10/12/2016

For self-employed taxi drivers across the United Kingdom, understanding and accurately claiming business expenses is not just good practice; it's a fundamental part of managing your finances and ensuring you pay the correct amount of tax. Among the myriad of expenses you might incur, mileage is often one of the most significant, given the very nature of your profession. This comprehensive guide will navigate the intricacies of claiming mileage expenses, from understanding HMRC's rules to meticulous record-keeping, ensuring you’re well-equipped to manage your financial obligations efficiently.

As a taxi driver, your vehicle is your primary tool, and the miles you cover directly translate into your income. However, these miles also incur substantial costs, including fuel, maintenance, and wear and tear. Accurately tracking and claiming these costs is crucial for reducing your taxable profit, thereby lowering your tax bill. Failing to claim legitimate expenses means you could be paying more tax than necessary, directly impacting your take-home pay. So, let’s delve into how you, as a dedicated taxi professional, can effectively claim your mileage expenses.

- Understanding HMRC's Approach to Vehicle Expenses for the Self-Employed

- The Paramount Importance of Record Keeping

- Calculating Business vs. Private Use

- Capital Allowances: Claiming Your Vehicle's Value

- Other Allowable Expenses for Taxi Drivers

- Submitting Your Claim: Self-Assessment Tax Return

- Common Pitfalls to Avoid

- Comparison Table: Actual Costs vs. Simplified Expenses (for Self-Employed Taxi Drivers)

- Frequently Asked Questions (FAQs)

- Q1: Can I claim for my commute to my first fare or from my last fare home?

- Q2: What if I use my personal car for taxi work sometimes?

- Q3: Do I need to keep every single receipt, even for small fuel purchases?

- Q4: How long do I need to keep my tax records?

- Q5: What is the difference between Approved Mileage Allowance Payments (AMAPs) and claiming actual costs?

- Q6: Can I claim for vehicle depreciation?

- Q7: What if I bought my taxi on finance? Can I claim the finance payments?

Understanding HMRC's Approach to Vehicle Expenses for the Self-Employed

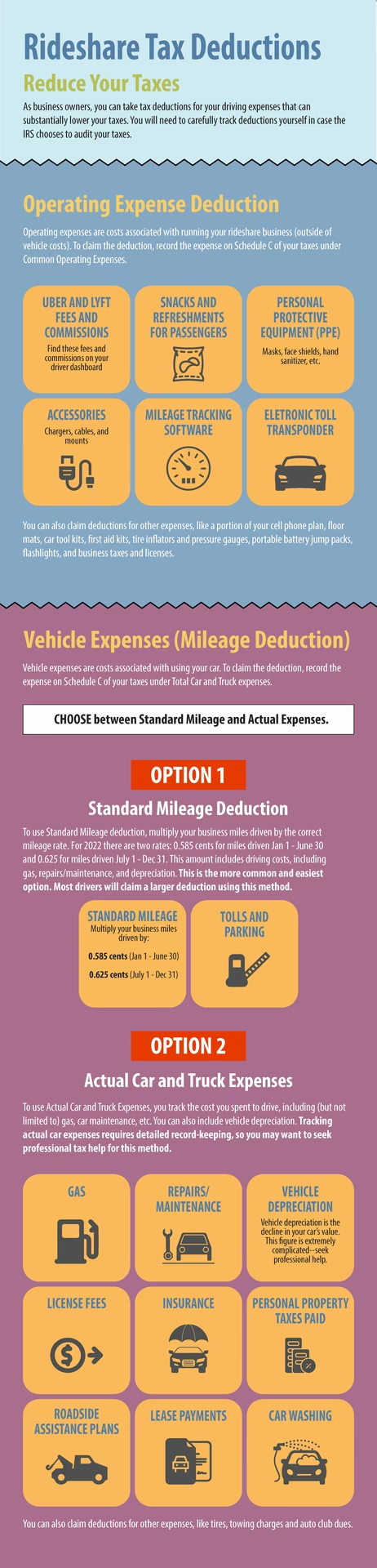

When it comes to vehicle expenses, HMRC distinguishes between different types of claimants and methods. For most self-employed taxi drivers, you will typically be claiming the actual costs of running your vehicle for business purposes, rather than relying on Approved Mileage Allowance Payments (AMAPs). AMAPs are primarily for employees using their own cars for work, where the employer reimburses them at a set rate per mile. As a self-employed individual, you deduct your business expenses directly from your income to calculate your taxable profit.

Actual Costs: The Preferred Method for Taxi Drivers

Claiming actual costs means you account for all the money you spend on your vehicle that is directly attributable to your taxi business. This is generally the most beneficial method for taxi drivers due to the high mileage and associated running costs. Here's a breakdown of what you can typically claim:

- Fuel: This will likely be your largest expense. Keep every receipt, no matter how small.

- Insurance: Only the portion of your insurance policy that covers business use for taxi driving. You cannot claim personal use.

- Repairs and Maintenance: Costs for servicing, fixing breakdowns, replacing parts, and general upkeep to keep your vehicle roadworthy.

- Road Tax (Vehicle Excise Duty): The annual cost of taxing your vehicle.

- MOTs: The cost of your annual Ministry of Transport test.

- Breakdown Cover: Premiums paid for breakdown assistance services.

- Cleaning: Costs associated with keeping your taxi clean and presentable for customers.

- Tyres: The cost of purchasing and fitting new tyres.

- Interest on Vehicle Loans: If you purchased your vehicle using a loan, you can claim the interest portion of the repayments.

- Depreciation (Capital Allowances): This is a crucial aspect for vehicle owners. Instead of claiming the full cost of the vehicle in one go (unless it qualifies for specific allowances like the Annual Investment Allowance), you claim a percentage of its value each year as a 'capital allowance'. This accounts for the vehicle's wear and tear over time.

Simplified Expenses for Vehicles: An Alternative (Often Less Suitable)

HMRC offers a 'simplified expenses' option for vehicles, which involves claiming a flat rate per mile for business journeys, instead of calculating and claiming all the actual costs (including capital allowances). The rates are currently 45p per mile for the first 10,000 miles and 25p per mile thereafter for cars and vans. While simpler, this method is often less advantageous for taxi drivers for several reasons:

- High Actual Costs: Taxi drivers typically incur significantly higher actual costs (fuel, maintenance, insurance, and depreciation) than the simplified mileage rates cover.

- No Capital Allowances: If you use simplified expenses for a vehicle, you cannot claim capital allowances for its purchase. Given the high value of a taxi, capital allowances can provide substantial relief.

- Flexibility: The actual costs method allows you to claim for precisely what you've spent, which for a high-usage vehicle like a taxi, usually results in a larger deduction.

For these reasons, most self-employed taxi drivers find it more beneficial to claim actual costs, meticulously tracking every expense and claiming capital allowances for their vehicle. It requires more diligent record-keeping but often leads to greater tax savings.

The Paramount Importance of Record Keeping

Accurate and comprehensive record keeping is the bedrock of a successful expense claim. Without proper records, HMRC can disallow your claims, leading to unexpected tax bills, penalties, and interest. Here’s what you need to keep:

- Mileage Logbook: This is non-negotiable. You need to record every business journey. For each trip, note the date, starting mileage, ending mileage, total business miles, and the purpose of the journey (e.g., 'taxi fare from A to B'). Many apps are available now for digital logging, or a simple notebook will suffice. Separate your business miles from any personal miles.

- All Receipts: Keep every single receipt for fuel, repairs, servicing, insurance payments, MOTs, breakdown cover, cleaning products, etc. Digital copies are acceptable, but ensure they are legible and securely stored.

- Bank Statements: These can help corroborate your expenses, especially for larger payments like insurance premiums or vehicle purchases.

- Invoices: For any services or goods purchased for your vehicle.

HMRC requires you to keep your records for at least five years after the 31 January submission deadline of the relevant tax year. For example, for the tax year 2023-2024 (ending 5 April 2024), you must keep records until at least 31 January 2030.

Calculating Business vs. Private Use

This is a critical distinction. You can only claim expenses for the portion of your vehicle's use that is *wholly and exclusively* for your taxi business. If you also use your taxi for personal journeys, you must apportion your costs. For example, if 80% of your total mileage in a year is for business and 20% is for private use, you can only claim 80% of your total vehicle running costs (fuel, insurance, repairs, etc.) and 80% of your capital allowance claim.

Your mileage logbook is essential for this calculation. By consistently tracking both business and private miles, you can accurately determine the business-use percentage.

Example of Apportionment:

Let's say in a tax year, your total vehicle mileage is 50,000 miles. Your mileage logbook shows 40,000 of these miles were for business purposes, and 10,000 were private. Your business use percentage is (40,000 / 50,000) * 100 = 80%.

If your total fuel costs for the year were £6,000, you could claim £6,000 * 0.80 = £4,800 as a business expense.

This same principle applies to all other running costs and capital allowances.

Capital Allowances: Claiming Your Vehicle's Value

When you purchase a vehicle for your taxi business, you can't typically claim the full cost as an expense in the year you bought it. Instead, you claim 'capital allowances' over several years, which effectively allows you to deduct a portion of the vehicle's value from your profits each year.

The type and amount of capital allowance you can claim depend on factors such as the vehicle's CO2 emissions and whether it's new or second-hand. Most taxis will fall under the 'main rate' pool (18% writing down allowance per year) or the 'special rate' pool (6% writing down allowance per year for cars with higher CO2 emissions).

The Annual Investment Allowance (AIA) allows businesses to deduct the full cost of qualifying plant and machinery (including many commercial vehicles and some cars) up to a certain limit in the year of purchase. If your taxi qualifies for AIA, you could claim 100% of its cost (or the business-use portion) in the first year, which can be a significant tax saving. However, cars generally do not qualify for AIA, unless they are specifically 'commercial vehicles' like certain vans or lorries. A standard taxi often falls under the rules for cars for capital allowance purposes.

It's always advisable to consult with an accountant to ensure you claim the correct capital allowances for your specific vehicle and circumstances.

Other Allowable Expenses for Taxi Drivers

While vehicle-related expenses are significant, remember to claim other legitimate business expenses that reduce your taxable profit. These might include:

- Licensing Fees: Your taxi driver's license, vehicle license, operator's license.

- Public Liability Insurance: Any insurance beyond vehicle insurance required for your business.

- Accountancy Fees: The cost of hiring an accountant to manage your tax affairs.

- Communication Costs: A portion of your mobile phone bill if used for business calls/apps.

- Uniforms: If you have a specific uniform for your taxi work.

- Training: Costs for any mandatory or beneficial training related to your taxi driving (e.g., advanced driving courses if required for insurance or licensing).

- Stationery and Office Supplies: For your record-keeping.

- Bank Charges: For a dedicated business bank account.

Submitting Your Claim: Self-Assessment Tax Return

All these expenses are declared on your annual Self-Assessment tax return. You will complete the 'SA103S' (short) or 'SA103F' (full) supplementary pages for 'self-employment' as part of your main SA100 tax return. There are specific boxes for vehicle running costs and capital allowances. Ensure all figures are accurate and supported by your meticulous records.

Common Pitfalls to Avoid

To prevent issues with HMRC, be mindful of these common mistakes:

- Poor Record Keeping: This is the number one reason for disallowed claims. Be diligent!

- Claiming Private Use: Do not claim expenses for personal journeys. Apportion accurately.

- Missing Receipts: No receipt, no claim. Make it a habit to collect them all.

- Not Understanding Rules: Stay updated with HMRC guidance or seek professional advice.

- Claiming AMAPs as Self-Employed: Remember, as a self-employed taxi driver, you claim actual costs or simplified expenses, not AMAPs.

Comparison Table: Actual Costs vs. Simplified Expenses (for Self-Employed Taxi Drivers)

| Feature | Actual Costs Method | Simplified Expenses Method |

|---|---|---|

| Expenses Claimed | All actual running costs (fuel, insurance, repairs, etc.) + Capital Allowances for vehicle purchase | Flat rate per business mile (45p/mile up to 10k, then 25p/mile) |

| Record Keeping | Extensive: Detailed mileage logbook, all receipts for costs, invoices | Simpler: Detailed mileage logbook only |

| Complexity | More complex calculations, especially for capital allowances and apportionment | Simpler calculation |

| Tax Benefit for Taxi Drivers | Generally more beneficial due to high running costs and vehicle value | Often less beneficial as it may not cover true costs and no capital allowances |

| Capital Allowances | Can claim for vehicle depreciation | Cannot claim for vehicle depreciation |

Frequently Asked Questions (FAQs)

Q1: Can I claim for my commute to my first fare or from my last fare home?

Generally, no. HMRC views ordinary commuting as a non-deductible personal expense. The 'journey' for business purposes typically starts from when you begin looking for or pick up your first fare, and ends when you drop off your last fare. Travel between your home and your usual place of business (e.g., a taxi rank you regularly operate from) is usually considered commuting.

Q2: What if I use my personal car for taxi work sometimes?

If you genuinely use a personal vehicle for self-employed taxi work, you can still claim the business-use portion of its running costs and capital allowances, following the same principles of apportionment. However, ensure your insurance covers 'business use' or 'hire and reward' as appropriate, as personal insurance policies will not cover taxi work.

Q3: Do I need to keep every single receipt, even for small fuel purchases?

Yes, absolutely. Every receipt contributes to your overall expense claim. HMRC can ask for proof for any expense claimed. It’s better to have too many receipts than not enough.

Q4: How long do I need to keep my tax records?

You must keep your records for at least five years after the 31 January submission deadline of the relevant tax year. For example, for the tax year ending 5 April 2024, you need to keep records until 31 January 2030.

Q5: What is the difference between Approved Mileage Allowance Payments (AMAPs) and claiming actual costs?

AMAPs are specific rates (e.g., 45p per mile) that employers can pay employees for using their own vehicle for work without tax implications for the employee. They are not generally applicable to self-employed individuals claiming expenses. As a self-employed taxi driver, you will typically claim the actual costs incurred for your business mileage, or in some cases, use the simplified expenses flat rate per mile (which is different from AMAPs and often less beneficial for taxi drivers).

Q6: Can I claim for vehicle depreciation?

Yes, but not directly as an 'expense' like fuel. Instead, you claim 'capital allowances'. This is a tax relief that allows you to deduct a portion of the cost of your vehicle (or other assets) from your profits over time, reflecting its depreciation in value due to business use. The specific allowance depends on the vehicle's type and CO2 emissions.

Q7: What if I bought my taxi on finance? Can I claim the finance payments?

You can usually claim the interest portion of your finance payments as a business expense. The capital repayment part of the loan is not an expense, but the vehicle itself would be eligible for capital allowances.

By diligently applying these principles, maintaining impeccable records, and understanding the nuances of HMRC's rules, UK taxi drivers can effectively manage their mileage expenses. This not only ensures compliance but also optimises your tax position, allowing you to focus on what you do best: providing excellent service to your passengers.

If you want to read more articles similar to UK Taxi Drivers: Mastering Mileage Expenses, you can visit the Taxis category.