22/07/2023

Discovering you’ve been a victim of card fraud can be a deeply unsettling experience, leaving you feeling vulnerable and unsure of the next steps. Whether your credit or debit card has been used without your permission, or your details have been compromised, acting immediately is paramount. Swift action can significantly improve your chances of recovering lost funds and preventing further financial damage. This comprehensive guide will walk you through what plastic card fraud entails, what you should do if you become a victim, understand your rights regarding refunds, and how to protect yourself in the future.

The digital age, while offering immense convenience, also presents new avenues for fraudsters. Understanding the landscape of card fraud and equipping yourself with the knowledge to respond effectively is your strongest defence. Don't panic; instead, empower yourself with the information to navigate this challenging situation.

- What is Plastic Card Fraud?

- Immediate Steps After Discovering Card Fraud

- Understanding Your Rights: When Banks Can Refuse a Refund

- The Role of the Financial Ombudsman Service (FOS)

- Preventing Card Fraud: Your Best Defence

- Reporting Fraud or Corruption Against TfL

- Immediate Actions: Stolen Card vs. Compromised Details

- Frequently Asked Questions (FAQs)

What is Plastic Card Fraud?

Plastic card fraud encompasses any unauthorised use or compromise of personal information associated with your credit, debit, or store cards. It's not just about the physical theft of your card; often, the fraud occurs even when your card remains in your possession. Fraudsters are ingenious in their methods, constantly evolving to exploit vulnerabilities.

Typically, card fraud involves the theft of sensitive information such as your card number, expiry date, and the three-digit security code (CVV/CVC) on the back. This information can be obtained through various means:

- Skimming: Devices illegally attached to card readers at ATMs, petrol pumps, or point-of-sale terminals, which copy card data.

- Phishing: Deceptive emails, text messages, or phone calls designed to trick you into revealing your card details or other personal information by impersonating legitimate organisations like your bank or a well-known retailer.

- Malware: Malicious software installed on your computer or phone that can capture keystrokes or access sensitive data.

- Data Breaches: When a company's database, containing customer card details, is hacked.

- Physical Theft: The actual theft of your card, which can then be used for unauthorised purchases, often through contactless payments or online transactions if the fraudster also obtains other details.

- Account Takeover: Fraudsters gain access to your online banking or shopping accounts, changing details and making purchases.

Once obtained, this stolen information can be used to make unauthorised purchases online, over the phone, or even to create counterfeit cards. The goal is always the same: to purchase goods in your name or obtain unauthorised funds from your account, leaving you out of pocket and potentially facing significant hassle.

Immediate Steps After Discovering Card Fraud

When you suspect or confirm card fraud, your response time is critical. Every minute counts. Follow these steps without delay:

Contact Your Bank or Card Provider Immediately

This is the absolute first step. Most banks have dedicated 24/7 fraud hotlines. You'll find the number on the back of your card, on your bank's official website, or on your bank statements. Explain the situation clearly, detailing any suspicious transactions you've identified.

Block or Cancel the Compromised Card

When you contact your bank, they will guide you through the process of blocking or cancelling the card. This prevents any further unauthorised transactions from being made using that card's details. A new card will typically be issued to you.

Review Your Account Statements Thoroughly

Go through all your recent transactions, not just on the compromised card but on all your accounts. Fraudsters often test small transactions first. Look for anything you don't recognise, no matter how small. Make a list of all fraudulent transactions, including dates, amounts, and merchant names.

Report the Fraud to Action Fraud

Action Fraud is the UK's national reporting centre for fraud and cyber crime. While your bank handles the financial aspects, reporting to Action Fraud helps law enforcement build a picture of fraud activity, identify trends, and potentially bring offenders to justice. You can report online or by calling 0300 123 2040. You will receive a crime reference number, which can be useful for your bank and for insurance purposes.

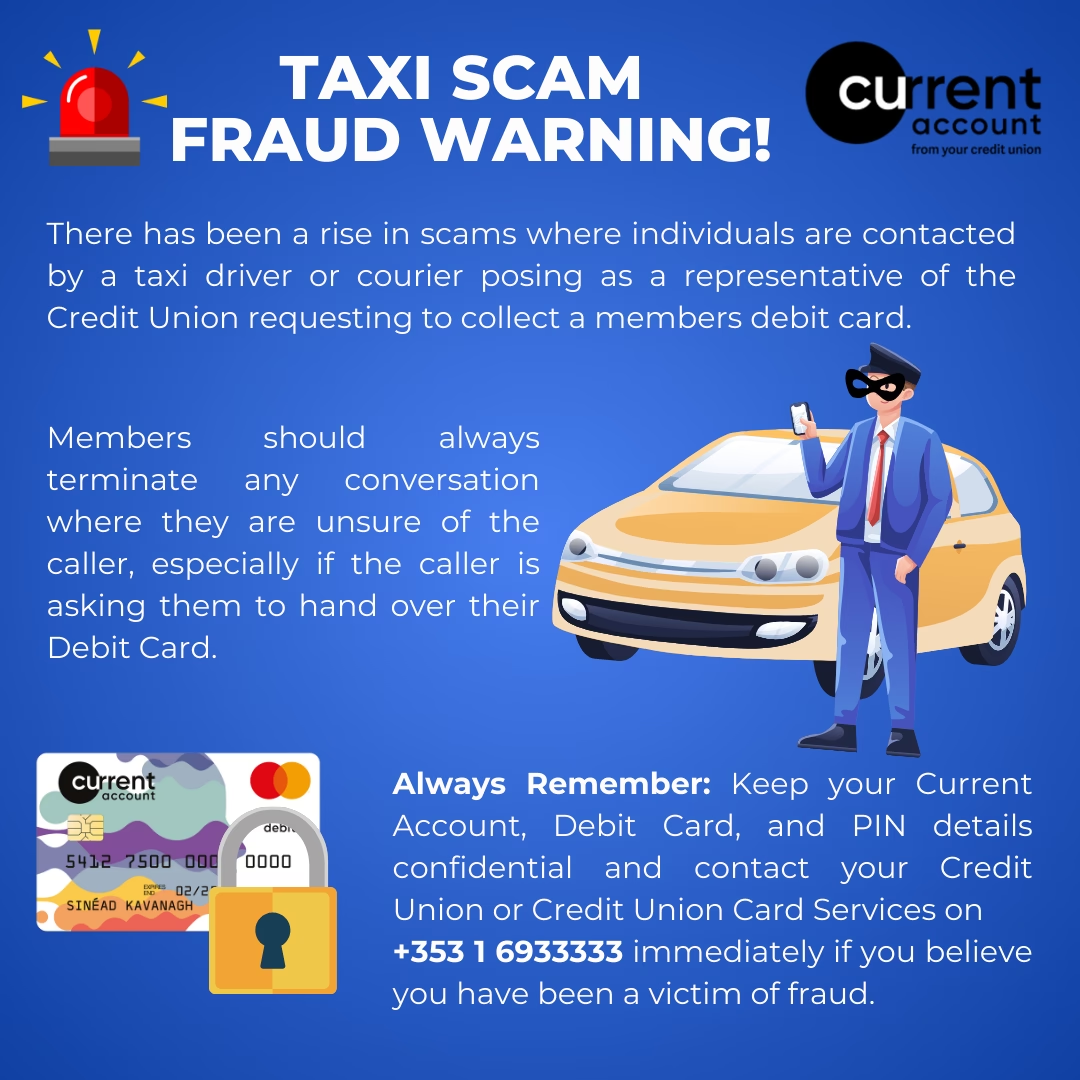

A scam taxi is altered or modified to charge a customer unfairly. There are two main types: one involving a taxi driver and one involving a driver and another passenger. The two-person scam usually involves two people pretending to argue. The “passenger” claims to be unable to pay their fare and asks bystanders to help. Keep Detailed Records

Maintain a meticulous record of everything related to the fraud. This includes:

- Dates and times of all phone calls with your bank and Action Fraud.

- Names of the people you spoke to.

- Reference numbers provided by your bank and Action Fraud.

- Copies of any correspondence (emails, letters).

- Your list of fraudulent transactions.

These records will be invaluable if there are any disputes or if you need to escalate your case.

Change Relevant Passwords

If you suspect your details were compromised online, change passwords for your online banking, email, and any other accounts where you might have saved card details. Use strong, unique passwords for each account.

Understanding Your Rights: When Banks Can Refuse a Refund

Under the Payment Services Regulations 2017 (for debit cards) and the Consumer Credit Act 1974 (for credit cards), you have significant protections against unauthorised payments. Generally, if an unauthorised payment is made from your account, your bank or card provider must refund you. However, there are specific circumstances where they might be able to refuse a refund:

If you genuinely authorised the payment, but now suspect you’ve sent money to a scammer (known as Authorised Push Payment, or APP, fraud), the situation can be more complex. While your bank can initially refuse a refund if you authorised it, new voluntary codes like the Contingent Reimbursement Model (CRM) Code are in place. This code commits participating banks to reimburse victims of APP fraud, provided the customer was not grossly negligent. The bank must investigate thoroughly to determine if you were duped into authorising the payment and whether they did enough to protect you.

You Acted Fraudulently

If the bank can prove that you acted fraudulently – for example, by fabricating a claim or colluding with the fraudster – they can refuse a refund. This is a high bar for the bank to prove.

You Failed to Protect Your Card Details, PIN, or Password

Your bank can refuse a refund if they can demonstrate that you failed to take reasonable steps to protect the security of your card details, PIN, or password, and this failure allowed the payment to occur. Examples might include writing your PIN on your card, sharing your PIN or password with someone else, or leaving your card unattended in an easily accessible place. However, the use of your password, card, or PIN might not on their own be sufficient proof that you authorised a payment or were grossly negligent. The bank must show a clear link between your negligence and the fraudulent transaction.

For unauthorised payments made on a credit card, or from an overdrawn account, the rules are slightly different. Your bank can only refuse a refund if you, or someone acting on your behalf, authorised the payment, or if the person who used your payment card (including virtual cards) had it with your consent. This provides a strong layer of protection for credit card users, as the Consumer Credit Act offers joint liability with the retailer for purchases over £100.

The Role of the Financial Ombudsman Service (FOS)

If you've reported card fraud to your bank and are unhappy with their final decision or the way your complaint has been handled, you have the right to escalate your case to the Financial Ombudsman Service (FOS). The FOS is an independent, free service that helps resolve disputes between consumers and financial businesses.

Before contacting the FOS, you must first go through your bank's internal complaints procedure and receive a final response. If eight weeks pass and you haven't received a final response, or if you're not satisfied with the response you've received, you can then take your complaint to the FOS. They will investigate your case impartially, considering all the evidence from both you and your bank, and make a decision on whether the bank acted fairly and reasonably. Their decisions are binding on the financial business.

Preventing Card Fraud: Your Best Defence

While you can't eliminate the risk of card fraud entirely, proactive measures can significantly reduce your vulnerability. Vigilance and good security practices are your strongest allies:

Guard Your Details

Never share your PIN with anyone, not even bank staff or police. Be wary of unsolicited calls, emails, or texts asking for your card details, passwords, or personal information. Your bank will never ask for your full PIN or online banking password.

Secure Online Transactions

Only make purchases on secure websites (look for 'https://' in the web address and a padlock symbol). Use strong, unique passwords for all your online accounts, especially for banking and shopping sites. Consider using multi-factor authentication (MFA) where available, which adds an extra layer of security, often requiring a code from your phone in addition to your password.

Monitor Your Accounts Regularly

Check your bank and credit card statements frequently, ideally daily or every few days, for any suspicious activity. Many banks offer mobile apps with instant transaction notifications, which can alert you to unauthorised spending almost immediately.

Be Wary of Public Wi-Fi

Avoid making online purchases or accessing sensitive accounts when connected to unsecured public Wi-Fi networks, as these can be vulnerable to interception by fraudsters.

Shred Sensitive Documents

Before discarding bank statements, credit card offers, or any documents containing personal or financial information, shred them to prevent identity theft.

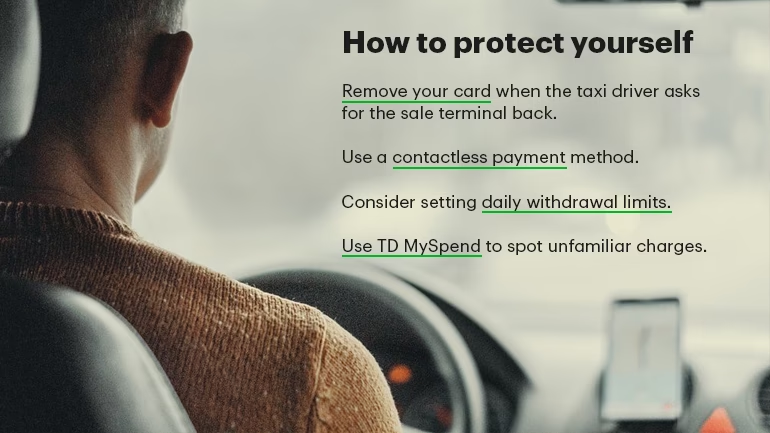

Protect Your Physical Card

Never let your card out of your sight when making a payment. Be cautious at ATMs and card readers, checking for any suspicious attachments (skimmers). Cover the keypad when entering your PIN.

Reporting Fraud or Corruption Against TfL

While the primary focus of this guide is personal card fraud, it's important to note that fraud can also impact public services. Transport for London (TfL) takes a zero-tolerance approach to fraud and corruption that affects its operations and public funds. If you know about or suspect fraud or corruption against TfL, it's crucial to report it in confidence so they can investigate.

You should use the dedicated reporting channels on the TfL website for suspicions related to:

- Fraud within their supply chain: This could include overcharging by suppliers, rigged tenders, undisclosed gifts, or conflicts of interest.

- Payment fraud: Such as payment diversion or cheque fraud impacting TfL.

- Revenue fraud: Examples include counterfeit ticketing, abuse of travel discounts or concessionary schemes, false claims for refunds, or fraudulent avoidance of penalty charge notices.

- Employee benefits fraud: Fraudulent pension claims, inappropriate overtime payments, undisclosed secondary employment, or abuse of employee or nominee travel passes.

- Theft or misuse of assets: Theft of spares or scrap, theft or sale of TfL property, or misuse of company vehicles.

- Unauthorised access to TfL systems and confidential information.

When reporting, include as much detail as possible to assist their counter-fraud specialists. While you can report anonymously, providing contact details allows them to seek clarification and, where appropriate, provide updates. It's vital to remember that this specific channel is *only* for fraud and corruption *against TfL*. For personal issues like unrecognised Oyster Card transactions, penalty fare notices, Congestion Charges, or ULEZ queries, you must contact the appropriate TfL help and contacts team directly.

Immediate Actions: Stolen Card vs. Compromised Details

| Scenario | Key Characteristics | Immediate Action |

|---|---|---|

| Card Stolen/Lost | Physical card is no longer in your possession. Risk of physical use and online transactions. | Contact your bank immediately to block/cancel the card. Report to police (if stolen) and get a crime reference number. Review all accounts for suspicious activity. |

| Card Details Compromised | Physical card is still with you, but its numbers/details have been stolen (e.g., via phishing, data breach, skimming). Risk of online/phone transactions. | Contact your bank immediately to block/cancel the card. Review all account statements carefully. Report to Action Fraud (UK). Change relevant online passwords. |

Frequently Asked Questions (FAQs)

Q: How quickly do I need to report card fraud?

A: You should report card fraud to your bank or card provider immediately upon discovery. The sooner you act, the better your chances of preventing further losses and recovering funds. Delays can sometimes impact your ability to be fully reimbursed.

Q: Will I get my money back if I'm a victim of card fraud?

A: In most cases of unauthorised card fraud, yes, you will get your money back, provided you were not negligent or fraudulent yourself, and you reported it promptly. The Payment Services Regulations (for debit cards) and the Consumer Credit Act (for credit cards) offer strong protections for consumers in the UK. For Authorised Push Payment (APP) fraud, reimbursement depends on the bank's adherence to voluntary codes and the specifics of your case.

Q: What is Action Fraud?

A: Action Fraud is the UK's national reporting centre for fraud and cyber crime. It collects information about fraud from victims across the country and passes it on to the National Fraud Intelligence Bureau (NFIB) to identify patterns, link cases, and inform law enforcement action. Reporting to Action Fraud is crucial for fighting fraud on a national level.

Q: My bank refused a refund. What can I do next?

A: If your bank refuses a refund and you believe their decision is unfair, first make a formal complaint through their internal complaints procedure. If you remain dissatisfied after receiving their final response, or if eight weeks have passed, you can then escalate your complaint to the Financial Ombudsman Service (FOS) for an independent review.

Q: Can I prevent card fraud entirely?

A: While no method is 100% foolproof, adopting strong security habits significantly reduces your risk. This includes being vigilant about phishing attempts, using strong and unique passwords, monitoring your accounts, and protecting your physical card details. Continuous awareness is your best defence.

Being a victim of card fraud is undoubtedly a stressful experience, but by understanding the nature of the threat and knowing the correct steps to take, you can navigate the situation effectively. Remember the importance of acting immediately, meticulously documenting every detail, and knowing your rights as a consumer. By remaining vigilant and informed, you empower yourself against the ever-evolving tactics of fraudsters and help maintain the security of your finances. Stay alert, stay safe, and don't hesitate to use the resources available to you in the event of fraud.

If you want to read more articles similar to Card Fraud: Your Essential UK Guide to Action, you can visit the Taxis category.