23/03/2026

For independent taxi drivers, navigating the landscape of Goods and Services Tax (GST) is a crucial aspect of financial management. The fares paid by passengers typically include GST, making it imperative for self-employed operators to understand their obligations. This comprehensive guide aims to demystify the process, from initial registration to detailed reporting, ensuring you remain compliant and can efficiently manage your business finances.

- Essential GST Registration and Obligations

- Understanding and Completing Your Business Activity Statement (BAS)

- Specific GST Considerations for Taxi Services

- GST on Ride-Sourcing Services (Ola, Uber, etc.)

- GST for Tour Operators and Agents

- Input Tax Credit on Car Purchases and Leases

- Selling Taxi Licences and Plates

- Crucial Record-Keeping Requirements

- Frequently Asked Questions (FAQs)

Essential GST Registration and Obligations

If you operate as a taxi driver and are not formally employed by another entity, you bear direct responsibility for your GST affairs. Unlike some other business types, taxi drivers are generally required to register for GST regardless of their annual earnings. This mandatory registration ensures that the tax collected on fares is accounted for correctly. Once registered, your primary responsibilities include accurately reporting your business income and expenses, specifically focusing on the GST component.

A key aspect of your obligations involves claiming GST credits. These credits relate exclusively to the GST included in your business purchases. For instance, if you pay GST on fuel, vehicle maintenance, or other operational costs, you can typically claim this back as a credit, reducing your overall GST liability. However, it's crucial that these expenses are directly related to your taxi work.

Lodging Business Activity Statements (BAS) is another non-negotiable requirement. For independent taxi drivers, these statements must be lodged either monthly or quarterly. It's important to note that the option to lodge annually is not available for this industry. Ultimately, your goal is to pay your net GST, which is the difference between the GST collected on all your fares and the input tax credits claimed on your eligible business purchases, including any bailment payments.

The Cents Per Kilometre Earnings Rate

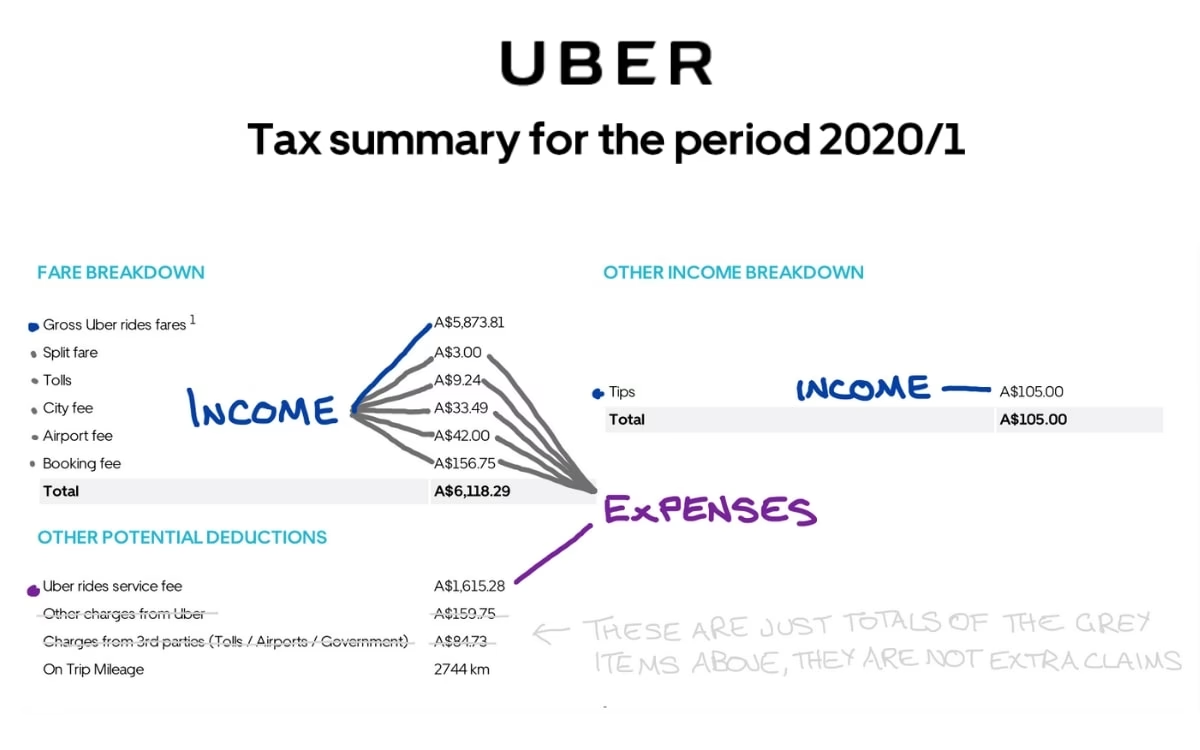

Maintaining meticulous records is fundamental to accurate tax reporting. However, in instances where proper records of your earnings are unavailable, you may be required to utilise the cents per kilometre earnings rate when preparing your BAS. This rate represents the average income earned by a taxi per total kilometre travelled in a year. It's a gross measure, meaning it includes GST and does not factor in expenses.

This rate, currently set at £1.30/km, serves multiple purposes. Taxi operators and drivers can use it to benchmark their performance against industry averages and to verify the accuracy of their existing tax records. Tax agents and accountants also leverage this rate to assist clients in preparing tax returns and BAS, particularly in cases where detailed records are lacking. The rate itself has been developed through consultation with various participants within the taxi industry, aiming for a fair and representative figure.

Understanding and Completing Your Business Activity Statement (BAS)

The Business Activity Statement (BAS) is the primary document you'll use to report and pay the GST you've collected from your fares and to claim any eligible GST credits. Since 1 July 2017, Simpler BAS has become the default reporting method for many small businesses, and taxi drivers have specific options available to them.

GST Reporting Methods for Taxi Drivers

Taxi drivers must choose one of the following methods for GST reporting:

- Simpler BAS: This streamlined method allows you to report only three key labels in your BAS: G1 (Total sales), 1A (GST on sales), and 1B (GST on purchases). You pay your actual amounts on a quarterly basis.

- Pay a Pre-determined GST Instalment Amount: Under this option, you pay a pre-determined GST instalment amount quarterly and report your actual GST information annually. To qualify, you must have reported actual GST amounts for at least four months (e.g., two quarterly BAS submissions) and must not be in a net refund position.

- Full Reporting: This method requires you to calculate and report all the GST labels in your BAS and pay your actual GST amounts quarterly.

As previously mentioned, reporting annually is generally not available for taxi drivers, irrespective of their chosen method. You can contact the relevant tax authorities to change your GST reporting method if your business needs evolve.

Reporting Sales and Purchases on Your BAS

When completing your BAS, you must include all income and expenses from your taxi driving business. Here’s a breakdown of what to report:

- G1 Total Sales: This label requires you to report all your income. This includes your total taxi takings from all sources (cash, credit cards, Cabcharge, etc.), any tolls collected, and extras such as baggage handling. Additionally, any tips received and WorkCover payments must be included in this total.

- 1B GST on Purchases: Here, you'll report the total GST included in all your business purchases.

If you opt for the Full Reporting method, you'll also need to consider G11 Non-capital purchases. This includes a broader range of expenses such as the bailment payment or shift rent paid to a taxi operator, fuel, oil, car washes, insurance payments, uniforms (if tax deductible), business telephone expenses, and accounting fees. Payments where no GST was included in the price, such as bank fees and licence fees, are also reported here.

The figure at label 9, 'Your payment or refund amount', indicates your net GST position. A positive figure means an amount payable, while a negative figure signifies a refund.

Specific GST Considerations for Taxi Services

While cab services are generally taxable, certain exemptions apply, particularly to metered taxis and auto rickshaws, including those operating through aggregators like Ola Auto. Understanding these nuances is vital for correct compliance.

GST Rate Options for Service Providers

As a service provider, you typically have two options regarding the GST rate you apply:

- Option 1: Pay GST at a rate of 5%. Under this option, you are permitted to claim input tax credits only for GST paid on cab services acquired from other persons. Any other GST paid on general business expenses (e.g., telephone bills) cannot be claimed as input tax credit and will effectively lapse. This option is primarily for those whose core inputs are also cab services.

- Option 2: Pay GST at the rate of 12%. This option allows you to claim input tax credits for GST paid on all eligible input goods and services, subject to general restrictions on the use of input tax credit. This provides broader scope for claiming back GST on various business expenditures.

In scenarios where a customer is charged based on fuel consumption plus separate service charges, GST is typically applied at a rate of 18% solely on the service charges, with no GST applicable to the fuel component itself.

Reverse Charge Mechanism (RCM) for Service Receivers

An important rule, applicable from 1st October 2019, concerns the Reverse Charge Mechanism (RCM). If you are an individual taxi driver not operating as a body corporate and have opted to pay GST at the 5% rate, you are not required to charge GST when providing services to a corporate entity. Instead, the corporate entity (the service receiver) is obliged to pay the GST on a reverse charge basis. In such cases, your invoice should clearly state that "GST payable on Reverse charge basis," and you would simply charge the amount for your services without adding GST.

Place of Supply for Rent-a-Cab Services

Determining the 'place of supply' is crucial for correctly applying GST, especially when services cross state or territorial boundaries. For services provided to a GST-registered person, the place of supply is generally the location of the recipient. For example, if a Delhi-registered cab provider offers a service to a Rajasthan-registered person in Gujarat, Rajasthan would be the place of supply.

However, if car rental services are provided to an unregistered person, the place of supply is the location where the passenger embarks on the conveyance for a continuous journey. If the right to passage is for future use and the starting point is unknown, the place of supply defaults to the recipient's location if an address is on record. If not, it becomes the service provider's location. The following table illustrates these scenarios:

| Location of Cab Service Provider | Registration Status of Service Recipient | Location of Cab Service Receiver | Location Where Journey Starts | Place of Supply for the Agent | GST to be Charged by the Service Provider |

|---|---|---|---|---|---|

| Gujarat | Registered | Gujarat | Rajasthan | Gujarat | CGST + SGST |

| Gujarat | Registered | Rajasthan | Gujarat | Rajasthan | IGST |

| Gujarat | Unregistered | Rajasthan | Rajasthan | Rajasthan | IGST |

| Gujarat | Unregistered | Not known | Rajasthan | Rajasthan | IGST |

| Gujarat | Unregistered | USA | Rajasthan | Rajasthan | IGST |

GST on Ride-Sourcing Services (Ola, Uber, etc.)

For taxi drivers operating through ride-sourcing platforms like Ola or Uber, the GST obligations differ significantly. These services are typically covered under Section 9(5) of the CGST Act, which mandates that the e-commerce operator (e.g., Ola, Uber) is responsible for collecting and paying GST to the government, rather than the individual cab driver.

This means that as a driver providing services through these aggregators, you are generally not required to collect and pay GST yourself. Furthermore, you are not typically required to register for GST, even if your turnover exceeds specified limits. For example, a driver operating five cars via Uber with a turnover of £25,000 would still not be required to register for GST. Even if a driver is already GST-registered for other activities, they are not required to collect GST for services provided via Ola or Uber.

Input Tax Credits (ITC) for Service Receivers

Under Section 17(5) of the CGST Act, GST paid on 'rent a cab' services is generally disallowed as an input tax credit for the service receiver. However, a crucial exception exists: if the service receiver is also a cab services provider, they can claim input credit for such GST. This distinction is vital for businesses within the same industry.

Corporate Services by Aggregators

When aggregators like Ola and Uber provide cab services to corporate entities, the transaction structure involves a few steps. Aggregators source services from cab drivers and then provide them to corporates. The aggregator pays fees to the cab drivers and then seeks reimbursement from the corporate via a debit note. For instance, if Ola uses M/s. Akash Cars to provide a service to Reliance Industries:

- Ola to M/s. Akash Cars: Ola pays the driver (e.g., £1,000 trip charges + £50 GST @ 5% = £1,050 total) and pays the GST to the government.

- Debit Note by Ola to Reliance: Ola issues a debit note to Reliance for the trip charges (£1,000 trip charges + £50 GST @ 5% = £1,050 total). Reliance gets reimbursement but cannot claim ITC on this GST.

- Commission Invoice by Ola to Reliance: Ola also charges a commission for its technology aggregation services (e.g., £200 commission + £36 GST @ 18% = £236 total). Reliance can claim ITC on the GST charged for this commission.

This complex structure highlights how GST is handled when aggregators facilitate corporate bookings.

GST for Tour Operators and Agents

Tour operators often provide bundled packages that include various services like hotels, cabs, and entertainment tickets. How GST is applied depends on how these packages are structured:

- Flat Fee Package: If a tour operator sells a package for a single flat fee (e.g., £20,000 for hotel, cab, etc.), the GST rate applicable to the tour package as a whole is applied to the total charges.

- Separately Charged Services: If the tour operator itemises and charges separately for each service (e.g., £10,000 for hotel, £5,000 for cab, £3,000 for entertainment tickets), then the specific GST rate applicable to each individual service is charged on its respective amount.

- Pure Agent for Some Services: A tour operator can act as a 'pure agent' for certain services. In this scenario, for services where the operator is merely facilitating a payment on behalf of the client (e.g., arranging a cab for £8,000 at the client's request), the operator does not charge GST on that amount and is not entitled to input tax credit for it. To qualify as a pure agent, specific conditions must be met: the payment must be separately indicated in the invoice, the procured supplies must be in addition to the operator's own services, the operator must not use the goods/services for their own interest, and they must only recover the actual amount incurred.

- Commission Basis: Some tour operators book all services on behalf of passengers and charge a commission for this facilitation. In this case, GST is leviable at a rate of 18% solely on the commission charged. Tour operators generally can claim input tax credit for GST paid on cab services, except when acting as a pure agent.

Input Tax Credit on Car Purchases and Leases

For cab owners, claiming input tax credit on the purchase of a car is specifically prohibited under Section 17(5) of the CGST Act, unless the purchased car is used for the taxable supply of transportation of passengers. If your car is used for this purpose, ITC is generally available in the month of purchase. However, it's important to remember that if you've opted for the 5% GST rate, you cannot claim such input credit. Only those who have chosen the 12% GST rate can do so.

For drivers operating through aggregators like Ola or Uber, where the driver is not required to pay GST themselves (as the aggregator handles it), taking ITC on a car purchase is typically not possible.

Many cab aggregators also offer car leasing services to their drivers. When an aggregator purchases a car and leases it to a driver for passenger transportation via their app, this leasing program is subject to GST. The driver pays minimum initial deposits and daily/monthly rent to the aggregator, with GST applicable on these lease amounts. The aggregator, in turn, can claim the ITC on the GST paid when they purchased the car, as it is used for providing passenger transportation services.

Selling Taxi Licences and Plates

The sale of a business, which can include taxi plates and licences, may be GST-free if the transaction constitutes the sale of a 'going concern'. A sale qualifies as a going concern if:

- The sale is for consideration.

- The purchaser is registered, or required to be registered, for GST.

- Both parties agree in writing that the sale is of a going concern.

- All necessary components for the continued operation of the business are supplied to the buyer.

- The supplier continues to operate the business until the day of sale.

For example, if an owner/driver sells their taxi business, including the licence, motor vehicle, and meter – all components necessary for continued operation – and continues to operate until the buyer takes over, this would be a sale of a going concern. However, selling just the licence, the vehicle, or the meter individually would not qualify, as all necessary items for continued business operation would not have been supplied.

Similarly, if you own a taxi licence that you lease out and then sell it to a third party with the original lessee still in place, this could also be a sale of a going concern because the activity of leasing out a taxi plate constitutes an enterprise, and all necessary elements for its continued operation are supplied. Conversely, selling a taxi licence to its lessee, or to a third party without an active lease, would not typically qualify as a sale of a going concern.

Crucial Record-Keeping Requirements

Maintaining accurate and thorough records is paramount for any independent taxi operator. You must keep proper records of all business transactions, which should include:

- Total kilometres travelled (both with and without passengers).

- Number of shifts worked.

- Total income received, detailing sources such as cash, credit card payments, and Cabcharge.

- All business expenses, including specifics like petrol and car washes.

Your records should be supported by appropriate documentation, such as invoices and receipts, to verify both your income and expenses. These vital records must be retained for a minimum of five years from the date they were prepared, obtained, or the transaction was completed, whichever is later. Proper record-keeping not only ensures compliance but also simplifies your BAS preparation and can be invaluable in case of an audit.

Frequently Asked Questions (FAQs)

- Do I need to register for GST if I'm a part-time taxi driver?

- Yes, if you're an independent taxi driver and not employed by someone else, you must register for GST regardless of how much you earn. There is no minimum turnover threshold for mandatory registration in this industry.

- What is 'net GST'?

- Net GST is the total GST included in all the fares you've taken, minus any input tax credits for the GST included in your business purchases, such as fuel, maintenance, and bailment payments.

- Can I choose to lodge my Business Activity Statement (BAS) annually?

- No, independent taxi drivers are generally required to lodge their BAS either monthly or quarterly. The option for annual lodging is not available for this industry.

- What happens if I don't keep proper records?

- If you do not have proper records of your earnings, you may be required to use the cents per kilometre earnings rate when preparing your BAS to estimate your income for GST purposes.

- Are ride-sourcing services like Uber or Ola covered by these GST rules?

- For ride-sourcing services, the e-commerce operator (e.g., Ola, Uber) is generally responsible for collecting and paying the GST. This means that individual drivers for these platforms are typically not required to collect or pay GST themselves, nor are they usually required to register for GST for these services.

- Can I claim GST credits on the purchase of my taxi vehicle?

- Input tax credit on car purchases is generally allowed if the car is used for the taxable supply of passenger transportation. However, if you've opted for the 5% GST rate, you cannot claim this credit. It's only available if you've chosen the 12% GST rate. For drivers operating through aggregators, claiming ITC on a purchased car is usually not possible as the aggregator handles the GST.

- Is the sale of a taxi licence always GST-free?

- The sale of a taxi licence or plate can be GST-free if it is part of a 'sale of a going concern', meaning all things necessary for the continued operation of the business are supplied to the buyer, and certain other conditions are met. If sold in isolation without the full business, it may not be GST-free.

If you want to read more articles similar to Understanding GST for Independent Taxi Operators, you can visit the Taxis category.