06/04/2025

Local authorities across the United Kingdom frequently face a complex array of pressures when it comes to managing their finances, and Broxtowe Borough Council is no exception. The council finds itself navigating what has been described as a significant financial challenge, a situation compounded by a trifecta of factors that are common in the current economic landscape. Understanding these pressures is crucial for residents and stakeholders alike, as they directly influence the services provided and the financial contributions expected from the community.

The underlying issues contributing to Broxtowe Borough Council's fiscal predicament are multifaceted. Primarily, there are increasing demands for a wide range of services that local councils are statutorily obliged to provide, or that they offer to enhance the quality of life for their residents. These demands can stem from population growth, demographic shifts, or evolving societal needs. Simultaneously, the council is grappling with the pervasive issue of rising costs. Inflationary pressures, increases in energy prices, and the general uplift in the cost of goods and services – including staffing costs – mean that delivering existing services becomes progressively more expensive year on year. Compounding these expenditure pressures is the significant impact of reductions in Central Government funding. While councils historically relied heavily on central grants, these have seen real-terms decreases over recent years, placing greater onus on local revenue generation. This combination of escalating demands, soaring costs, and diminished external financial support creates a formidable obstacle to achieving a balanced budget, which is a legal requirement for all local authorities.

The Anatomy of a Council's Financial Challenge

To truly appreciate the scale of the financial challenge faced by Broxtowe Borough Council, it is important to delve deeper into each contributing factor:

Increasing Demands for Services

A local council is responsible for a vast array of services that touch almost every aspect of daily life for its residents. These can include waste collection and recycling, planning and development control, housing services, environmental health, leisure facilities, parks and open spaces, and much more. As communities grow and evolve, so too do the expectations and requirements placed upon these services. For instance, an ageing population might increase demand for certain support services, while new housing developments necessitate expanded infrastructure and public amenities. Each new demand, or increase in existing demand, places additional strain on already stretched budgets. Meeting these escalating needs requires careful strategic planning and often, difficult choices about resource allocation.

Rising Costs and Inflationary Pressures

The economic climate has a direct and profound impact on council finances. Just like households and businesses, local authorities are not immune to inflationary pressures. The cost of fuel for refuse collection vehicles, electricity for public buildings, materials for maintaining parks, and even the basic supplies needed for administrative functions, all increase over time. Furthermore, a significant portion of a council's budget is allocated to staffing costs. Maintaining competitive salaries and fulfilling pension obligations are essential for attracting and retaining skilled personnel, but these also contribute to the overall expenditure. When costs rise faster than income, a budget deficit looms large, necessitating either cuts to services or increases in local taxation.

Reductions in Central Government Funding

Historically, a substantial proportion of local government funding came from grants provided by Central Government funding. Over the past decade, however, there has been a notable shift towards greater financial self-reliance for councils. While this offers opportunities for local innovation, it also means that the real-terms value of central grants has diminished. This reduction forces councils to rely more heavily on locally generated income, such as Council Tax and business rates. When this central funding stream is reduced, particularly in an environment of rising costs and increasing demands, the pressure on the local taxpayer intensifies, and the ability to maintain or improve services becomes severely constrained.

Understanding the Council Tax Base: A Key Revenue Metric

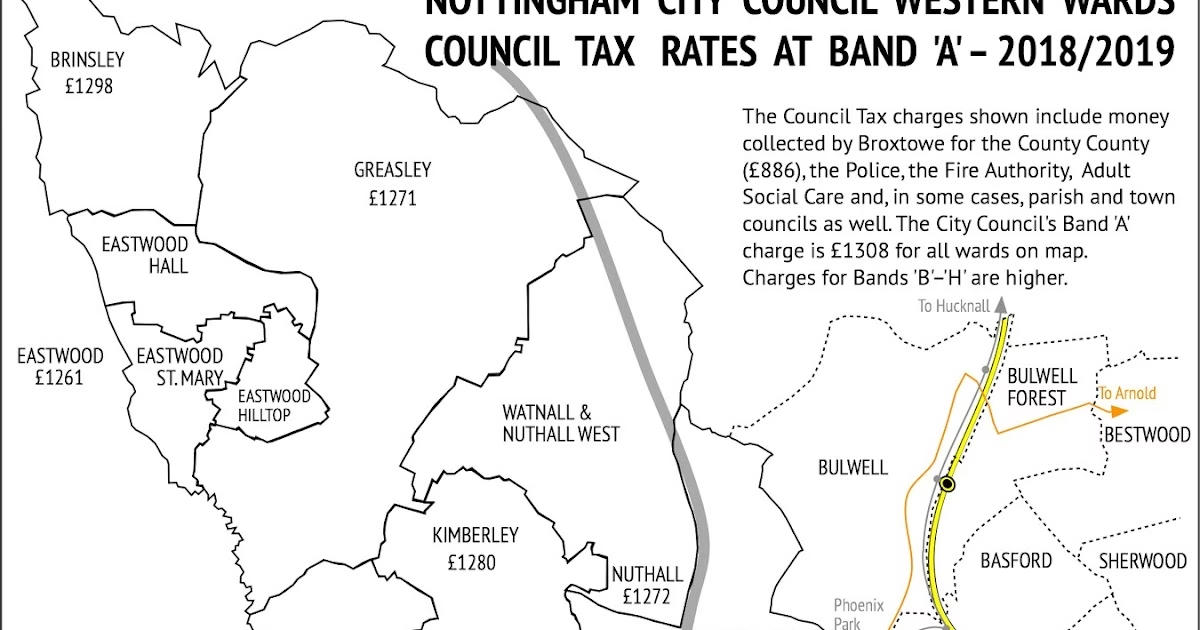

In the face of these significant financial pressures, understanding the local revenue streams becomes paramount. For Broxtowe Borough Council, as with all English councils, Council Tax is a critical component of its income. The calculation of the Council Tax Base is a fundamental step in setting the annual budget and determining the Council Tax rates for residents.

The calculated Council Tax Base for the Borough for the full year commencing 1 April 2025, assuming a collection rate of 98.5%, is 35,568.23. This figure represents the total number of Band D equivalent properties in the borough, after accounting for various discounts, exemptions, and the anticipated collection rate. It is not the actual number of properties, but a standardised measure used for calculating overall Council Tax income.

It is important to note that separate calculations have been made for the parishes and special expenses areas within the borough. This acknowledges that certain local services or amenities may be funded by specific charges levied only on residents within those particular geographical areas, beyond the standard borough-wide Council Tax. These localised calculations ensure fairness and precision in funding specific community needs.

Key Figures for the 2025/2026 Financial Year (Broxtowe Borough Council)

| Metric | Value | Notes |

|---|---|---|

| Financial Year Commencement | 1 April 2025 | The start date for the period this tax base applies to. |

| Assumed Collection Rate | 98.5% | The anticipated percentage of Council Tax that will be successfully collected. |

| Calculated Council Tax Base (Band D Equivalent) | 35,568.23 | The standardised measure for the entire Borough. |

| Additional Calculations | Separate for Parishes and Special Expenses Areas | Ensures localised funding for specific services. |

This Council Tax Base figure is a key decision point for the council, as it forms the bedrock upon which the annual Council Tax requirement is built. A higher tax base means that a lower Council Tax rate per household might be needed to raise the same amount of money, or conversely, more money can be raised at the same rate. Conversely, a lower tax base could necessitate higher individual Council Tax bills to meet budgetary needs.

Implications for Residents and Services

The ongoing financial challenges faced by Broxtowe Borough Council have direct implications for the residents and the services they receive. When budgets are tight, councils are forced to make difficult decisions. This can manifest in several ways:

- Service Reductions: Non-statutory services, or those not legally required, may face cuts or be scaled back. This could impact leisure facilities, cultural programmes, or discretionary grant funding for community groups.

- Efficiency Drives: Councils will increasingly look for ways to deliver services more efficiently, perhaps through technological adoption, shared services with other councils, or process improvements. While beneficial, these can sometimes lead to changes in service delivery methods.

- Increased Council Tax: To bridge funding gaps and meet rising costs, councils may need to increase the Council Tax levied on residents. The amount of any increase is subject to government limits and local consultation.

- Investment Delays: Major infrastructure projects or long-term investments in public assets might be delayed or postponed until financial conditions improve.

- Focus on Core Services: Resources might be prioritised towards statutory duties, such as waste collection and planning, ensuring these essential services are maintained even under pressure.

The balance between maintaining service quality, managing rising costs, and ensuring a fair contribution from residents is a delicate one. The council's ability to navigate this challenge will largely depend on its strategic planning, prudent financial management, and effective engagement with its local community.

Frequently Asked Questions About Council Finance

Given the complexities of local government finance, it's natural for residents to have questions about how their money is used and the challenges their council faces. Here are some common queries:

What does 'Band D equivalent' mean for Council Tax?

Council Tax is based on property values, with properties grouped into eight bands (A to H). Band D is used as the baseline for calculation. When a council talks about its 'Council Tax Base' in terms of 'Band D equivalent', it means they've converted all properties in different bands into a single comparable measure. For example, a Band H property might count as two Band D equivalents, while a Band A property might count as 0.67 Band D equivalents. This standardisation allows for a consistent way to calculate the total taxable capacity of an area.

Why is the Council Tax collection rate important?

The assumed collection rate, such as Broxtowe's 98.5%, is crucial because it directly impacts the council's projected income. If a council expects to collect 98.5% of the total Council Tax billed, it means 1.5% is anticipated to be uncollected due to various reasons like non-payment, empty properties, or appeals. When setting the budget, councils must be realistic about how much money they will actually receive. A lower collection rate means less income, potentially leading to a need for higher tax rates or service cuts to balance the budget.

What are 'special expenses areas'?

Special expenses areas typically refer to parts of a borough where an additional charge is levied on Council Tax bills to fund specific local services or amenities that benefit only that particular area. These can often be parish or town council precepts (an amount collected on behalf of a smaller local council) or charges for specific services like enhanced street lighting, community halls, or local parks that are not provided borough-wide. Broxtowe Borough Council's separate calculations for these areas ensure that residents only pay for the services relevant to their immediate locality, beyond the general borough-wide services.

How does 'balancing the budget' affect a council's decisions?

Local authorities in the UK have a legal duty to balance their budget each financial year. This means that their projected expenditure must not exceed their projected income. If a council faces a financial challenge, like Broxtowe, it means they have to find ways to either increase income (e.g., through Council Tax, fees, and charges) or reduce expenditure (e.g., through efficiency savings, service redesign, or service cuts) to ensure that income equals outgoings. This legal requirement drives many of the difficult decisions councils must make, especially when faced with rising costs and reduced funding.

What is the role of Central Government funding in local council budgets?

While local councils raise a significant portion of their income through Council Tax and business rates, Central Government funding traditionally provided a crucial top-up. This funding helps support a wide range of services, including those with national policy objectives. When this funding decreases in 'real terms' (meaning its purchasing power diminishes due to inflation), councils are left with a larger gap to fill from local sources. This shift has placed more financial responsibility on local taxpayers and has required councils to become more innovative in their revenue generation and cost management strategies.

In conclusion, Broxtowe Borough Council, like many local authorities, is navigating a complex and demanding financial landscape. The interplay of increasing demands for services, persistently rising costs, and a reduction in real-terms Central Government funding creates a significant challenge for balancing the budget. The careful calculation of the Council Tax Base for 2025, factoring in a robust collection rate and specific local needs, is a critical step in their ongoing efforts to ensure financial stability and continue delivering essential services to the residents of Broxtowe.

If you want to read more articles similar to Broxtowe Council's Fiscal Tightrope Walk, you can visit the Taxis category.