taxi, such as fuel, insurance, servicing, repairs, MOTs, and loan interest if you bought the taxi with finance. This method requires more detailed record-keeping but can often lead to a higher claim, especially for more expensive vehicles with higher running costs.

Crucially, black cab drivers cannot claim for simplified expenses. Due to their commercial design and the fact they are eligible for AIA, they must always record and claim their actual costs. This reinforces the need for diligent record-keeping for black cab owners.

Here’s a simplified comparison:

| Expense Method | Description | Pros | Cons | Who Can Use It |

|---|---|---|---|---|

| Simplified Expenses | Fixed rate per business mile (e.g., 45p/25p) | Easy to calculate, minimal record-keeping | May claim less than actual costs, cannot claim capital allowances for the same vehicle | Most self-employed taxi drivers (excluding black cab drivers) |

| Actual Expenses | Record and claim all specific costs (fuel, insurance, repairs etc.) | Potentially higher claim, more accurate reflection of costs, can claim capital allowances for the vehicle | Requires detailed record-keeping (receipts, logs) | All self-employed taxi drivers (mandatory for black cab drivers) |

Key Allowable Costs to Reduce Your Tax Bill

Beyond the vehicle itself, many other expenses can be claimed. If using actual expenses, these include:

- Road Tax (Vehicle Excise Duty - VED)

- MOT fees

- Licence and registration fees (e.g., private hire or taxi licence fees)

- Business phone bills (a proportion if also used privately)

- Accountancy fees

- Cleaning costs for your vehicle

- Advertising costs

- Parking charges (for business purposes)

- Any other costs incurred wholly and exclusively for your taxi business

If you are leasing your taxi, the leasing costs can be claimed, often covering some running expenses like road tax and servicing. However, insurance and fuel are usually separate and would need to be claimed individually.

The vast majority of taxi drivers operate as self-employed 'sole traders'. This means you are responsible for calculating and paying your own tax. The main taxes you'll encounter are Income Tax and National Insurance.

Self-Assessment: Your Annual Tax Return

If your annual income exceeds the tax-free trading allowance (currently £1,000), you must complete a self-assessment tax return. This online submission details all your income (fares, tips) and your allowable expenses. The deadline for online self-assessment returns is typically 31 January following the end of the tax year (which runs from 6 April to 5 April). Missing this deadline incurs immediate fines, so timely submission is crucial.

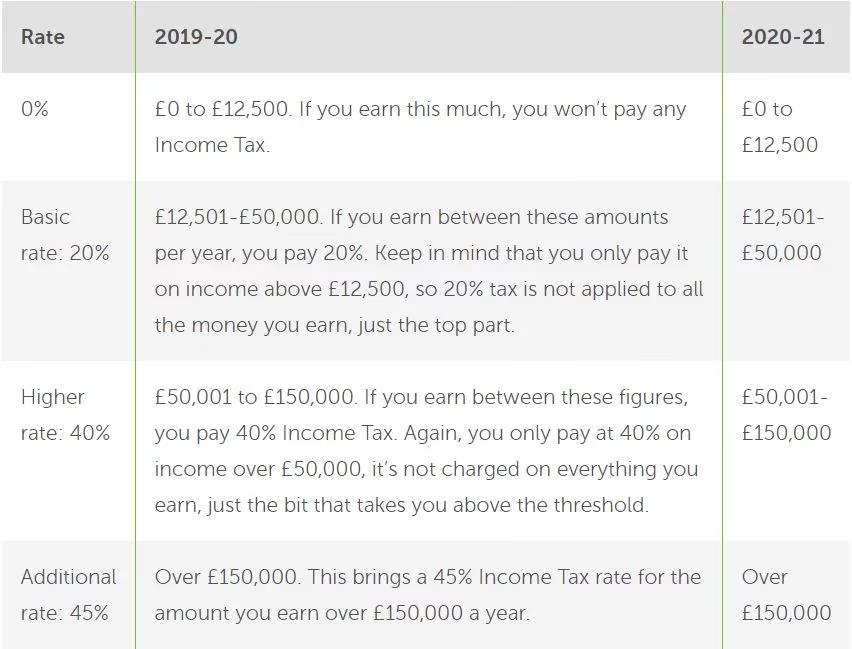

Understanding Income Tax Bands and National Insurance

Your Income Tax liability is based on your annual profit (income minus expenses). The UK operates a tiered system, with different tax rates applying to different income bands above the personal allowance (the amount you can earn tax-free). For example, a basic rate of 20% applies to income above the personal allowance up to a certain threshold, then higher rates apply to income above that. It's important to remember that these bands are incremental, meaning you only pay the higher rate on the portion of income within that band, not your entire income.

As a self-employed individual, you'll also pay National Insurance contributions, typically Class 2 and Class 4. Class 2 contributions are a fixed weekly amount (if your profits are above a certain threshold), while Class 4 contributions are a percentage of your profits above another threshold. These contributions fund certain state benefits and the State Pension.

Essential Record Keeping and Professional Advice

Accurate and meticulous record-keeping is the cornerstone of effective tax management for a taxi driver. You must keep detailed records of all your income (fares, tips) and every single expense, including receipts for fuel, repairs, insurance, and any other business costs. This will not only make completing your self-assessment tax return much easier but also ensures you can justify your claims if HMRC ever queries them.

Using accounting software or a simple, up-to-date log of money in and out can greatly simplify this process. Many digital tools are available that can help track mileage, expenses, and even integrate directly with HMRC for streamlined submission.

Given the complexities of capital allowances, the distinction between vehicle types, and the choice between expense methods, consulting an accountant is highly recommended. A professional can provide tailored advice for your specific circumstances, helping you navigate the rules, ensure compliance, and potentially identify further tax savings that you might miss. While there is a fee, the peace of mind and potential savings often far outweigh the cost.

Frequently Asked Questions (FAQs)

Q: Can I claim 100% tax relief on any taxi purchase?

A: No. While the Annual Investment Allowance (AIA) offers 100% relief on qualifying plant and machinery, 'cars' are generally excluded. Only specific types of vehicles, such as traditional Hackney carriages (black cabs), are explicitly excluded from the 'car' definition for capital allowances purposes and thus qualify for AIA. Other vehicles, like standard mini-cabs, typically only qualify for Writing Down Allowances (WDA), which spread the relief over several years.

Q: Is a mini-cab considered a 'car' for capital allowances?

A: In most cases, yes. HMRC defines a 'car' for capital allowances purposes as a mechanically propelled road vehicle, unless it's a motorcycle, primarily for goods, or a type not commonly used AND unsuitable for private use. Mini-cabs, including MPVs, are generally considered suitable for private use, even if primarily used for business. Therefore, they are usually treated as 'cars' and are not eligible for AIA.

Q: What if I use my taxi for personal travel?

A: If you use your taxi for both business and personal travel, you must accurately apportion your expenses. You can only claim the business portion of costs (e.g., fuel, insurance, repairs). If using simplified expenses, you must separate business miles from personal miles. If claiming actual expenses, you'll need to calculate the business proportion of all relevant costs.

Q: When should I register as self-employed?

A: You need to register as self-employed with HMRC by 5 October in your business's second tax year. For example, if you started driving a taxi on 1 February 2024, you would need to register by 5 October 2024. If you started after 6 April 2024, you'd register by 5 October 2025. It's often advisable to wait until you are sure your income will exceed the £1,000 trading allowance before registering.

Q: Why is it important to keep detailed records?

A: Detailed records of your income and expenses are crucial for several reasons. They allow you to accurately calculate your taxable profits, ensure you claim all eligible allowances and expenses, and provide evidence to HMRC if your tax return is ever queried. Good records simplify the self-assessment process and help you avoid overpaying tax or facing penalties.

While the world of tax can seem daunting, especially for self-employed taxi drivers, a clear understanding of capital allowances and other allowable expenses can significantly impact your profitability. The key distinction between a 'car' and a 'Hackney carriage' for tax purposes is vital for determining your eligibility for the highly beneficial 100% Annual Investment Allowance. By maintaining diligent records, understanding your options for claiming expenses, and seeking professional advice when needed, you can ensure your journey on the open road is as financially efficient as possible.

If you want to read more articles similar to Maximising Tax Relief: Capital Allowances for UK Taxis, you can visit the Taxis category.