04/02/2026

For anyone earning a living behind the wheel of a taxi in the UK, insurance isn't merely an option; it's an absolute necessity and a complex landscape to navigate. Unlike standard private car insurance, policies for taxi drivers are specialised, reflecting the unique risks and responsibilities that come with transporting the public for 'hire and reward'. This guide delves into everything you need to know about taxi driver insurance, ensuring you're not only compliant with the law but also fully protected against the myriad of challenges the road can throw your way.

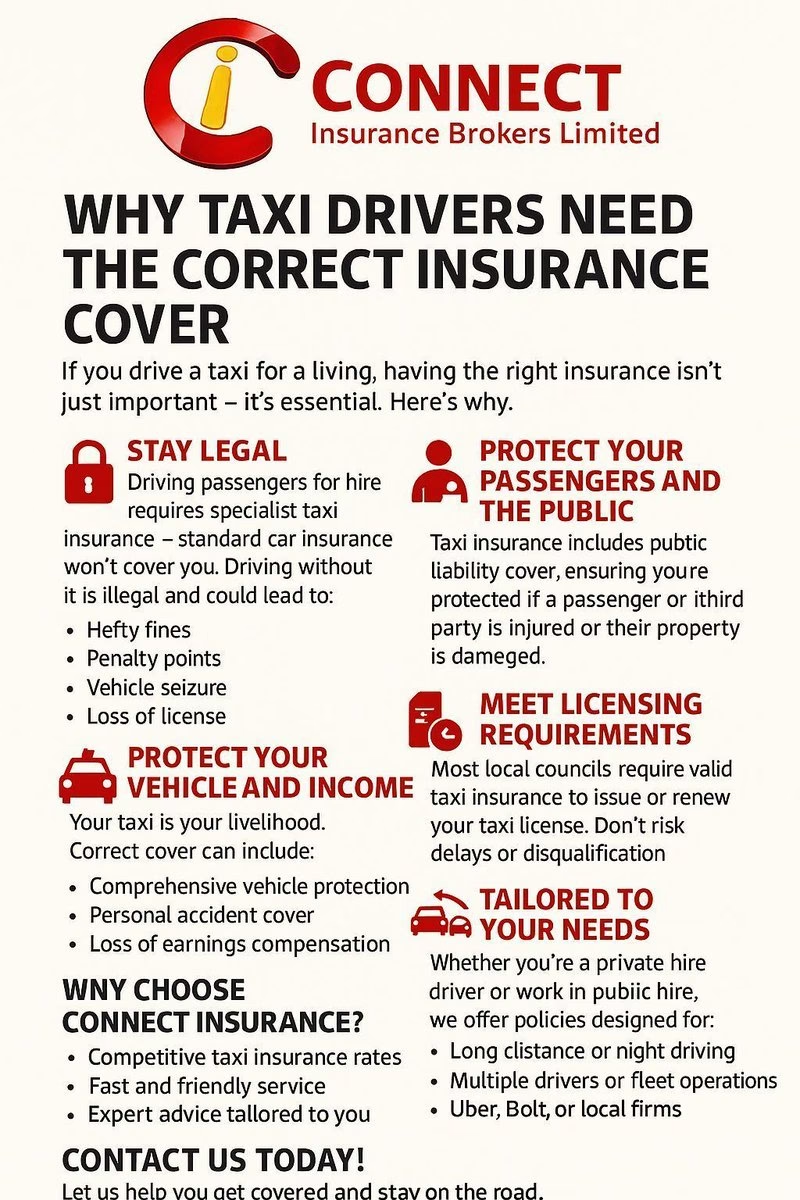

Driving a taxi means your vehicle is your livelihood, and your passengers are your priority. A standard car insurance policy simply won't cut it. It’s illegal to operate a taxi or private hire vehicle without the appropriate cover, and doing so can lead to severe penalties, including hefty fines, licence revocation, and even vehicle seizure. More importantly, it leaves you and your passengers dangerously exposed in the event of an accident or incident.

- Why Taxi Insurance Isn't Just a Legal Mandate

- Understanding the Different Types of Taxi Insurance

- Key Coverage Elements Every Taxi Driver Needs

- Navigating the Nuances: Factors Affecting Your Premium

- The Role of Specialist Support: When Accidents Happen

- Comparing Policies: What to Look For

- Frequently Asked Questions About Taxi Insurance

Why Taxi Insurance Isn't Just a Legal Mandate

Beyond the legal obligations, tailored taxi insurance provides a critical safety net for your business and personal finances. Imagine the scenario: an accident occurs, your vehicle is damaged, and you're unable to work. Without adequate cover, you face not only repair costs but also a significant loss of income. This is where the right policy becomes invaluable.

Taxi drivers have a heightened duty of care to their passengers. Should a passenger be injured while entering, exiting, or travelling in your vehicle, or should their property be damaged, your liability can be substantial. Specialist taxi insurance is designed to address these specific risks, offering peace of mind that you're protected against potential claims that could otherwise devastate your business.

Furthermore, your vehicle is on the road for extended periods, often in busy urban environments, increasing its exposure to accidents, theft, or vandalism. Comprehensive taxi insurance mitigates these financial risks, allowing you to focus on your driving and your customers rather than worrying about unforeseen incidents.

Understanding the Different Types of Taxi Insurance

The UK taxi industry broadly categorises vehicles into two main types, each requiring a specific kind of insurance policy:

Public Hire Insurance (Black Cab Insurance)

This is typically for Hackney Carriages, commonly known as black cabs, which can be hailed from the street, picked up from taxi ranks, or pre-booked. These vehicles often have specific licensing requirements and are easily identifiable. Public hire insurance is tailored to cover the unique operational aspects of these vehicles, including the ability to pick up passengers spontaneously.

Private Hire Insurance (Minicab Insurance)

Private hire vehicles, or minicabs, operate exclusively on a pre-booked basis. They cannot be hailed from the street or wait on taxi ranks. This category includes vehicles working for app-based services like Uber, Bolt, or traditional private hire companies. Private hire insurance reflects the nature of pre-arranged journeys and the associated risks.

While both fall under 'hire and reward', the subtle differences in operation dictate the specific policy needed. It's crucial to ensure you have the correct type of insurance for your operating licence.

| Feature | Public Hire Insurance | Private Hire Insurance |

|---|---|---|

| Booking Method | Can be hailed, from ranks, or pre-booked | Must be pre-booked only |

| Vehicle Type | Often traditional Hackney Carriages | Wider range of standard vehicles |

| Flexibility | More flexible in picking up passengers | Strictly pre-arranged journeys |

| Cost Factors | Often higher due to street hailing exposure | Varies based on operator and location |

| Licensing | Specific Hackney Carriage licence | Specific Private Hire Vehicle licence |

Key Coverage Elements Every Taxi Driver Needs

Just like standard car insurance, taxi policies come in different levels of cover, but with additional specialised components:

Third-Party Only (TPO)

This is the minimum legal requirement. It covers damage or injury to other people, their vehicles, or property if you're at fault in an accident. It does not cover any damage to your own taxi.

Third-Party, Fire & Theft (TPFT)

In addition to TPO cover, this policy protects your vehicle against fire damage and theft.

Comprehensive Taxi Insurance

This is the most extensive level of cover. It includes TPO and TPFT, plus it covers damage to your own vehicle, even if the accident was your fault. It often includes cover for personal injury to you and your passengers, too. For a taxi driver, comprehensive cover is almost always the recommended option to protect your valuable asset and livelihood.

Public Liability Insurance

Beyond road traffic accidents, this is incredibly important. Public liability insurance protects you against claims made by passengers or members of the public for injuries or damage to property that occurs outside of a road traffic accident. For example, if a passenger slips on a wet pavement while exiting your vehicle and injures themselves, or if their luggage is damaged while you're loading/unloading it. This is a crucial addition that goes beyond standard motor insurance and provides essential public liability protection.

Breakdown Cover

A non-operational taxi means lost earnings. Integrated breakdown cover ensures prompt assistance if your vehicle breaks down, getting you back on the road faster or arranging recovery.

Loss of Earnings Cover

If your taxi is off the road due to an accident or theft, this cover provides compensation for the income you lose during that period. This is vital for maintaining your financial stability and is often referred to as loss of earnings cover.

Legal Expenses Cover

This covers the legal costs incurred in pursuing or defending a claim related to an accident, such as recovering uninsured losses from an at-fault driver or defending against a claim made against you.

| Coverage Type | What it Protects | Why it's Important for Taxi Drivers |

|---|---|---|

| Third-Party Only | Others' vehicles, property, and injuries | Legal minimum, but leaves your vehicle exposed |

| Comprehensive | All of the above + damage to your own taxi | Maximum protection for your primary business asset |

| Public Liability | Passenger/public injury/damage (non-RTA) | Crucial for incidents outside of road accidents |

| Loss of Earnings | Your income when your taxi is off the road | Sustains your livelihood during repairs/replacement |

| Breakdown Cover | Vehicle breakdowns and recovery | Minimises downtime and lost income |

| Legal Expenses | Costs of legal representation for claims | Helps manage complex accident-related legal processes |

Several factors influence the cost of your taxi insurance premium:

- Driver's Age and Experience: Younger or less experienced drivers typically face higher premiums.

- Driving History: A clean driving record with no claims or endorsements will result in lower costs. A good no-claims bonus is highly beneficial.

- Vehicle Type: The make, model, age, and value of your taxi will affect the premium. More powerful or expensive vehicles usually cost more to insure.

- Operating Location: Premiums can vary significantly depending on whether you operate in a high-risk urban area or a quieter rural location.

- Annual Mileage: The more miles you drive, the higher the risk, and potentially the higher your premium.

- Excess Levels: Opting for a higher voluntary excess can reduce your premium, but ensure you can afford to pay it in the event of a claim.

- Security Measures: Installing approved security devices in your vehicle can sometimes lead to discounts.

The Role of Specialist Support: When Accidents Happen

Even with the most comprehensive insurance, accidents can still occur. For taxi drivers, the aftermath can be particularly complex due to the involvement of passengers, the need for a replacement vehicle to maintain income, and the often intricate process of recovering losses. This is where specialist support and claims management services become invaluable.

In the unfortunate event of a road traffic accident, particularly for taxi drivers, the aftermath can be complex. Beyond vehicle repairs and personal injury, there's the critical need for a replacement vehicle to maintain income. This is where specialist teams become invaluable. Companies like Connect Claims, with main offices in London and regional offices in Harrogate, Leeds, and Greater Manchester, offer dedicated support for personal injury claims resulting from road traffic accidents. They work alongside specialist solicitors to ensure drivers, and even innocent passengers, receive the compensation they deserve. Crucially for taxi drivers, they can assist with securing a replacement taxi-plated vehicle, ensuring minimal disruption to your livelihood. They also support Credit Hire Organisations in recovering outstanding charges, streamlining the process for all involved.

Such services can alleviate the stress and administrative burden, allowing you to focus on your recovery and getting back to work.

Comparing Policies: What to Look For

When obtaining quotes for taxi insurance, don't just focus on the price. A cheaper policy might have significant exclusions or a higher excess that could leave you exposed. Always consider:

- Policy Limits: Ensure the cover limits are adequate for your needs, especially for public liability.

- Exclusions: Carefully read the small print for any exclusions that might affect your specific operations.

- Add-ons: Check if essential add-ons like breakdown cover or loss of earnings are included or need to be purchased separately.

- Reputation of the Insurer: Research the insurer's customer service and claims handling reputation.

- Excess Levels: Understand both the compulsory and voluntary excesses you would need to pay.

Comparing quotes from multiple specialist taxi insurance brokers is always recommended to find the best balance of cover and cost.

Frequently Asked Questions About Taxi Insurance

Is taxi insurance different from standard car insurance?

Yes, absolutely. Standard private car insurance explicitly excludes 'hire and reward' use. Taxi insurance is a specialist policy designed to cover the unique risks of carrying paying passengers and is a legal requirement for taxi drivers.

What is a 'no-claims bonus' for taxi drivers?

Similar to private car insurance, a no-claims bonus (NCB) or no-claims discount (NCD) is a reduction in your premium for each year you drive without making a claim. Accumulating a good no-claims bonus can significantly lower your taxi insurance costs.

Do I need public liability insurance if I have comprehensive taxi insurance?

While comprehensive motor insurance covers incidents directly related to the driving of the vehicle (road traffic accidents), public liability insurance typically covers non-motor-related incidents where a member of the public (including passengers) might be injured or suffer damage to their property due to your business activities. For example, if a passenger trips and falls on the pavement after exiting your taxi, public liability would cover that, whereas comprehensive motor insurance might not. It's highly recommended to have both.

Can I get temporary taxi insurance?

Some specialist providers do offer temporary taxi insurance policies, which can be useful for short-term cover, such as when borrowing a vehicle or for specific events. However, these are less common for full-time taxi drivers who require continuous, long-term cover.

What happens if I have an accident and it's not my fault?

If you're involved in an accident that isn't your fault, your insurer or a specialist claims management company (like Connect Claims) can help you recover costs from the at-fault party's insurer. This can include vehicle repairs, a replacement taxi-plated vehicle (known as credit hire), and any loss of earnings you incur while your vehicle is off the road.

Navigating the roads as a taxi driver is a demanding profession, and having the right insurance is fundamental to your success and peace of mind. By understanding the different types of cover available, the factors influencing your premium, and the importance of specialist support, you can ensure your livelihood, your vehicle, and your passengers are always adequately protected. Don't compromise on your cover; it's an investment in your future on the bustling streets of the UK.

If you want to read more articles similar to Essential Taxi Driver Insurance Guide UK, you can visit the Insurance category.