28/01/2023

As a dedicated sole trader taxi driver in the UK, every penny counts. From fuel costs to licensing fees, the expenses can quickly add up. One area often overlooked, yet crucial for significant tax savings, is understanding capital allowances, especially when it comes to purchasing your vehicle. While the world of tax relief can seem dauntingly complex, particularly concerning second-hand assets, grasping these allowances can make a substantial difference to your bottom line. This article aims to demystify capital allowances for you, focusing on how they apply to your second-hand taxi, whether it's a traditional black cab or a standard car used for private hire.

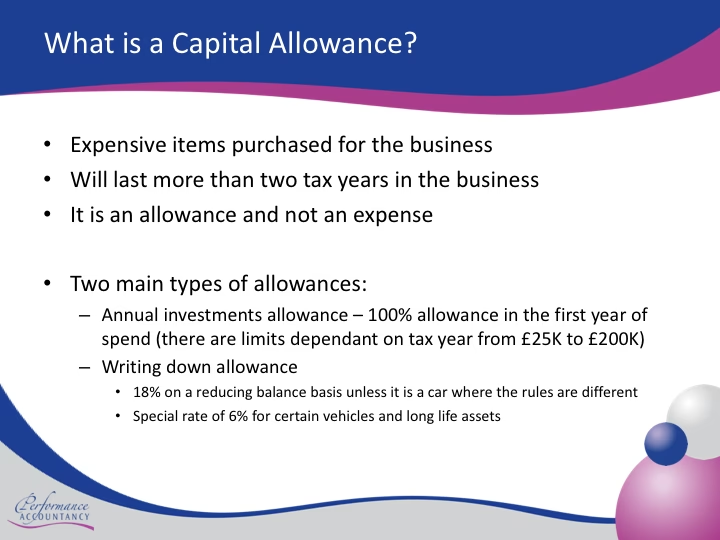

Capital allowances are a vital form of tax relief designed to help businesses, including sole traders like yourself, reduce their taxable profits when they invest in long-term assets. These 'fixed assets' are items you expect to use in your business for more than a year, and naturally, your taxi falls squarely into this category. Instead of deducting the entire cost of your vehicle as an immediate expense, capital allowances allow you to deduct a portion or, in some cases, the full value of the asset from your profits over time. The fundamental principle is simple: lower taxable profits mean a lower tax bill. It's an incentive from HMRC to encourage investment in business assets that contribute to productivity and growth.

It's important to differentiate capital allowances from everyday business expenses. While expenses cover items you expect to use up or replace within 12 months (like your taxi insurance, fuel, or minor repairs), capital allowances apply to durable assets like your vehicle. You must own the asset to claim capital allowances; leased vehicles, for example, are not eligible. This distinction is paramount, as miscategorising can lead to errors in your tax return.

- Why Capital Allowances Are Crucial for Sole Trader Taxi Drivers

- The Distinction: Cars vs. Commercial Vehicles

- Capital Allowances for Your Second-Hand Taxi

- Working Out Your Capital Allowance: Practical Examples

- The Impact of Business vs. Personal Use

- What Happens When You Dispose of Your Taxi?

- Comparison of Capital Allowances for Taxi Vehicles

- Frequently Asked Questions (FAQs)

- Seeking Professional Guidance

Why Capital Allowances Are Crucial for Sole Trader Taxi Drivers

For a sole trader taxi driver, the primary benefit of claiming capital allowances is the direct reduction in your tax liability. The purchase of a taxi, whether new or second-hand, represents a significant investment. By effectively reducing your profits through these allowances, you pay less income tax, freeing up valuable capital that can be reinvested into your business or used for personal needs. This immediate and ongoing financial relief is why understanding and correctly claiming capital allowances is not just an option, but a strategic necessity.

Furthermore, capital allowances offer a degree of flexibility. If, for instance, your taxable profits in a particular year are lower than the allowance you could claim, you might not be able to utilise the full amount immediately. However, the good news is that any unused allowance can often be carried forward to subsequent tax years. This creates a 'tax asset' on your balance sheet, allowing you to offset future profits and continue to benefit from the allowance until it's fully utilised. This carry-forward mechanism provides a safety net, ensuring that you don't lose out on relief even during leaner periods.

The Distinction: Cars vs. Commercial Vehicles

This is arguably the most critical and often confusing aspect for taxi drivers when it comes to capital allowances. HMRC has specific definitions for what constitutes a 'car' versus a 'commercial vehicle' for tax purposes, and this distinction profoundly impacts the type and amount of allowance you can claim. It's not always about how the vehicle looks, but how it's defined for tax.

- What counts as a 'Car' for Capital Allowances? HMRC generally considers a vehicle a 'car' if it's suitable for private use and wasn't built primarily for transporting goods. This includes most standard saloon cars, hatchbacks, and SUVs, even if you use them exclusively for private hire. Motorhomes are also included in this category.

- What doesn't count as a 'Car' (i.e., a 'Commercial Vehicle')? This is where it gets interesting for taxi drivers. Vehicles like vans, lorries, and crucially, purpose-built taxis such as traditional black cabs, are generally classified as commercial vehicles. This classification is vital because commercial vehicles often qualify for more generous capital allowances, specifically the Annual Investment Allowance (AIA), without being subject to the CO2 emission rules that apply to 'cars'.

Before purchasing your taxi, especially if it's a second-hand vehicle, it's paramount to ascertain its classification. A traditional London black cab, for example, will almost certainly be treated as a commercial vehicle, offering potentially greater tax relief than a standard saloon car used for private hire, even if both are second-hand.

Capital Allowances for Your Second-Hand Taxi

Now, let's address the core question: can a sole trader taxi driver claim capital allowances on a second-hand car? The answer is a resounding yes, but the specific allowance and the amount you can claim depend heavily on the vehicle's classification and, if it's considered a 'car', its CO2 emissions.

1. Annual Investment Allowance (AIA)

The AIA is often the most beneficial allowance for businesses, as it allows you to deduct the full cost of eligible plant and machinery, up to a certain limit (currently £1 million per year), from your profits in the year you buy them. This can significantly reduce your tax bill immediately. For taxi drivers, the key is that commercial vehicles – such as black cabs, purpose-built hackney carriages, or vans converted for taxi use – are typically eligible for the AIA. This means if you buy a second-hand black cab for your business, you could potentially claim 100% of its cost as an allowance in the first year.

It's important to note that the AIA generally does not apply to 'cars' as defined by HMRC (i.e., those suitable for private use and not primarily built for goods transport). This is a common point of confusion.

2. Writing Down Allowances (WDAs)

If your second-hand taxi is classified as a 'car' by HMRC, then you'll likely be claiming Writing Down Allowances. Unlike the AIA, WDAs allow you to deduct a percentage of the car's value from your profits each year, over a longer period. The rate depends on the car's CO2 emissions:

- Main Rate Allowance (18%): This applies to cars with CO2 emissions of 50g/km or less. This includes many newer second-hand electric cars, as well as some very low-emission hybrid or conventional vehicles. If your second-hand taxi falls into this category, you can claim 18% of its value each year.

- Special Rate Allowance (6%): This applies to cars with CO2 emissions above 50g/km. Most older or higher-emission second-hand cars used as taxis will fall into this category, allowing you to claim 6% of its value annually.

The 'value' for capital allowance purposes is generally what you paid for the car, plus any additional costs incurred to get it ready for business use, such as modifications for taxi meters or specific livery, assuming these costs are part of the capital expenditure and not just ongoing maintenance.

3. 100% First-Year Allowances (FYAs)

While less common for *second-hand* vehicles, it's worth noting that new, unused electric cars with zero CO2 emissions are eligible for a 100% First-Year Allowance. This allows you to deduct their full cost from your profits in the first year. If you happen to be the first business owner of a second-hand electric car that was previously owned by a private individual and never used for business, there might be a rare scenario where it could qualify, but typically this is for new vehicles only.

Working Out Your Capital Allowance: Practical Examples

Let's illustrate how these allowances might work for a sole trader taxi driver buying a second-hand vehicle:

Example 1: Purchasing a Second-Hand Black Cab (Commercial Vehicle)

- You buy a second-hand, purpose-built black cab for £30,000 to use solely for your taxi business.

- As a commercial vehicle, it's eligible for the Annual Investment Allowance (AIA).

- You can claim 100% of the £30,000 cost as an allowance in the first year. If your taxable profit for that year is £40,000, your taxable profit after claiming AIA would be £10,000 (£40,000 - £30,000). This significantly reduces your tax bill.

Example 2: Purchasing a Second-Hand Saloon Car (High Emissions 'Car') for Private Hire

- You buy a second-hand saloon car for £15,000 to use for private hire. Its CO2 emissions are 120g/km (placing it in the special rate pool).

- This vehicle is classified as a 'car' for capital allowances.

- You can claim Writing Down Allowances at the special rate of 6% each year.

- In the first year, you'd claim £900 (£15,000 x 6%). In subsequent years, the 6% is applied to the remaining 'written down value' of the asset.

Example 3: Purchasing a Second-Hand Electric Car (Low Emissions 'Car') for Private Hire

- You buy a second-hand electric car for £25,000 to use for private hire. It has 0g/km CO2 emissions.

- This vehicle is classified as a 'car' for capital allowances, but due to its low emissions, it falls into the main rate pool.

- You can claim Writing Down Allowances at the main rate of 18% each year.

- In the first year, you'd claim £4,500 (£25,000 x 18%).

The Impact of Business vs. Personal Use

As a sole trader, it's common to use your vehicle for both business and personal purposes. When claiming capital allowances, you must apportion the allowance based on your business use percentage. HMRC expects a fair and reasonable apportionment.

For instance, if your second-hand electric car (from Example 3) cost £25,000 and you determine that you use it 80% for business and 20% for personal travel, your capital allowance claim would be restricted. Instead of claiming £4,500 (18% of £25,000), you would claim £3,600 (£4,500 x 80%). Maintaining accurate mileage records (business vs. total) is crucial for justifying this split to HMRC.

What Happens When You Dispose of Your Taxi?

When you eventually sell, scrap, or otherwise dispose of your taxi, this is known as a 'disposal' for capital allowance purposes. At this point, you'll need to calculate a 'balancing adjustment'. This calculation compares the written down value of the asset (its value after all capital allowances have been claimed) with the amount you received for its disposal.

- If the disposal value is less than the written down value, you'll have a 'balancing allowance', which creates a further tax deduction.

- If the disposal value is more than the written down value, you'll have a 'balancing charge', meaning you may need to pay more tax.

This mechanism ensures that the total tax relief you receive over the asset's life accurately reflects its true cost to your business.

Comparison of Capital Allowances for Taxi Vehicles

| Vehicle Type (Second-Hand) | HMRC Classification | Eligible Allowance(s) | Key Consideration |

|---|---|---|---|

| Purpose-built Black Cab / Hackney Carriage | Commercial Vehicle | Annual Investment Allowance (AIA) or Writing Down Allowances | Often 100% deduction in first year via AIA if used solely for business. CO2 emissions are not a factor. |

| Standard Car (e.g., Saloon, SUV) for Private Hire (0-50g/km CO2) | Car | Writing Down Allowances (Main Rate - 18%) | Annual percentage deduction based on original cost. Business use apportionment required. |

| Standard Car (e.g., Saloon, SUV) for Private Hire (>50g/km CO2) | Car | Writing Down Allowances (Special Rate - 6%) | Annual percentage deduction based on original cost. Business use apportionment required. |

| New Electric Car (Zero CO2, Unused) | Car | 100% First-Year Allowance (FYAs) | Full cost deductible in first year. Very rarely applies to second-hand cars unless specific conditions met. |

Frequently Asked Questions (FAQs)

Q: Can I claim capital allowances if I lease my taxi instead of buying it?

A: No, you can only claim capital allowances on assets that your business owns. Leased vehicles are not eligible for capital allowances.

Q: Are maintenance and servicing costs for my taxi also considered capital allowances?

A: No, maintenance, servicing, fuel, and insurance costs are considered day-to-day running expenses. These are deductible from your profits as allowable business expenses, not capital allowances. Capital allowances are for the purchase of the long-term asset itself.

Q: What if I don't use the full amount of capital allowance available in one tax year?

A: If you don't have enough taxable profit to utilise the full capital allowance in one year, the unused portion can typically be carried forward to reduce your taxable profits in subsequent years. This creates a 'tax asset' on your balance sheet.

Q: Is it complicated to claim capital allowances on my tax return?

A: While the underlying rules are complex, the actual process of claiming on your self-assessment tax return involves completing the relevant capital allowances pages. However, ensuring your calculations are accurate and that you've applied the correct allowance for your specific vehicle type and usage can be challenging. It is highly recommended to seek advice from a qualified accountant.

Q: Does the age of the second-hand taxi affect the capital allowance I can claim?

A: The age of the second-hand taxi itself doesn't directly determine the allowance type or rate. What matters is whether it's classified as a 'car' or 'commercial vehicle' by HMRC and, if a 'car', its CO2 emissions. Its purchase price is the basis for the allowance calculation.

Seeking Professional Guidance

As you can see, capital allowances, especially for vehicles, are a nuanced area of UK tax. While this article provides a comprehensive overview for sole trader taxi drivers, the specifics can vary, and misinterpretations can lead to incorrect claims or missed opportunities for tax relief. The distinction between a 'car' and a 'commercial vehicle' for HMRC purposes is particularly critical for taxi drivers, as it can drastically change the available allowances.

For peace of mind and to ensure you're maximising your legitimate tax savings, it is always advisable to consult with a qualified accountant. They can provide tailored advice based on your specific circumstances, help you accurately calculate your allowances, and ensure your tax return is compliant with HMRC regulations. Their expertise can not only save you money but also prevent potential issues down the line. Don't let the complexity deter you; instead, see it as an opportunity to optimise your business's financial health.

If you want to read more articles similar to UK Taxi Drivers: Capital Allowances on Used Cars, you can visit the Taxis category.