28/09/2025

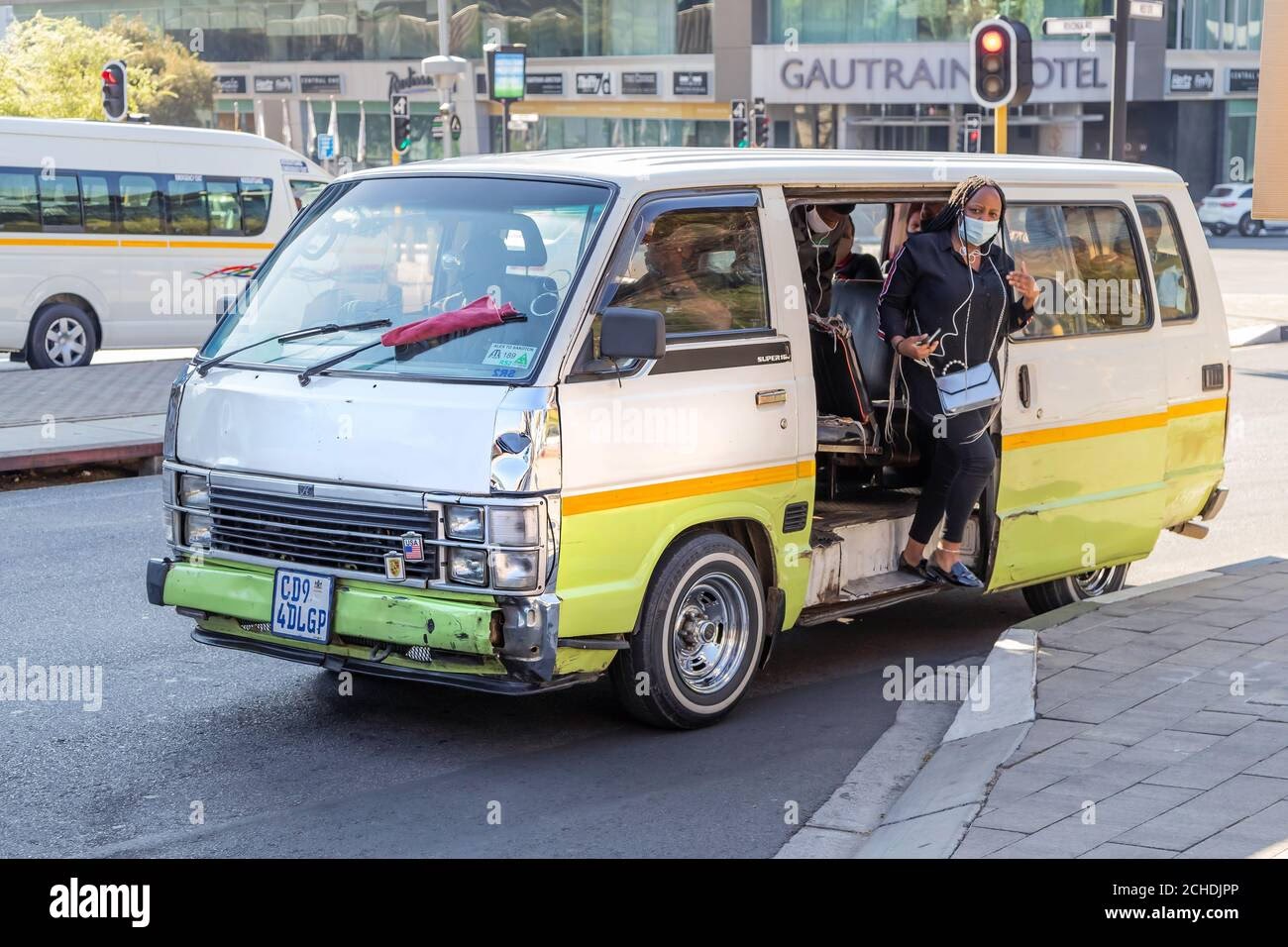

South Africa's urban and rural landscapes are undeniably shaped by one ubiquitous mode of transport: the taxi. For millions of commuters, these vehicles are not merely a convenience but the very backbone of their daily lives, facilitating journeys to work, school, and essential services. Yet, the exact scale and intricate workings of this colossal industry often remain shrouded in mystery, with conflicting figures and deep-seated misconceptions clouding the true picture. So, how many taxis truly operate across the vast expanse of South Africa, and what lies beneath the surface of this indispensable sector?

- The Indispensable Backbone of South African Transport

- Defining a Taxi in South Africa: A Nuanced Perspective

- The Taxi Industry and the Economy: A Deep Dive into Taxation

- An Uneven Playing Field: Competition and Fairness

- Towards Formalisation: Government's Role and Future Prospects

- Frequently Asked Questions (FAQs)

- Conclusion

The Indispensable Backbone of South African Transport

The taxi industry in South Africa is far more than just a collection of vehicles; it's a dynamic, sprawling ecosystem that underpins the country's public transport system. Each day, an astonishing 3.7 million workers rely on taxis for their commute, undertaking a staggering 10 million trips. This immense daily activity translates into a significant economic force, generating an estimated R90 billion in revenue annually. To put this into perspective, the sector's annual fuel expenditure alone stretches into R36 billion, with additional tens of billions allocated to service, maintenance, finance, and insurance costs.

This makes the taxi industry invaluable to the local economy, accounting for an impressive 80.2% of the country's 4.7 million daily public transport trips, a substantial increase from 67.6% in 2013. Its sheer dominance underscores its critical role, especially given that a large segment of the population lacks access to private vehicles. The industry is organised into over 1,200 associations scattered nationwide, comprising approximately 150,000 individual owners. These associations provide structured services to specific areas, operating under a highly regulated framework that requires government registration, valid operating licences, and regular vehicle inspections.

Defining a Taxi in South Africa: A Nuanced Perspective

Pinpointing an exact number of taxis in South Africa is surprisingly complex, with figures varying significantly depending on the source and the definition of 'taxi'. Initial broad estimates have ranged from as high as 1.7 million to as low as 1.2 million, or even around 1.3 to 1.4 million. However, a more detailed understanding of the formal sector suggests a more specific number of vehicles owned by the approximately 150,000 individual operators who form the core of the organised taxi industry.

The distinction between different types of taxi services further complicates the count. Traditionally, South Africa has been home to both independently operated taxis and government-regulated metered taxis:

- Traditional Taxis: Often privately owned small, four-door cars, these are typically brightly painted and decorated, sometimes bearing a large 'T' on the roof. They are driven by independent operators, are generally more common, and drivers are often well-versed in local routes.

- Metered Taxis: Regulated by the government, these are usually larger, more modern vehicles, and drivers often wear uniforms. Fares are regulated by a meter or offered at a fixed price for a given distance, making them generally more expensive but often perceived as safer and more reliable.

While some estimates suggest around 20,000 traditional taxis and 8,000 metered taxis in operation, these figures are often overshadowed by the sheer volume of the minibus taxi sector, which constitutes the bulk of the industry's operations and accounts for the larger reported numbers of vehicles belonging to associations. The discrepancy highlights the informal nature of parts of the sector versus the formal, regulated elements.

Regional Distribution of Registered Taxis

The number of registered taxis also varies significantly across South Africa's provinces, reflecting population density and urbanisation levels. While these figures might not encompass the broader, sometimes informal, estimates, they provide insight into the formally recognised fleet:

| Province | Approx. Registered Taxis |

|---|---|

| Western Cape | 11,000 |

| Eastern Cape | 7,000 |

| Gauteng | 5,000 |

| KwaZulu-Natal | 6,000 |

Within major metropolitan areas, the concentration is naturally higher. For instance, Cape Town is estimated to have around 7,000 taxis operating within its metropolitan area, significantly more than Johannesburg's roughly 3,000. This provincial and urban variation further illustrates the fragmented nature of the industry's data.

The Taxi Industry and the Economy: A Deep Dive into Taxation

Despite its undeniable economic footprint, the taxi industry's contribution to state coffers through taxes has been disproportionately low, a point of significant contention and a major focus for the South African Revenue Service (SARS). With an estimated annual revenue of R90 billion, the sector has the potential to make a substantial tax contribution, particularly concerning Corporate Income Tax, as taxi associations are registered as businesses.

However, in 2021, the entire sector reportedly paid a mere R5 million in corporate income tax. This figure stands in stark contrast to the potential tax revenue SARS is missing out on annually:

| Tax Type | Estimated Annual Uncollected Revenue |

|---|---|

| Corporate Income Tax (from operators) | R3.6 billion |

| Value-Added Tax (VAT) on fares | R6.75 billion |

| Pay-As-You-Earn (PAYE) Tax | R1.91 billion |

| Total Estimated Tax Loss (including fuel levies & RAF contributions) | R20 billion – R25 billion |

This massive tax gap is roughly equivalent to the amount President Cyril Ramaphosa pledged to support black-owned and small businesses, highlighting the profound economic implications. For context, compare this to other major South African corporations:

| Company (2023) | Revenue (Approx.) | Income Tax Paid to SA Govt. (Approx.) |

|---|---|---|

| Shoprite | R215 billion | R2.46 billion |

| MTN Group (SA share) | N/A | R6.8 billion |

| Uber (platform contribution to SA economy) | R17 billion | (Pays 15% tax on service/booking fees) |

The stark difference raises questions about fairness and regulatory consistency across industries.

Why Taxing the Taxi Industry is So Challenging

SARS has long acknowledged the tax gap, but efforts to improve compliance face formidable obstacles:

- Informal Nature: The industry largely operates on a cash basis, with fares collected in hand and minimal financial documentation. Most operators do not keep formal records of their earnings, making revenue tracking and enforcement exceedingly difficult.

- Political Influence: The industry is highly organised and influential, with powerful groups like SANTACO and the National Taxi Alliance (NTA) often resisting regulatory changes. Strikes and protests have historically been used to push back against stricter licensing, fare regulation, and taxation, as seen with SANTACO-WC's withdrawal from the Minibus Taxi Task Team in 2023 over vehicle impoundment disputes.

- Economic Concerns: Taxi associations argue that increased taxes would inevitably lead to higher fares, disproportionately burdening low-income commuters who rely on their services. They also highlight unequal government subsidies; while bus operators receive financial support, minibus taxis do not, despite carrying the vast majority of public transport passengers.

Expert Perspectives: A Divided View

The debate around taxi industry taxation features diverse viewpoints:

- Andre Bothma (CEO of Irhafu, Tax Educator): Bothma underscores that the cash-based nature of operations makes proper record-keeping rare, leading to very little income tax being collected. He asserts that the main tax contribution from taxi operators comes through fuel levies rather than direct income tax. He also clarifies that membership fees paid to associations function more as internal dues than formal tax contributions.

- Mbali Ntuli (CEO of Ground Work Collective, former politician): Ntuli offers a contrasting perspective, arguing that the industry is more compliant than often assumed, with 89% of operators registered and paying income tax, VAT, and levies. She dismisses the notion that taxi owners hoard cash to evade taxes, stating that South Africa's financial regulations make large-scale evasion nearly impossible as operators need to bank earnings to finance new vehicles. She also highlights bureaucratic delays, where many owners apply for operating licences but are left waiting indefinitely, forced to use application receipts as proof of application. Ntuli criticises impoundments, suggesting taxis are sometimes seized for issues beyond the owner's control, and argues that some provinces, like the Western Cape, escalate directly to impoundment, worsening tensions. She debunks the claim that taxis undermined South Africa's rail system, stating they coexisted for decades and rail's decline has documented, unrelated causes. While acknowledging internal violence within the sector, she notes passengers are considered sacred. She also highlights the industry's long history of supporting black economic empowerment, with businesses passed down through families and associations funding community initiatives like scholarships and housing.

An Uneven Playing Field: Competition and Fairness

The disparity in tax contributions creates an uneven playing field within the transport sector. Ride-hailing companies like Uber and Bolt, direct competitors to traditional taxis, pay 15% tax on service and booking fees. Logistics companies, using vans and buses, adhere to strict tax regulations, and even traditional bus operators like Putco pay VAT and corporate tax. For businesses that follow formal rules, this situation creates significant competitive pressure, as they face rising costs and tax obligations while minibus taxis appear to operate with fewer financial burdens.

However, this perceived benefit often doesn't extend to the drivers. Unlike ride-hailing drivers who receive fare breakdowns and digital records, taxi drivers are typically paid in cash, making income tracking virtually impossible. They also contend with high daily rental fees, fluctuating fuel prices, and often lack formal employment benefits. For many drivers, tax compliance becomes a matter of survival in an industry where they wield little control over their earnings structure. The true beneficiaries, in terms of financial control and potential tax avoidance, are often the taxi associations and fleet owners who manage fares and finances.

Towards Formalisation: Government's Role and Future Prospects

Closing the tax gap in the minibus taxi industry is a monumental task that requires a phased, strategic approach. International examples from Zimbabwe, Ghana, and Nigeria demonstrate the risks of rushed policies in taxing informal sectors, often leading to limited collection due to weak financial records, lack of trust, and strong industry resistance.

For South Africa, a gradual strategy could involve SARS initially implementing a fixed annual tax per taxi before gradually transitioning to a more structured system. Embracing digital fare payments could significantly aid revenue tracking, but given the deep entrenchment of cash transactions, any shift must be slow and undertaken in close collaboration with taxi associations.

Enforcement alone is unlikely to succeed. Unlike bus operators who receive government subsidies, minibus taxis cover all their costs, making taxation feel like an additional burden. Incentives such as fuel tax rebates or vehicle financing support could encourage compliance. Crucially, SARS and the government must engage with industry leaders like SANTACO and the National Taxi Alliance to foster buy-in and avoid widespread resistance or protests. A strategy focusing on targeted audits, improved record-keeping, and incentives for voluntary compliance would likely be more effective than heavy-handed crackdowns. Furthermore, the government should push for greater transparency within taxi associations, holding them accountable for tax compliance rather than allowing them to shield individual operators.

If implemented effectively, such measures could generate much-needed tax revenue while maintaining stability within the vital transport sector. However, without genuine industry cooperation and a respectful, collaborative dialogue that involves the true decision-makers – the taxi owners – the persistent challenges of violence, intimidation, and under-taxation are likely to endure.

Frequently Asked Questions (FAQs)

1. How many taxis are there in South Africa?

The exact number varies by source and definition. While broad estimates range from 1.2 million to 1.7 million, the formal organised industry comprises approximately 150,000 individual owners whose vehicles form the backbone of public transport. Specific provincial figures for registered taxis are lower, indicating the complexity of a precise count due to formal and informal operations.

2. What is the economic impact of South Africa's taxi industry?

The taxi industry is a massive economic force, generating an estimated R90 billion in revenue annually. It accounts for over 80% of daily public transport trips, facilitating 10 million journeys and transporting 3.7 million workers each day. It also contributes significantly to fuel sales and vehicle maintenance costs.

3. Why is it difficult to tax the taxi industry in South Africa?

Taxation is challenging due to the industry's largely informal, cash-based nature, making revenue tracking difficult. Political influence and strong resistance from taxi associations also hinder regulatory changes. Additionally, associations argue that increased taxes would lead to higher fares for low-income commuters, and they highlight unequal government subsidies compared to other public transport modes.

4. Do taxi drivers and owners pay taxes in South Africa?

While the industry's overall tax contribution is disproportionately low compared to its revenue, many individual operators and associations do pay some taxes, particularly through fuel levies and indirect contributions. Taxi owners, to finance new vehicles, often need to demonstrate financial records and tax compliance. However, formal corporate income tax and VAT collections from the sector are significantly below potential.

5. What are the main types of taxis in South Africa?

South Africa has traditional taxis (often privately owned, independent operators), metered taxis (government-regulated, larger vehicles with fixed fares), and the dominant minibus taxis (which form the core of the organised public transport system, serving specific routes and associations).

Conclusion

The South African taxi industry is a colossal, indispensable pillar of the nation's public transport system, moving millions daily and generating billions in revenue. Despite its vital role, it navigates a complex landscape marked by varying operational figures, a predominantly informal cash-based structure, and a contentious relationship with taxation. While the exact number of vehicles remains elusive due to the industry's multifaceted nature, the core of the organised sector involves around 150,000 individual owners.

The significant gap between the industry's vast earnings and its formal tax contributions presents a major challenge for SARS and the government. Bridging this gap requires a nuanced, phased approach that acknowledges the industry's unique characteristics, fosters collaborative dialogue with key stakeholders, and potentially offers incentives alongside targeted enforcement. Ultimately, formalising the sector's tax contributions is not just about revenue generation; it's about ensuring fairness across the transport sector, fostering trust, and recognising the profound socio-economic impact of an industry that truly keeps South Africa moving.

If you want to read more articles similar to South Africa's Taxis: Numbers, Impact, and Tax, you can visit the Transport category.