01/05/2026

In recent years, the landscape of work has undergone a significant transformation, with a booming gig economy making flexible roles, such as those of a courier or delivery driver, increasingly popular across the UK. Whether you're delivering piping hot takeaways, essential parcels, or bespoke goods, the convenience and autonomy of being your own boss, or working for a platform, are undeniable. However, with this flexibility comes a crucial responsibility: ensuring you have the correct and comprehensive insurance cover. This isn't just a recommendation; it's a legal necessity that protects you, your vehicle, and your livelihood. Without the right policy, you could find yourself in a precarious position, facing significant financial penalties and legal repercussions.

What Exactly is Courier Car Insurance?

At its core, courier car insurance is a specialised form of vehicle insurance designed for individuals who use their personal car to transport goods for payment. It goes by several names, including 'Carriage of Goods for Hire and Reward' insurance or 'Food Delivery Car Insurance,' depending on the specific nature of your delivery work. Unlike standard private car insurance, which covers personal use only, courier car insurance explicitly provides protection for you and your vehicle when you are actively engaged in making deliveries for a fee. This distinction is paramount because standard policies contain clauses that invalidate your cover if you use your vehicle for commercial purposes without the appropriate endorsement.

The fundamental purpose of this insurance is to bridge the gap between private vehicle use and commercial operations. If you're delivering goods, parcels, or fast food on behalf of someone else, whether it's a local restaurant, a national logistics firm, or a popular app-based platform, this specific type of policy ensures you are legally and financially protected. It acknowledges the increased risks associated with commercial driving, such as higher mileage, more frequent stops, and the potential for carrying valuable goods, and provides the necessary safeguards that a standard policy simply cannot.

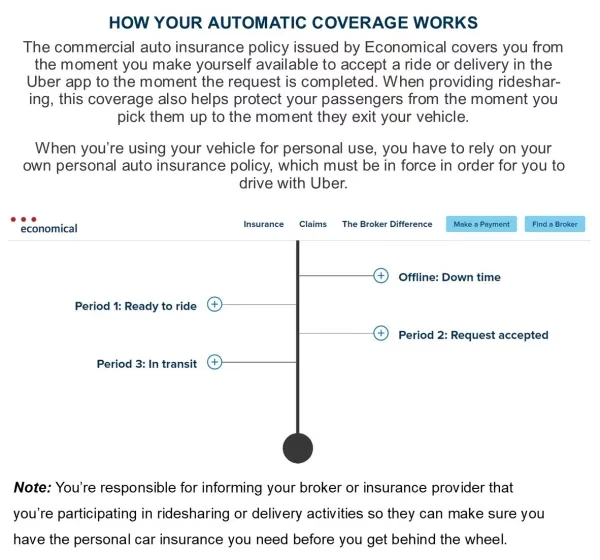

The Critical Divide: Private vs. Courier Car Insurance

Understanding the fundamental difference between private car insurance and courier car insurance is not just important; it's absolutely vital for anyone considering or currently undertaking delivery work. Many individuals mistakenly believe their existing private car policy will suffice, leading to potentially devastating consequences. The truth is, standard private car insurance is specifically designed for 'social, domestic, and pleasure' use, often including commuting to a single place of work. It explicitly excludes any form of 'hire and reward' activity.

When you use your personal car to perform courier duties – meaning you are transporting goods in exchange for payment – you are legally required to have 'hire and reward' insurance. This is because the nature of the risk changes dramatically. A private vehicle typically covers fewer miles, operates during less congested hours, and carries no commercial goods. A courier vehicle, by contrast, covers significantly more ground, often operates during peak times (lunch, dinner, rush hour), and is responsible for the safe delivery of items that have a monetary value. Insurers view these as entirely different risk profiles. If you were involved in an accident while making a delivery and only had private car insurance, your policy would likely be invalidated. This means your insurer would refuse to pay out for any damages or injuries, leaving you personally liable for potentially enormous costs, including vehicle repairs, third-party claims, and legal fees. Furthermore, driving without the correct insurance is a serious offence, carrying penalties such as points on your licence, a substantial fine, or even disqualification from driving.

The allure of flexible work as a courier is strong, offering an attractive prospect for those seeking an extra source of income or even a main livelihood. Companies like Amazon Flex, Deliveroo, and Uber Eats rely on individuals with their own transport. However, it's crucial to remember that your own transportation, while convenient, must be adequately insured for the specific work you undertake. A dedicated courier car policy gives you that comfort and peace of mind, knowing you have the right level of protection in place, ensuring you're covered if something goes wrong along the way.

Comprehensive Cover: Beyond the Basics for Couriers

While 'hire and reward' insurance is the absolute legal minimum for couriers, experienced drivers and smart business owners understand that full protection often requires additional layers of cover. These supplementary policies address other facets of risk inherent in delivery work, providing a robust safety net.

- Goods in Transit Insurance: This is arguably the most crucial additional cover for any courier. While 'hire and reward' protects your vehicle and your liability for accidents, it does not typically cover the items you are transporting. Goods in Transit insurance protects the parcels, food, or other items you are delivering from loss, damage, or theft while they are in your care. Imagine a scenario where a box of expensive electronics is damaged in a sudden brake, or a food order is spilled due to an unexpected jolt. Without Goods in Transit cover, you could be personally liable for the cost of replacement, directly impacting your earnings and reputation. This policy is essential for safeguarding your income and building trust with clients.

- Public Liability Insurance: As a courier, you interact with the public and visit various properties on a daily basis. Public Liability insurance covers you if you accidentally injure someone or damage property while on the job. For example, if you trip and spill a drink on a customer's expensive carpet, or if you accidentally knock over a valuable ornament while entering a building, this policy would cover the costs of compensation and legal fees. It's a vital safeguard against unforeseen accidents that can occur at delivery addresses.

- Employers' Liability Insurance: If you're growing your courier business and employ other drivers, Employers' Liability insurance becomes a legal requirement in the UK. This policy protects you against claims from employees who suffer injury or illness as a result of their work for you. It's a non-negotiable cover for businesses with staff, ensuring you comply with UK employment law and protect your team.

- Legal Expenses Insurance: This optional but highly recommended cover helps with the costs of legal advice and representation if you are involved in a dispute related to your courier work that isn't covered by other parts of your policy. This could include disputes over contracts, or if you need to defend yourself against charges arising from an accident.

- Breakdown Cover: While not strictly an insurance, robust breakdown cover is paramount for couriers. Your vehicle is your office, and any downtime directly impacts your earnings. Dedicated commercial breakdown cover often offers faster response times and caters to the specific needs of business vehicles, ensuring you're back on the road swiftly.

- Excess Protection: This optional add-on covers the cost of your insurance excess in the event of a claim. If you have a high excess to keep your premiums down, this can be a valuable addition, preventing a significant out-of-pocket expense after an incident.

By combining these covers, self-employed couriers, those working for delivery platforms, or small fleet operators can ensure they have comprehensive protection against the diverse risks inherent in their profession. It pays to understand the differences and invest in the right combination of policies to stay compliant and secure.

The Unseen Risks: Why Skipping Courier Insurance is a Costly Gamble

The temptation to save money by avoiding specialised courier insurance might seem appealing at first glance, but the potential consequences far outweigh any short-term savings. Ignoring the legal requirement for 'hire and reward' cover is not merely a technicality; it's a profound risk to your financial stability, legal standing, and even your ability to continue working as a courier. Let's delve deeper into the ramifications:

- Policy Invalidation: As previously mentioned, this is the most immediate and severe consequence. If you're involved in an accident while making a delivery without the correct 'hire and reward' cover, your private insurance policy will be void. This means your insurer will not pay for any damages to your vehicle, the other party's vehicle, or any injuries sustained. You become personally responsible for all costs, which can quickly run into tens or even hundreds of thousands of pounds.

- Legal Penalties: Driving without valid insurance is a serious offence in the UK. You could face a fixed penalty of £300 and 6 penalty points on your licence. If the case goes to court, you could receive an unlimited fine and be disqualified from driving. For a courier, losing your licence means losing your livelihood.

- Vehicle Seizure: In some cases, the police have the power to seize your vehicle if they find you are driving without valid insurance. This adds further inconvenience and cost, as you would need to pay to retrieve your vehicle after proving you have obtained proper insurance.

- Loss of Earnings: An invalidated policy and subsequent legal issues or vehicle seizure will inevitably lead to a halt in your ability to work. This means a direct loss of income, potentially for an extended period, while you resolve the situation.

- Reputational Damage: For self-employed couriers, your reputation is everything. Being involved in an incident without proper insurance can severely damage your standing with clients and platforms, making it difficult to secure future work.

- Personal Liability: If you cause an accident resulting in significant damage or injury to a third party, and your insurance is invalid, you will be personally liable for compensation. This could mean years of financial struggle, potentially forcing you into bankruptcy.

Investing in the correct courier car insurance is not an expense; it's an investment in your future, your business, and your security. It provides the peace of mind that allows you to focus on your deliveries, knowing you're protected against the unforeseen.

While separate from your primary insurance, robust breakdown cover is an indispensable asset for any courier or delivery driver. Your vehicle is your primary tool, and any downtime due to a breakdown directly impacts your ability to earn. Unlike standard personal breakdown cover, commercial breakdown services are often tailored to the demands of professional drivers, understanding the urgency of getting you back on the road.

Many providers offer specialist breakdown cover for business vehicles, including cars used for courier work and delivery vans. It's important to note that if you have a Heavy Goods Vehicle (HGV) or a vehicle weighing more than 3.5 tonnes, you would typically need a specific 'pay as you go truck cover' or similar, as standard courier breakdown policies usually cater to lighter commercial vehicles. VAT is not always charged on specialist breakdown cover, which can be a small saving for businesses.

When setting up a business account for breakdown cover, the process is usually straightforward. Your account can be set up as soon as you provide your details and payment. However, it's crucial to remember that your cover won't start until you've sent your vehicle number plate details. Additionally, there's often a waiting period before you can make a claim; typically, you can make a claim 24 hours after your cover starts or after you add vehicle details. This prevents immediate claims right after sign-up for pre-existing issues.

Most breakdown services for couriers will provide a membership card. This card usually has the telephone number for your driver to call in a breakdown situation, and quoting your card number helps the service find your details on their system quickly. You'll also likely need to show a valid card when the patrol arrives. You should typically receive your breakdown card around 7 days after your account is opened.

A common concern for couriers is what happens if a part is needed during a breakdown. Unless alternative arrangements have been made before the callout, the driver would usually have to pay for the part there and then. This highlights the importance of regular vehicle maintenance to minimise such occurrences.

Furthermore, if you sell one of your covered vehicles mid-way through your breakdown cover period, most providers allow you to add another vehicle in its place at any point up to the renewal of your cover. However, if a replacement vehicle isn't allocated, you typically won't be able to get a refund or credit for the unused portion of the policy. This flexibility is key for couriers who frequently update or change their delivery vehicles.

Comparing Your Options: Private vs. Courier Insurance at a Glance

| Feature | Private Car Insurance | Courier Car Insurance |

|---|---|---|

| Purpose | Social, domestic, pleasure, commuting to one place of work. | Transporting goods for hire or reward (payment). |

| Legality for Courier Work | Illegal and invalidates policy. | Legally Required for any paid delivery work. |

| Coverage Scope | Covers personal use only. | Covers commercial use, including higher mileage and frequent stops. |

| Risk Profile | Lower risk; fewer miles, less exposure. | Higher risk; increased mileage, more stops, carrying goods. |

| Key Inclusions (Base) | Third Party Only, Third Party Fire & Theft, Comprehensive. | Hire & Reward cover. |

| Recommended Add-ons | Breakdown, Legal Expenses. | Goods in Transit, Public Liability, Breakdown, Legal Expenses, Employers' Liability (if applicable). |

| Consequences of Misuse | Policy invalidation, fines, points, vehicle seizure, personal liability. | Appropriate cover for legal compliance and peace of mind. |

Frequently Asked Questions About Courier Car Insurance

Navigating the nuances of insurance can be complex, so here are some common questions couriers often ask to help clarify your understanding:

Q: Can I just add 'business use' to my private car insurance for courier work?

A: No, simply adding 'business use' to a standard private car policy is generally not sufficient for courier or delivery work. 'Business use' typically covers things like driving to multiple business premises for meetings, or using your car for administrative tasks related to a business. It does not cover 'hire and reward,' which is the legal term for carrying goods for payment. For courier work, you specifically need a 'hire and reward' policy.

Q: What is 'hire and reward' insurance, and why is it so important?

A: 'Hire and reward' insurance is a specific type of cover that permits you to legally carry goods or passengers in exchange for payment. It's crucial because without it, your standard private car insurance policy becomes invalid when you are making deliveries. This means you would be driving uninsured, facing severe legal penalties and financial liability in the event of an accident.

Q: Do I really need Goods in Transit insurance if I have courier car insurance?

A: While courier car insurance covers your vehicle and your liability for accidents, it typically does not cover the items you are delivering. Goods in Transit insurance is a separate policy that protects the parcels, food, or other goods from loss, damage, or theft while they are in your care. It's highly recommended, as it protects your earnings and reputation by covering the cost of replacing damaged or lost items.

Q: What happens if I break down during a delivery?

A: If you have commercial breakdown cover, you should call the number provided on your breakdown card. They will dispatch assistance. Be aware that most commercial breakdown policies have a waiting period (often 24 hours) from when your cover starts or when you add a vehicle before you can make a claim. If a part is needed, you might have to pay for it on the spot unless pre-arranged.

Q: How quickly can I get courier car insurance cover?

A: Many providers offer instant online quotes and immediate cover once you've completed the application and payment. However, always ensure you have received confirmation and all necessary documentation before you start making deliveries.

Q: What if I sell one of my delivery vehicles mid-way through my policy period?

A: Most courier insurance and breakdown policies allow you to transfer the cover to a replacement vehicle. You would typically need to inform your insurer and provide the new vehicle's details. If you don't replace the vehicle, it's unlikely you'll receive a refund or credit for the remaining period of cover, so it's best to allocate a replacement if possible.

Q: Is courier car insurance more expensive than private car insurance?

A: Generally, yes. Due to the increased risk associated with commercial driving – higher mileage, more time on the road, operating in busier areas, and carrying goods – courier car insurance premiums are typically higher than those for private use. However, the cost is a necessary investment to ensure legal compliance and comprehensive protection.

Conclusion: Drive Protected, Deliver with Confidence

The rise of the delivery economy has opened up new avenues for flexible work, but it has also highlighted the critical importance of specialised insurance. For any individual using their car for courier or delivery services in the UK, obtaining the correct 'hire and reward' car insurance is not merely an option; it is a fundamental legal requirement. Without it, you expose yourself to severe financial penalties, legal repercussions, and the complete invalidation of any existing private car insurance. Beyond the mandatory cover, considering additional policies such as Goods in Transit and Public Liability insurance provides a robust shield, protecting not only your vehicle but also the goods you carry and your interactions with the public. Investing in the right insurance is an investment in your livelihood, your peace of mind, and your future. Ensure you are fully covered, drive protected, and deliver with absolute confidence.

If you want to read more articles similar to Courier Car Insurance: Your Essential UK Guide, you can visit the Insurance category.