14/04/2022

In an increasingly cashless world, where a quick tap of your card or phone pays for your taxi ride, understanding financial security is more critical than ever. Whether you're a busy passenger hailing a cab or a dedicated driver navigating the city streets, your bank account is at the heart of your transactions. But what happens if something feels amiss with your finances, even if no money has seemingly vanished yet? This comprehensive guide will walk you through the essential steps to protect your pounds, identify potential threats, and know exactly what to do if you suspect fraudulent activity, ensuring your journey is always financially secure.

- The Silent Threat: When Money Isn't Taken (Yet)

- When the Worst Happens: Reporting Fraudulent Transactions

- Beyond the Bank: Tackling Identity Theft

- Reclaiming Your Cash: The Refund Process

- The Tricky Territory of Scams: Authorised Push Payments (APP)

- Unhappy with the Outcome? Escalating Your Complaint

- Proactive Protection: Everyday Security Measures

- FAQs: Your Questions Answered

The Silent Threat: When Money Isn't Taken (Yet)

It's a common misconception that you only need to act when money disappears from your account. However, proactive vigilance can save you a significant amount of stress and financial loss. If you suspect someone might have unauthorised access to your bank account, even if no funds have been debited, immediate action is paramount. Perhaps you've just completed a taxi journey and now have a nagging feeling about the card reader, or you've simply lost your wallet with your cards inside. Don't wait for a suspicious transaction to appear.

Here are the crucial indicators and immediate steps:

- Lost or Stolen Details: If your bank card, phone, or security details (like PINs or passwords) have been lost or stolen, contact your bank or building society straight away. This is crucial even if you haven't seen any suspicious activity. They can immediately block cards and change security details to prevent future misuse. Imagine leaving your card in the back of a taxi – act fast!

- Unrecognised Payments on Statement: Regularly check your bank statements. Do you see payments you don't recognise? This could be a small test transaction by a fraudster before a larger sum is taken. Even if it's not a taxi payment, it warrants investigation.

- Unexpected Account Changes: Has your card reached its limit, or has your account unexpectedly gone into overdraft? If you weren't expecting this, it could indicate unauthorised activity. Perhaps a fraudulent 'taxi' booking has unexpectedly drained your funds.

To report these issues, locate your bank's dedicated security helpline number on their official website or a recent bank statement. Alternatively, visit a branch in person. Even without money being taken, your bank will take decisive action to protect your account, such as cancelling your card or changing security details. Remember, prevention is always better than cure.

When the Worst Happens: Reporting Fraudulent Transactions

If you discover that money has indeed been taken from your account without your permission, this is known as fraud, and it is unequivocally illegal. It's a distressing situation, whether it's related to a taxi payment, an online purchase, or something else entirely. The moment you become aware of it, you must act swiftly.

Upon contacting your bank, they will take immediate measures to secure your account and prevent further losses. This might involve cancelling your existing cards or cheque books and issuing replacements. It's vital to provide them with as much detail as possible about the suspicious transactions, including dates, amounts, and any merchants involved (e.g., if it was a phantom taxi payment).

Beyond contacting your bank, it is imperative to report the crime to the police through Action Fraud. Action Fraud is the UK's national reporting centre for fraud and cyber crime. They will log your report and provide you with a unique crime reference number. This number is not only crucial for police investigations but also serves as vital evidence when dealing with your bank or credit reference agencies. Even if the fraudulent transaction isn't directly related to a taxi ride, for instance, a scam email purporting to be from a taxi company, reporting it to Action Fraud is the correct procedure.

If you've received a scam email, text message, or phone call – perhaps a fake message about an overdue taxi fare or a discount offer – you can also report these scams directly to the relevant authorities, such as the National Cyber Security Centre (NCSC) or your mobile network provider, to help prevent others from falling victim.

Beyond the Bank: Tackling Identity Theft

Sometimes, the threat goes beyond just a single transaction. If someone uses your personal information – your name, address, date of birth – to open new bank accounts, obtain credit, or purchase services without your knowledge, this is called identity theft. It's a insidious crime that can have long-lasting repercussions on your financial standing. You might first suspect it if you begin receiving bank letters, bills, or correspondence from debt collectors for accounts or services you know nothing about. Perhaps a fake taxi company has opened credit in your name to fund their operations.

If you suspect you're a victim of identity theft, contact your bank or building society immediately. They will investigate the matter, take steps to protect your existing accounts, and refer the crime to the police. It is crucial to maintain a meticulous record of all conversations with your bank, including dates, times, and names of representatives you speak with. Keep copies of all letters, emails, and documents related to the fraud, as this paper trail will be invaluable throughout the resolution process.

Involving Credit Reference Agencies

If you suspect someone has applied for credit in your name – for example, if you're receiving letters about loans or credit cards you never applied for, possibly even related to a fraudulent taxi business venture – you must also contact the main credit reference agencies in the UK. These are:

- Experian

- Equifax

- TransUnion

Explain to each agency that you've been a victim of identity theft. Request a copy of your credit file to see what credit accounts or services are listed under your name. Identify any accounts you didn't apply for and ask for that information to be removed from your file. Each agency might only have a partial view of your financial history, so contacting all three ensures a comprehensive review and clean-up of your credit report.

You can also ask the credit reference agency to add a 'notice of correction' password to your file. This means that if anyone applies for credit in your name in the future, the agency will require this password, adding an extra layer of security. This is a powerful tool to protect yourself against further financial impersonation.

If you believe your details were obtained by mail theft or redirection, contact Royal Mail's Customer Enquiry Number on 03457 740 740. This could be relevant if a scammer redirected your bank statements to their address, for example, to facilitate identity theft.

Reclaiming Your Cash: The Refund Process

One of the most pressing concerns for victims of fraud and identity theft is getting their money back. Fortunately, UK banks and building societies generally have a responsibility to refund any money stolen from you as a direct result of fraud or identity theft. They should process this refund as quickly as possible, ideally by the end of the next working day after you report the problem. This rapid response is crucial for minimising the impact on your daily life, especially if you rely on immediate access to your funds for things like paying for a taxi ride home.

When a Refund Might Be Refused

However, there are specific circumstances where your bank might refuse to issue a refund. This typically occurs if they find evidence that you acted fraudulently yourself or were 'grossly negligent'. Gross negligence means you failed to take reasonable care to protect your account details. Common examples include:

- Sharing your PIN with someone else (even a trusted friend or family member).

- Writing down your password and leaving it in an easily accessible place.

- Responding to phishing scams that trick you into revealing security details.

It's important to differentiate between falling for a sophisticated scam and being grossly negligent. If you genuinely believed you were making a legitimate payment – perhaps for a taxi booking through a seemingly official, but actually fraudulent, website – this might not be considered gross negligence. The burden of proof for gross negligence lies with the bank.

If your bank refuses to refund your money and you believe their decision is unfair, your only recourse to recover the funds directly from the person who stole them would typically be through legal action, taking them to court. This can be a complex and costly process, which is why understanding your bank's refund policies and your rights is so important.

It can be even more challenging to recover your money if you willingly sent it to a scammer, even if you were tricked into doing so. This scenario, where you authorise a payment to someone you believe is legitimate but turns out to be a fraudster, is known as an 'authorised push payment' (APP) scam. Examples include paying a fake invoice for a taxi service you never received, or being tricked into transferring money for a bogus investment opportunity related to a taxi fleet.

Recognising the growing problem of APP fraud, most major UK banks have signed up to a voluntary Code of Conduct (the Contingent Reimbursement Model Code, or CRM Code). Under this code, banks generally agree to refund victims of APP scams, provided certain conditions are met:

- You followed any security warnings or advice provided by your bank.

- You genuinely believed the transaction was legitimate.

- You were not careless when making the payment.

Even if you feel you were careless because you fell for a clever scam, it is always worth approaching your bank for a refund. The sophistication of some scams can make them incredibly difficult to spot, and banks are increasingly recognising their role in protecting customers. They will assess your case based on the specific circumstances and the information you provide.

Here’s a comparative look at different fraud scenarios:

| Scenario | What Happened? | Bank's Action & Refund Likelihood | Your Primary Action |

|---|---|---|---|

| Unauthorised Transaction (Classic Fraud) | Money taken without your knowledge/permission (e.g., card cloned, details stolen). | High likelihood of refund, usually quick. Bank blocks cards. | Contact bank immediately, report to Action Fraud. |

| Identity Theft | Your details used to open new accounts/credit in your name. | Bank investigates, secures existing accounts. | Contact bank, credit reference agencies (Experian, Equifax, TransUnion), Royal Mail if post stolen. |

| Authorised Push Payment (APP) Scam | You were tricked into sending money to a scammer. | Refund based on CRM Code adherence (did you follow warnings, were you careless?). | Contact bank, report scam. |

Unhappy with the Outcome? Escalating Your Complaint

If you're not satisfied with how your bank or credit card provider has handled your fraud case or an APP scam claim, you have the right to make a formal complaint. All financial institutions have a complaints procedure they must follow. First, exhaust their internal complaints process. This usually involves contacting their dedicated complaints department and waiting for their final response.

If, after going through their internal process, you remain unhappy with their decision or the way your case was handled, you can escalate your complaint to the Financial Ombudsman Service (FOS). The FOS is an independent body that resolves disputes between consumers and financial businesses. They will review your case impartially and can order the bank to pay compensation or issue a refund if they find the bank acted unfairly or did not follow relevant rules and guidelines. This is a vital recourse for consumers who feel they have been let down by their financial provider, ensuring fair treatment.

Proactive Protection: Everyday Security Measures

While knowing what to do when things go wrong is crucial, the best defence is always a strong offence. Taking proactive steps can significantly limit your risk of becoming a victim of fraud, whether it's related to your taxi payments or other financial activities. Here are some key measures:

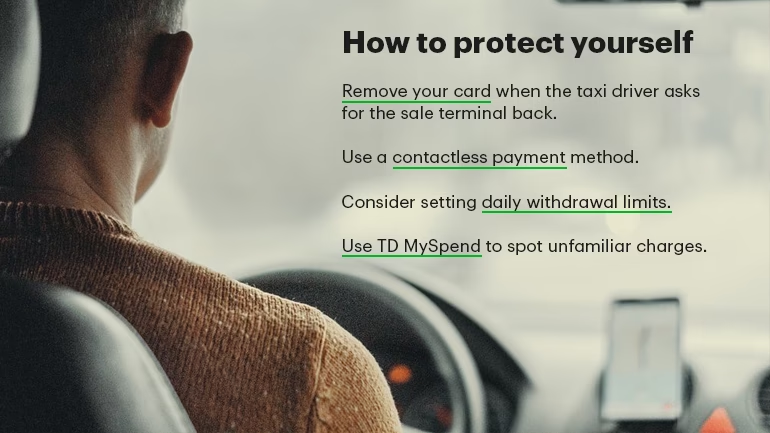

- Stay Alert to Scams: If you receive a call, text, or email from someone claiming to be your bank, the police, or even a taxi service, asking for personal details, your PIN, or to move money, be extremely wary. Legitimate organisations will never ask for your full PIN or password via these channels.

- Use Official Channels: When booking taxis or making payments, always use official apps, websites, or established payment terminals. Be suspicious of unusual payment links sent via text or email, especially if they claim to be for a taxi fare. Always double-check the URL.

- The 159 Service: If you receive a suspicious call claiming to be your bank, hang up and dial 159. This is a secure service that connects you directly to your bank's fraud department, bypassing potential scammers. It's a fantastic initiative by Stop Scams UK. Check their website to see if your bank is part of the 159 service. Calls are usually charged at the national rate.

- Secure Your Devices: Ensure your phone, tablet, and computer have up-to-date antivirus software and strong, unique passwords. Be cautious about using public Wi-Fi for banking or sensitive transactions, especially when waiting for a taxi or in a public transport hub.

- Check Your Bank's Advice: Your bank or building society's website is a treasure trove of advice on how to make your account more secure. They often have dedicated sections on fraud prevention, offering tips on creating strong passwords, recognising phishing attempts, and using their security features.

- Be Mindful of Your Surroundings: When making payments in public, such as paying your taxi driver, ensure no one is looking over your shoulder when you enter your PIN. Always cover the keypad.

FAQs: Your Questions Answered

Q: Can I get scammed by a taxi driver?

A: While the vast majority of taxi drivers are honest, reputable professionals, there are rare instances of individuals attempting scams. This is typically not through direct fraud on the payment terminal itself (as these are usually regulated), but rather through inflated fares, demanding cash for a pre-paid journey, or suggesting an unofficial payment method. Always use licensed taxis and official apps, confirm the fare before starting the journey, and use the official payment methods.

Q: What if my card details were skimmed during a taxi payment?

A: If you suspect your card was skimmed (details illegally copied) during a taxi payment, contact your bank immediately to report it and cancel your card. Regularly check your statement for any suspicious transactions. Reputable taxi payment terminals are designed to be secure, but vigilance is always key.

Q: How do I know if a payment link from a taxi service is legitimate?

A: Always be suspicious of unexpected payment links. Legitimate taxi services typically integrate payments directly into their app or use secure, well-known payment gateways. If you receive a link via text or email, check the sender's address carefully for discrepancies, and never click on links if you're unsure. If in doubt, contact the taxi company directly via their official phone number or website to verify the payment request.

Q: Is paying for a taxi with cash safer?

A: Paying with cash eliminates the risk of digital card fraud or skimming. However, it comes with its own risks, such as carrying large amounts of money or not having exact change. Many modern taxi services are moving towards cashless payments for convenience and record-keeping. The 'safest' method often depends on your personal comfort level and the specific circumstances of your journey.

Q: What if I paid a scammer for a fake taxi booking or service?

A: This falls under an Authorised Push Payment (APP) scam. Contact your bank immediately and explain you were scammed. They will investigate under the CRM Code. Also, report the scam to Action Fraud. Provide all details, including the website or contact method used by the scammer.

Q: What is the 159 service and how does it help?

A: The 159 service is a secure way to connect directly to your bank's fraud department if you receive a suspicious call. Instead of calling a number given by the potential scammer, you hang up and dial 159. It's designed to stop fraudsters who try to trick you into transferring money or giving away personal details. It's a crucial tool in the fight against impersonation scams.

By staying informed, remaining vigilant, and knowing the correct steps to take, you can significantly enhance your financial security, whether you're navigating the bustling streets of London in a black cab or processing payments as a licensed driver. Your money is hard-earned, so ensure it stays safe.

If you want to read more articles similar to Secure Your Ride: Protecting Your Money in Taxis, you can visit the Taxis category.