15/01/2017

For anyone in the United Kingdom contemplating the bustling streets of New York City as a professional driver, whether behind the wheel of a classic yellow cab, a sleek limousine, or operating for popular ride-hailing services like Uber or Lyft, there's a unique and absolutely essential requirement you must understand: TLC insurance. This isn't your standard personal car insurance, nor is it merely a generic commercial policy. It's a highly specific type of coverage mandated for anyone operating a 'for-hire' vehicle within the five boroughs of New York City.

New York City stands out as one of the few places in the United States that demands such specialist coverage for its extensive network of rideshare, private hire, taxi, and limousine drivers. This regulation ensures a robust safety net for drivers, passengers, and pedestrians alike, reflecting the city's commitment to public safety and consumer protection. Navigating this requirement can seem complex, particularly for those accustomed to different insurance landscapes. However, understanding the nuances of TLC insurance is paramount for legal and secure operation in the city that never sleeps. This comprehensive guide will explain everything you need to know about TLC insurance in New York City, how it functions, and why it's indispensable for your driving career there.

- Understanding New York's TLC Insurance Framework

- Why This Specialist Cover Is Absolutely Crucial

- Who Needs This Specialist Cover in NYC?

- What Does TLC Insurance Encompass?

- Navigating the Costs of TLC Insurance in NYC

- Securing Your TLC Policy: A Practical Approach

- Frequently Asked Questions About TLC Insurance

- Is TLC insurance required outside New York City?

- Can I simply use my personal car insurance policy for commercial driving in NYC?

- Does Uber or Lyft provide full insurance coverage for their drivers in NYC?

- What happens if I operate a for-hire vehicle in NYC without TLC insurance?

- Is TLC insurance the same as a standard commercial auto insurance policy?

- Final Word on NYC TLC Insurance

Understanding New York's TLC Insurance Framework

TLC insurance is a bespoke type of motor vehicle coverage specifically designed for vehicles operating on a 'for-hire' basis within New York City. The acronym 'TLC' stands for the Taxi and Limousine Commission, the regulatory body established in 1971. This commission holds the vital responsibility of overseeing and licensing all taxis, limousines, black cars, and other private hire services that operate within the city's jurisdiction. Consequently, the insurance required by this authoritative body has become universally known as TLC insurance.

This particular insurance policy provides extensive protection, encompassing various critical aspects for drivers, their passengers, and any third parties, including pedestrians, who might be affected in the event of an incident. It typically comprises several core components, including robust liability coverage, personal injury protection, and cover for property damage. For any driver licensed by the TLC to legally operate their vehicle, possessing this specific insurance is not merely a recommendation but a strict legal imperative. Without it, you simply cannot pick up fare-paying passengers or operate commercially within New York City.

The rates for TLC insurance are not static; they can fluctuate considerably based on a multitude of factors, much like standard motor insurance. These variables often include the driver's age, their driving record (a clean record is always beneficial), and the specific type of vehicle being insured. To secure the most advantageous coverage at a competitive price, drivers are strongly advised to compare quotes from a variety of insurance providers. Furthermore, maintaining an exemplary driving record and undertaking approved defensive driving courses can significantly contribute to securing more favourable insurance premiums. Insurance companies meticulously assess a driver's history when determining policy costs, meaning safe driving habits and an accident-free record can lead to substantial long-term savings on your TLC insurance.

Why This Specialist Cover Is Absolutely Crucial

The fundamental reason you need TLC insurance when driving for commercial purposes in New York City is straightforward: your standard personal car insurance policy simply will not cover you. As soon as you begin to use your vehicle for commercial activities – whether that's picking up a passenger via Uber or Lyft, driving a taxi, or chauffeuring clients in a limousine – your personal policy effectively ceases to provide coverage. This critical distinction is often misunderstood, leading to potentially devastating financial consequences.

While ride-hailing platforms like Uber and Lyft do offer some basic coverage, this protection is often limited. Typically, their insurance might cover you when you are actively driving to pick up a passenger or when a passenger is in your vehicle. However, there can be significant gaps, particularly during the periods between rides – for instance, when you are logged into the app but awaiting a fare. This is where TLC insurance steps in. It functions much like a comprehensive commercial vehicle insurance policy, ensuring you are continuously covered, even during these 'between rides' periods when other policies might leave you exposed.

Whether you're affiliated with a major ride-hailing app, an established taxi firm, or a luxury limousine company, TLC insurance is non-negotiable for both protection and ultimate peace of mind. It safeguards you against financial ruin by covering damages to other people and their property that might result from your actions behind the wheel. Crucially, it also protects your passengers. Without adequate TLC insurance, you could find yourself personally liable for substantial out-of-pocket expenses for damages, medical costs, or legal fees, especially if you've mistakenly relied solely on a personal vehicle policy. This specialist cover is your shield against the unforeseen, allowing you to focus on providing excellent service to your fares.

Who Needs This Specialist Cover in NYC?

In New York City, the requirement for TLC insurance extends to virtually every individual who provides professional driving services for remuneration. If you are involved in picking up and transporting fare-paying passengers anywhere within New York City, it is highly probable that you are legally obligated to carry TLC insurance. Operating a for-hire vehicle (FHV) in New York City without this specific insurance is unlawful and can lead to severe penalties, including fines, vehicle impoundment, and the revocation of your TLC licence.

The broad spectrum of drivers who necessitate TLC insurance in NYC includes, but is not limited to, the following categories:

- Uber and Lyft Drivers: Despite the ride-hailing apps offering some level of coverage, it is supplementary, and drivers still require their own TLC policy to ensure continuous, comprehensive protection.

- Black Car Drivers: These are typically pre-arranged, high-end private car services, often catering to corporate clients or luxury travel.

- Livery Drivers: Similar to black cars, livery services are usually pre-booked and operate outside the traditional yellow cab system.

- Green and Yellow Taxi Drivers: The iconic yellow cabs, authorised to pick up street hails anywhere in Manhattan and at airports, and the green boro taxis, permitted to pick up street hails in the outer boroughs and northern Manhattan.

- Limousines and Luxury Limousines: Operators of these vehicles, ranging from standard limos to larger, high-capacity luxury vehicles.

- Commuter Van Drivers: Those operating vans that transport multiple passengers along fixed or flexible routes.

- Paratransit Service Drivers: Vehicles providing specialised transportation services for individuals with disabilities.

Essentially, if your vehicle is engaged in commercial passenger transport within New York City, TLC insurance is a mandatory component of your operational toolkit. It's the cornerstone of legal and responsible for-hire driving in the metropolis.

What Does TLC Insurance Encompass?

The exact scope of coverage provided by a TLC insurance policy can vary, depending on the specific provider and the limits chosen by the driver. Some drivers, particularly those operating higher-capacity or luxury vehicles, may opt for or be required to carry higher limits than others. However, there are several fundamental components that are universally included in TLC insurance, designed to offer robust protection:

- Liability Coverage: This is a cornerstone of any insurance policy and is particularly crucial for commercial drivers. It includes:

- Property Damage Liability Coverage: This vital component covers any damage you might cause to another person's property. For example, should you be involved in an accident in NYC and your vehicle collides with someone else's car, fence, or building, your TLC insurance's property damage liability coverage would be responsible for the repair or replacement costs.

- Bodily Injury Liability Coverage: This covers medical expenses, lost wages, and pain and suffering for others who are injured as a result of an accident you cause.

- Personal Injury Protection (PIP) Coverage: Also known as "no-fault" insurance in some contexts, PIP is designed to cover medical expenses, lost wages, rehabilitation costs, and certain other related expenses for you and your passengers after an accident, regardless of who was at fault. This helps ensure that immediate medical care and financial support are available without the need to determine fault first, streamlining the post-accident process.

- Uninsured Motorist Coverage: This crucial protection steps in when you are involved in a collision with a driver who either does not carry liability insurance or whose insurance limits are insufficient to cover the damages they cause. It helps to cover your medical expenses and, in some cases, property damage, ensuring you are not left financially vulnerable due to another driver's negligence or lack of proper cover.

It is important for drivers to thoroughly understand these components and ensure their policy limits meet or exceed the minimum requirements set by the New York City Taxi & Limousine Commission. This comprehensive suite of coverages ensures that drivers are adequately protected against the myriad risks associated with commercial driving in a busy urban environment.

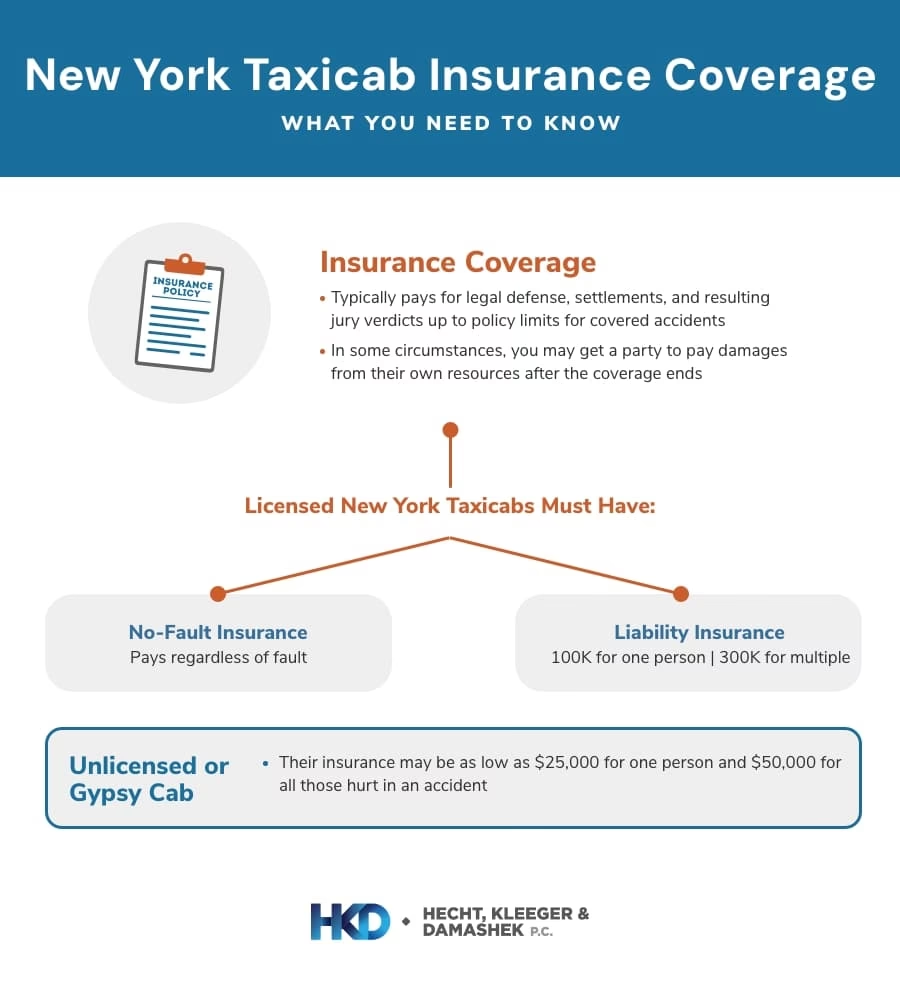

Minimum TLC Insurance Requirements

The New York City Taxi & Limousine Commission establishes specific minimum coverage requirements, which can vary based on the type and capacity of the vehicle being operated. This differentiation ensures that vehicles carrying more passengers or operating under different service models have appropriate levels of financial backing in case of an incident. For instance, the mandated limits for livery vehicles and black cars differ from those for luxury limousines or commuter vans, reflecting the varying risks and potential liabilities.

However, the majority of for-hire vehicles fall under the 1-7 passenger vehicle minimum insurance requirements. These are the most common limits drivers will encounter:

| Coverage Type | Minimum Requirement (1-7 Passenger Vehicles) |

|---|---|

| Liability Coverage per Person | $100,000 |

| Liability Coverage per Accident | $300,000 |

| Personal Injury Protection (PIP) | $200,000 |

It's crucial to note that the more seating capacity your vehicle possesses, the higher your insurance requirements will become. As an illustrative example, a driver operating a 20-passenger luxury limousine faces significantly higher obligations, requiring $5 million of liability coverage per accident, alongside a $200,000 personal injury protection policy. This scaled approach to requirements underscores the TLC's commitment to ensuring that vehicles with greater potential for passenger impact carry commensurate levels of insurance protection.

The cost of TLC insurance in New York City is akin to that of a comprehensive commercial car insurance policy, reflecting the increased risks and liabilities associated with for-hire driving. Generally, drivers can anticipate paying between $125 to $200 per month for TLC insurance in NYC, which translates to an annual expenditure of approximately $1,500 to $2,400. However, this is merely an average, and the actual premium you pay can vary quite substantially based on a multitude of influencing factors.

Key determinants of your TLC insurance premium include:

- Driving History: A clean driving record, free of accidents, moving violations, or serious infractions, is paramount. Insurers view drivers with a history of safe driving as lower risk, which typically results in more favourable rates.

- Years of Experience as a Commercial Driver: More experienced commercial drivers, particularly those with a proven track record of safe operation in a for-hire capacity, often qualify for lower premiums.

- Claim and Accident History: Any previous insurance claims or at-fault accidents will almost certainly drive up your rates. Insurers analyse this history to predict future likelihood of claims.

- Police and Citation History: Tickets for speeding, reckless driving, or other traffic violations signal higher risk to insurers, leading to increased costs.

- Vehicle Make, Model, Type, and Safety Rating: The specific vehicle you drive plays a significant role. Newer, safer vehicles with advanced safety features might attract lower rates. Conversely, high-performance or more expensive vehicles can lead to higher premiums due to higher repair or replacement costs.

- Driver Age: Younger, less experienced drivers typically face higher premiums, as they are statistically considered to be at a higher risk of accidents. As drivers gain experience and mature, their rates tend to decrease, assuming a clean record.

To put this into perspective, a young and relatively inexperienced driver who has had one at-fault accident within the last three years might find themselves paying well over $200 per month for TLC insurance in NYC. Conversely, an older, seasoned driver with an impeccable driving record could potentially secure coverage for less than $125 per month. This wide variance underscores the importance of maintaining a clean driving history and actively seeking competitive quotes.

Securing Your TLC Policy: A Practical Approach

Acquiring TLC insurance in New York City is a specialised process that typically involves engaging with auto insurance brokers who operate within the metropolitan area. These local insurance brokers possess invaluable expertise in the unique requirements of TLC insurance and can assist you in identifying the most suitable policy tailored to your specific needs as a for-hire driver.

Many reputable brokers will actively shop around on your behalf, comparing offerings from multiple insurance providers to help you secure the most comprehensive coverage at the most competitive price. Furthermore, some brokers specialise in offering highly specific coverage options designed for unique segments of the for-hire market. This could include policies specifically for black cars, yellow cabs, green taxis, livery vehicles, or even paratransit services, among other niche requirements. Their specialisation ensures that you receive a policy that precisely matches the operational parameters of your driving service.

For added assurance and to ensure you are dealing with a legitimate and licensed provider, it is always a wise strategy to consult official sources. The New York State's Department of Motor Vehicles (DMV) often recommends checking a list of licensed insurance companies on their official website. By selecting an insurer from this verified list, you can have greater confidence in the legitimacy and reliability of your chosen TLC coverage provider. This due diligence is crucial to avoid fraudulent policies and ensure your legal compliance and financial protection while driving commercially in New York City.

Frequently Asked Questions About TLC Insurance

Navigating the requirements for commercial driving in a city as unique as New York can bring forth numerous questions. Here are some of the most common queries regarding TLC insurance:

Is TLC insurance required outside New York City?

No, TLC insurance is a specific requirement for for-hire vehicles operating within the five boroughs of New York City and is regulated by the New York City Taxi & Limousine Commission. If you operate a for-hire vehicle outside of NYC, you would typically need a standard commercial auto insurance policy applicable to that jurisdiction, but not necessarily 'TLC insurance' as defined by NYC.

Can I simply use my personal car insurance policy for commercial driving in NYC?

Absolutely not. Your personal car insurance policy is explicitly designed for private use and will not cover you when you are driving for commercial purposes, such as picking up fare-paying passengers. Attempting to operate commercially with only personal insurance leaves you completely exposed to significant financial liabilities in the event of an accident or incident.

Does Uber or Lyft provide full insurance coverage for their drivers in NYC?

While Uber and Lyft do provide some levels of insurance coverage, particularly when a passenger is in your vehicle or you are en route to pick one up, this coverage is often limited and may not cover all scenarios, especially during periods when you are logged into the app but awaiting a ride request. TLC insurance is essential to bridge these gaps and provide comprehensive, continuous coverage as mandated by NYC regulations.

What happens if I operate a for-hire vehicle in NYC without TLC insurance?

Operating a for-hire vehicle in New York City without valid TLC insurance is illegal. Consequences can be severe and may include substantial fines, impoundment of your vehicle, and the suspension or revocation of your TLC driver's licence. Furthermore, you would be personally responsible for all damages, medical expenses, and legal costs arising from any accident, which could be financially ruinous.

Is TLC insurance the same as a standard commercial auto insurance policy?

TLC insurance functions similarly to a standard commercial auto insurance policy in that it covers vehicles used for business purposes. However, it is a highly specialised form of commercial insurance tailored specifically to meet the stringent regulations and unique requirements set forth by the New York City Taxi & Limousine Commission. It includes specific coverages and limits mandated for for-hire operations within NYC that might not be found in a generic commercial policy.

Final Word on NYC TLC Insurance

New York City truly stands as a unique entity, not least in its approach to regulating its extensive network of for-hire vehicles. It is one of the very few cities in the United States that strictly mandates drivers to carry a specific and specialised type of motor insurance: TLC insurance. As governed by the New York City Taxi and Limousine Commission (TLC), this essential coverage is a non-negotiable requirement for certain drivers operating within the city's bustling boundaries.

TLC insurance is a robust policy designed to provide comprehensive protection, typically encompassing crucial elements such as property damage liability coverage, personal injury protection (PIP) coverage, and uninsured motorist coverage. These components collectively ensure that drivers, their passengers, and the general public are adequately protected against the myriad risks inherent in commercial driving in a dense urban environment.

In essence, TLC insurance operates much like a commercial auto insurance policy, but with the added layer of specificity required by NYC's unique regulatory framework. Whether you are contemplating a career with a rideshare company like Uber or Lyft in New York City, or planning to drive a traditional taxi or limousine, securing a commercial policy that meets TLC standards is not just advisable – it is a legal imperative. Without it, your personal car insurance policy will simply not provide the necessary cover, leaving you exposed to significant financial and legal risks.

For those embarking on this journey, understanding and complying with New York City's TLC insurance requirements is the first and most critical step. It ensures not only your legal standing but also your financial security and peace of mind as you navigate the iconic streets of one of the world's most vibrant cities.

If you want to read more articles similar to NYC TLC Insurance: A UK Driver's Guide, you can visit the Insurance category.