07/09/2020

Running a limited company comes with its fair share of responsibilities, and understanding taxes is right up there on the list. Taxes can feel like a maze at first, but getting a handle on what you owe and when to pay can save you a lot of stress, and money, in the long run.

For limited companies, the main tax to tackle is Corporation Tax, which is calculated on your business profits after expenses and salaries are deducted. Unlike sole traders, limited companies don’t pay income tax directly on profits. Instead, you’ll pay Corporation Tax, currently set between 19% and 25%, depending on your company’s earnings. On top of that, there’s VAT and employer National Insurance contributions to take into account, depending on your business setup. Sounds like a lot? Don’t worry, we’ll break it all down so you know exactly what’s expected and how to stay on top of it.

- Understanding Limited Company Taxes

- Corporation Tax: The Core Obligation

- VAT and When It Applies

- Employers' National Insurance Contributions (NIC)

- Personal Tax Implications for Directors

- Taxable Income Explained

- Deductions and Allowances for Limited Companies

- Other Taxes Limited Companies May Face

- How To Calculate Corporation Tax

- Tips To Minimise Tax Liability Legally

- Should I take a salary from my limited company?

- Conclusion

- Frequently Asked Questions

- Do all limited companies pay the same Corporation Tax rate?

- When does a company need to register for VAT?

- What expenses are deductible for limited companies?

- How can directors reduce their tax liability?

- What is the marginal relief for Corporation Tax?

- Are directors personally taxed on company profits?

- What is the Annual Investment Allowance (AIA)?

Understanding Limited Company Taxes

Limited company taxes are distinct from taxes for sole traders or partnerships due to the unique legal and financial structure of the business. A limited company is treated as a separate legal entity, which means it pays taxes on its profits rather than passing them directly to owners or shareholders. Exploring these differences helps you manage your tax liabilities effectively and stay compliant with regulations.

Corporation Tax: The Core Obligation

Corporation Tax is central to your limited company tax responsibilities. It's calculated on taxable profits, which include any income from trading activities, investments, or asset sales exceeding their original value. After deducting allowable expenses like wages, rent, and utilities, the remainder forms the taxable profits.

Currently, Corporation Tax rates range from 19% to 25%, depending on your company's profit levels. Businesses with lower earnings remain at 19%, while those with profits over £250,000 pay closer to the upper threshold. Paying this tax requires filing a CT600 form to HMRC, usually submitted online as part of your annual accounts process. Once filed, you have up to nine months and one day to make the payment.

Current Corporation Tax Rates (Financial Year Starting 1 April 2024)

Understanding Corporation Tax rates is critical for managing your limited company’s tax obligations. The rates you pay depend on your profits and accounting period.

- Small Profits Rate: 19% on profits up to £50,000.

- Full Rate: 25% on profits exceeding £250,000.

- Marginal Relief: For profits between £50,001 and £250,000, a marginal relief mechanism creates a sliding scale of rates, gradually increasing the effective tax rate up to 25%.

Companies with associated businesses divide the thresholds (£50,000 and £250,000) between the total number of those companies. For example, if your company has two associated companies, the upper threshold reduces to £83,333. Short accounting periods also reduce these thresholds proportionately.

A lower tax rate of 10% applies to profits linked to patent exploitation. This favourable rate includes trading profits derived from selling patented products, beyond royalties.

VAT and When It Applies

If your company's turnover exceeds £85,000 in a 12-month rolling period, registering for Value Added Tax (VAT) is mandatory. VAT is added to the sale of goods or services, with standard rates at 20%. But, some goods qualify for reduced rates, such as children's car seats or energy supplies taxed at 5%. By adequately tracking turnover, you can maintain compliance and avoid late registration penalties.

If your turnover is below the VAT threshold, you can still choose to register voluntarily to claim back VAT on business expenses. This option works well for businesses investing heavily in taxable goods or services. Remember, once registered, VAT returns must be filed quarterly.

Employers' National Insurance Contributions (NIC)

If your company employs workers or if you, as a director, draw a salary above the secondary threshold (£9,100 annually in 2023-2024), you'll need to make Employers' NIC payments. This amount is 13.8% of salaries or wages exceeding the specified threshold. Directors frequently manage their salaries to minimise NIC liabilities by combining lower salaries with dividends.

Personal Tax Implications for Directors

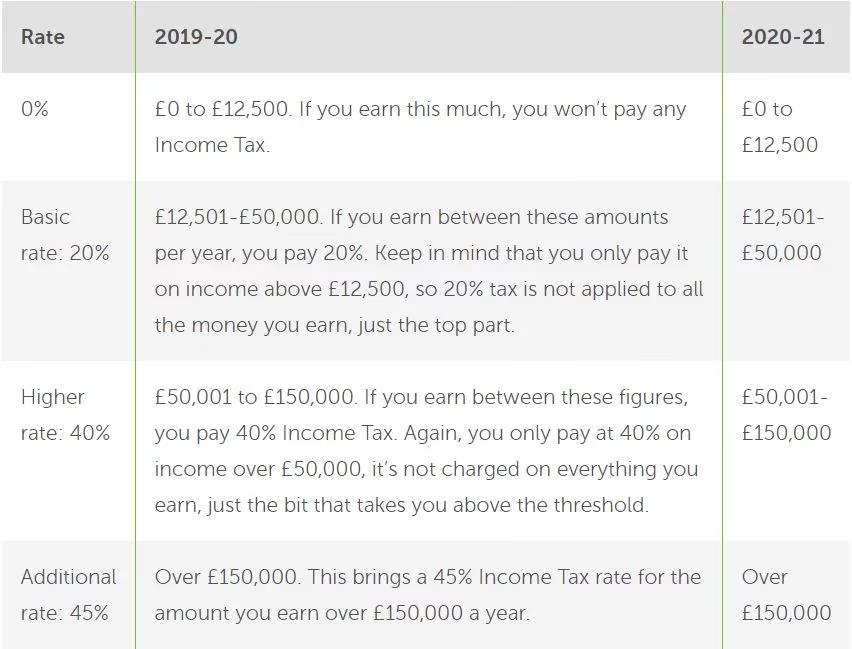

As a director or shareholder, you'll face personal tax responsibilities. The salary drawn from the company is taxed under PAYE (Pay As You Earn), while dividends are subject to different rates after utilising the £1,000 annual dividend allowance. In 2023-2024, basic-rate taxpayers pay 8.75% on dividends, higher-rate taxpayers pay 33.75%, and additional-rate taxpayers pay 39.35%. Striking the right balance between dividends and salary can optimise your overall tax payments.

Taxable Income Explained

Understanding taxable income is essential for calculating how much Corporation Tax your limited company owes. It's the amount left after deducting allowable expenses from your total income. Ensuring accuracy in these calculations helps you manage cash flow better.

What Counts as Taxable Income

Taxable income includes all profits generated by your limited company, whether from trading activities, investments, or the sale of business assets. For example:

- Trading profits: Revenue from selling goods or services minus allowable business expenses.

- Investment income: Earnings from interest, dividends, or rental income received by the company.

- Asset disposals: Profits from selling business equipment, property, or inventory.

It's important to maintain records of all revenue streams and classify them correctly. For example, income from an asset sale can attract different tax rates compared to trading profits. Keeping detailed records reduces risks during HMRC audits and ensures compliance.

Deductions and Allowances for Limited Companies

Taking full advantage of deductions and allowances can significantly reduce taxable income, helping your company retain profits. Here's a breakdown of commonly used ones:

- Business expenses: Qualify for deduction if they're wholly and exclusively for business purposes. Common examples include rent, salaries, utilities, and marketing.

- Capital allowances: Enable you to claim tax relief on investments in assets like machinery, vehicles, or technology. For instance, under the super-deduction allowance, you can claim 130% relief on qualifying assets until March 2023. The Annual Investment Allowance (AIA) provides up to £1,000,000 in tax relief for business purchases like equipment or tools.

- Research and Development (R&D) tax credits: Reward innovation by offering up to 33.35% relief on R&D expenditure, even for unsuccessful projects.

- Loss relief: Lets you offset trading losses against other income or carry them forward to future tax years. Constraints like the cap on Income Tax relief apply.

Using accounting software or working with a professional accountant ensures you don't miss out on these opportunities. Always stay updated with current regulations to adapt accordingly. For instance, contribution limits for pensions have changed, permitting £60,000 annually as a deductible company expense starting FY 2024.

Other Taxes Limited Companies May Face

Limited companies may encounter additional tax obligations depending on their size, structure, and business activities. Understanding these taxes ensures compliance and allows you to optimise your financial strategy.

VAT (Value Added Tax)

VAT applies to most goods and services sold in the UK. If your VAT-taxable turnover exceeds £90,000 within 12 months (effective 1 April 2024), registration is mandatory. It's also required if you anticipate exceeding this threshold in the next 30 days or if your company supplies goods or services to the UK from outside the country. Once registered, you'll need to charge VAT on your products, submit quarterly VAT returns, and remit any owed VAT to HMRC.

Smaller businesses with a turnover below the threshold may voluntarily register for VAT. This option can allow you to reclaim VAT on business purchases like equipment, utilities, and materials, helping reduce expenses. Voluntarily registering might suit you if you frequently buy VATable goods or aim to appear more established to clients. But, weigh this benefit against the administrative burden of compliance before deciding. Accurate record-keeping is essential, whether filing VAT quarterly or using the Flat Rate Scheme for simpler returns.

Employers' National Insurance Contributions

Limited companies with employees are liable for Employers' National Insurance Contributions (NICs). This tax applies to salaries above the Secondary Threshold (£9,100 for 2024/25), at a rate of 13.8%. Registered employers calculate and pay these contributions alongside employee pay under the PAYE system.

An Employment Allowance of £5,000 may reduce your NIC liability, making it a valuable relief for smaller employers. To qualify, annual NIC bills must not exceed £100,000, and certain exclusions apply. Taking advantage of this allowance could significantly lower your costs. Directors drawing a salary from the company also fall under NIC rules. Balancing salaries and dividends strategically helps optimise tax efficiency. Many use a tailored payroll system or professional advice to navigate thresholds and apply allowances correctly, ensuring accurate reporting to HMRC.

How To Calculate Corporation Tax

Calculating Corporation Tax involves determining the taxable profits of your limited company and applying the correct tax rate. Taxable profits include trading income, investments, and gains from the disposal of assets, minus allowable expenses and deductions.

Steps To Work Out the Tax Due

- Calculate total income: Add all forms of income your company earned during the financial year, including sales revenue, investment income, and profits from asset sales. For instance, a company generating £300,000 from sales and £20,000 from investments has a total income of £320,000.

- Deduct allowable expenses: Subtract business expenses incurred solely for company operations. Examples include rent, utilities, employee wages, and certain travel costs. For clarity, allowable expenses exclude personal costs, such as suits for meetings.

- Claim deductions and reliefs: Use available allowances and reliefs to lower taxable income. Examples include Annual Investment Allowances for equipment purchases or R&D tax credits for innovation expenses. For example, if £50,000 qualifies as an R&D expense, you can claim it to reduce your taxable income.

- Subtract capital allowances: Deduct capital allowances for business assets like machinery or vehicles. For example, claiming 100% of the cost of a £25,000 machine under the Annual Investment Allowance reduces taxable profits directly.

- Apply loss relief: Offset current or previous losses against taxable profits. For instance, a £10,000 loss from the previous year can reduce current taxable income from £100,000 to £90,000.

- Determine the correct tax rate: Apply the applicable Corporation Tax rate based on profits. Use the small profits rate of 19% for taxable profits under £50,000, while profits above £250,000 are taxed at 25%. Marginal relief is available for profits between £50,001 and £250,000, gradually increasing the rate.

- Calculate tax payment: Multiply taxable profits by the Corporation Tax rate. For example, profits of £80,000 at 19% equate to a £15,200 tax liability.

Tips for Efficiency and Accuracy

- Maintain detailed records: Track income, expenses, and asset purchases during the year. Accurate financial records simplify calculations and reduce errors during filing.

- Use accounting software: Invest in reliable accounting tools for automated calculations. These guarantee compliant tax processes and provide accurate reports for filing.

- Seek expert advice: Engage a professional accountant to optimise deductions and guarantee compliance. Accountants identify additional allowances like R&D tax credits and make best possible use of reliefs.

By following these steps and tips, you can calculate Corporation Tax efficiently while ensuring compliance with HMRC regulations.

Tips To Minimise Tax Liability Legally

Reducing your company’s tax bill within legal boundaries requires using allowances, efficient planning, and strategic approaches.

Using Allowances and Reliefs

Allowances and reliefs are fundamental to reducing taxable profits. They enable you to deduct certain costs and investments directly from your income before Corporation Tax is applied. The Annual Investment Allowance (AIA), currently set at £1 million until 31 March 2023, allows you to claim 100% tax relief on qualifying plant and machinery purchases in the same financial year. For example, if your company invests £800,000 in equipment, you can immediately deduct this from your taxable profits. Capital allowances also apply to other fixed assets. If an asset exceeds the AIA cap, it falls under the writing-down allowance at 18% for standard equipment or 6% for long-term assets like building fixtures. Research and Development (R&D) tax credits offer relief for innovative projects. For instance, qualifying small companies can receive an additional deduction of up to 130% on R&D costs, significantly reducing tax liabilities. Loss relief is another powerful tool. If your business incurs a loss, you can offset it against profits from the previous year, reducing taxable income. Alternatively, unused losses can carry forward to offset future profits. Keeping detailed records ensures you can maximise these reliefs effectively.

Planning for Tax Efficiency

Tax efficiency comes down to strategising your income and expenses to lower liability legally. Salary and dividend planning is a popular method for company directors. By balancing a reasonable salary with dividend payments, you minimise income tax and National Insurance, while maintaining Corporation Tax obligations. For example, taking a salary just below the National Insurance threshold and the remainder as dividends can reduce your overall tax bill.

Claiming for genuine business expenses is equally indispensable. Expenses purely for commercial use, such as travel, uniforms, office supplies, or financial services, are deductible. Guarantee that these costs are wholly and exclusively for the company—personal use disqualifies an expense. For instance, laptops purchased for business qualify, but any significant private use of these assets triggers an add-back when calculating tax.

Consider perks like tax-free incentives. Some benefits, such as mobile phones or employee assistance schemes, can be provided without tax implications, offering relief for the company. Also, if you work from home, you can claim deductions for a proportionate share of utility bills, broadband, or mortgage interest.

Finally, reviewing your VAT scheme can make a difference. Flat-rate VAT schemes simplify administration and may save money for businesses with limited VAT-charged expenses. For turnover under £85,000, voluntary VAT registration allows you to reclaim VAT on purchases, though additional administrative costs should be weighed.

Strategic tax preparation ensures compliance with HMRC while lowering liabilities. Collaborating with accounting experts creates opportunities to explore savings unique to your business model.

Should I take a salary from my limited company?

Starting a limited company is often a sensible choice for self-employed workers, but it can present you with a lot of things to get your head around – especially when it comes to deciding how much to pay yourself. Whilst you may just want to put as much money as you can into your bank account as a result of your business efforts, paying yourself from a limited company requires a little more strategy. When paying yourself, you need to do it in the most tax-efficient way – which is usually done by taking a combination of a low salary and dividends from your limited company.

The salary will be paid to you as a director, in the same way as a regular employee. Before you calculate how much you should take, you’ll need to make sure that you meet all your reporting and tax filing responsibilities for running your payroll under HMRC’s Real-Time Information (RTI) rules or you may incur fines and penalties. You'll also need to make sure you follow HMRC's rules on issuing dividends.

Why take a salary?

There are two main reasons to take a salary from your limited company:

- It’s counted as an allowable business expense, which means it lowers the amount of Corporation Tax your company pays.

- If the salary is above the Lower Earnings Limit (e.g., £6,396 in 2024/25), you accrue qualifying years towards your state pension.

Why would I want to take a low salary?

Under HMRC’s rules, ‘office holders’ (i.e., people who hold a position at a company but don’t have a contract, or receive regular salary payments) aren’t subject to the National Minimum Wage Regulations unless there is a contract of employment in place. A low salary can be paid which means you do not have to pay Income Tax or National Insurance Contributions (NICs) on that salary.

As a UK taxpayer, each year you’ll have a Personal Allowance – any income you receive up to the Personal Allowance is free from Income Tax, which was frozen until 2026 by chancellor Rishi Sunak. In the 2024/25 and 2025/26 tax years, this threshold is £12,570.

There are also National Insurance (NI) thresholds to be aware of. They’re all currently lower than the Personal Allowance and are important when setting your salary:

- The Lower Earnings Limit: As long as your salary is set above this level, you’ll retain your State Pension contribution record.

- The National Insurance (NI) Primary threshold: As long as your salary is below this level, you won’t need to pay any employee’s NICs.

- The National Insurance (NI) Secondary threshold: As long as your salary is below this level, your limited company (as your employer) won’t need to pay any employer’s NICs.

So, the aim is to set your salary at a level that is above the Lower Earnings Limit to obtain the benefits of qualifying for the state pension, but below the level where you’ll need to pay either employee or employer’s NI. Win, win!

National Insurance Thresholds and Director's Salary

For the 2025/26 and 2024/25 tax years, if your salary is above the National Insurance (NI) ‘Lower Earnings Limit’ (£6,500 and £6,396 respectively) but below the NI ‘Primary Threshold’ (£12,570 per year), you don’t pay employee’s NI contributions, but you do retain your State Pension contribution record. However, your limited company would have to pay employer’s NI contributions on any salary above the NI ‘Secondary Threshold’ which is £9,100 (2024/25).

For the 2024/25 tax years, setting your salary at the NI Primary threshold would mean your company will need to pay Employer’s NI and your company’s profits will be reduced due to the increased salary costs. Any reduction in your company’s profits reduces the amount of dividends available to distribute to your company’s shareholders.

This means that the most tax-efficient salary for a limited company with a single director who has no other sources of taxable income for the 2024/25 tax years will usually be £758.33 per month (£9,100 for the tax year) which is the NI Secondary threshold amount.

For the 2025/26 tax year, the NI Primary threshold is £1,048 per month (£12,570 for the tax year). Although there will still be Employers NI to pay, there will be no payroll fees.

Why might I want to take a higher salary?

If your salary is set at a very low level, or if you don’t take a salary at all, there are disadvantages, such as:

- Reduced maternity benefits: Technically, to qualify for maternity benefits, you need to be “employed” and thus be compliant with the National Minimum Wage Regulations.

- Missing out on tax-free personal allowance: You could miss out on part of your annual tax-free personal allowance if your salary is paid at the NIC threshold and you have no other sources of income. (You should ensure that you understand the impact of the total amount of salary and dividends you take from your company and other sources of income on your available tax-free personal allowance).

- Reduced cover under insurance policies: Reduced cover under permanent health, critical illness, personal accident or similar policies, where payouts are calculated based on your earnings.

- Issues with National Minimum Wage Regulations: If you want to have a Contract of Employment.

- Loan or mortgage applications: When applying for a loan or a mortgage you may need to meet certain criteria which are unsympathetic to a low salary. However, there can be ways around this if you use a specialist self-employed mortgage broker.

Paying yourself in dividends

If your company makes a profit, which it hopefully will, then you have two options available to you. You can either reinvest your profit into the company or pay shareholders by issuing a dividend. The term “shareholder” simply refers to the owner(s) of the company. So, if you own and manage your limited company, you can pay yourself a dividend. This can be a tax-efficient way to take money out of your company, due to the lower personal tax paid on dividends. Through combining dividend payments with a salary, you can ensure that you’re at optimum tax efficiency.

Tax implications of taking a salary

As with regular full-time employees, all salaries will be subject to tax via Pay-as-you-earn (PAYE). With three separate PAYE ‘taxes’, the benefit of reducing your Corporation Tax liability by taking a higher salary can soon be outweighed by the additional tax paid.

Income tax

Income tax is cumulative on all employment earnings and other sources of income in a tax year. For example, if you’ve already earned £10,000 from any employment in a given tax year, your tax-free Personal Allowance will be reduced by this amount.

Employee National Insurance Contributions

Unlike Income Tax, employee National Insurance Contributions (NICs) aren’t cumulative. They are payable for each pay period (usually weekly or monthly). This means each new employment has a separate earnings threshold before NICs are due. For employees who are Higher Rate taxpayers, there’s a maximum limit on the amount of NICs to be paid. If you’re an employee (but not a director), this threshold is set as a monthly amount. If you’re paid over this amount in any given month, you’ll have to pay NICs even if your pay for the rest of the year is reduced. Directors have an annual threshold, which is 52 times the weekly threshold amount. When salary starts to go over this, they pay NICs.

Employer National Insurance Contributions

The threshold for employer NICs works in the same way as employees. For every salary amount your employee earns above the weekly National Insurance earnings threshold, the employer has to pay NICs at 13.8% for the 2024/25 tax year (unchanged from 2023/24). This also applies to your own director’s salary and represents another PAYE tax the company has to pay.

Putting it all together - the best way to pay yourself as a director

Taking all the above taxes together, in the 2025/26 and 2024/25 tax year, it’s usually tax-efficient for most limited company directors to take a monthly salary up to the NI Secondary threshold of £1,048 per month, or £12,570 per year for the 2025/26 tax year and £758.33 per month, or £9,100 per year for the 2024/25 tax year. As we mentioned at the start of this article, as the Lower Earnings Limit is below the point at which you pay employee or employer’s NICs, you’ll still accrue qualifying years for the state pension.

If you pay yourself a salary up to the relevant National Insurance threshold from your limited company, you won’t pay any Income Tax or National Insurance on it as long as it’s your only earnings. We usually recommend this option on the basis of tax efficiency. As a company director, you can choose the amount of salary you’re paid, but you may wish to get advice from one of our expert accountants to ensure you’re paying yourself in the most tax-efficient way.

Conclusion

Exploring the tax world as a limited company can feel complex, but with the right knowledge and planning, it becomes manageable. Staying informed about Corporation Tax rates, VAT obligations, and allowable deductions ensures you're not paying more than necessary.

By keeping accurate records, utilising tax reliefs, and seeking expert advice when needed, you can optimise your tax position while remaining compliant with HMRC rules. Proactive tax management not only saves money but also supports the long-term success of your business.

Frequently Asked Questions

Do all limited companies pay the same Corporation Tax rate?

No, Corporation Tax rates depend on profit levels. A small profits rate of 19% applies to profits under £50,000, while the main rate of 25% applies to profits above £250,000. Marginal relief is available for profits between £50,000 and £250,000.

When does a company need to register for VAT?

A company must register for VAT if its taxable turnover exceeds £85,000 in a 12-month period. Businesses below the threshold may voluntarily register to reclaim VAT on expenses, but should consider administrative responsibilities.

What expenses are deductible for limited companies?

Allowable expenses include business-related costs such as office supplies, travel, salaries, and equipment. Additional allowances like R&D tax credits, capital allowances, and loss relief help reduce taxable income and Corporation Tax liability.

How can directors reduce their tax liability?

Directors can optimise tax efficiency by balancing salaries and dividends, claiming legitimate business expenses, contributing to pensions, and leveraging reliefs such as the Employment Allowance. Strategic planning with an accountant is highly recommended.

What is the marginal relief for Corporation Tax?

Marginal relief applies to profits between £50,000 and £250,000, gradually increasing the Corporation Tax rate from 19% to 25%. This ensures businesses with mid-range profits face a tapered tax rate rather than a sudden jump.

Are directors personally taxed on company profits?

Directors are not taxed directly on company profits. Instead, they pay Income Tax on salaries and dividends received from the company. Strategic dividend planning can reduce personal tax liability.

What is the Annual Investment Allowance (AIA)?

The AIA allows companies to claim 100% tax relief on certain capital expenditures, like equipment and machinery, up to £1 million annually. This reduces taxable profits and, in turn, the Corporation Tax bill.

If you want to read more articles similar to Understanding Limited Company Taxes, you can visit the Taxis category.