03/04/2021

In recent years, the landscape of vehicle acquisition in the UK has undergone a significant transformation. Once dominated by outright purchases and traditional car loans, vehicle leasing has surged in popularity, with reports indicating more than five million leased vehicles now gracing UK roads. Historically, the vehicle leasing market was primarily the domain of businesses and large fleet customers. However, a notable shift has occurred, and personal vehicle leasing now commands the largest market share. This change has been partly driven by increased taxation on company cars, alongside a growing societal preference for 'usership' over traditional ownership.

For self-employed contractors, freelancers, or sole traders considering leasing a vehicle, either wholly or partly for business purposes, understanding the tax implications is paramount. A crucial question often arises: can vehicle leasing costs be offset against your business profits to reduce your overall tax bill? This comprehensive guide aims to address this very question, providing clarity on reporting and paying tax when you lease a vehicle for work if you're a self-employed individual in the UK.

- The Surging Popularity of Vehicle Leasing in the UK

- Understanding Vehicle Leasing: Pros and Cons for the Self-Employed

- How Does Vehicle Leasing Actually Work?

- Is Vehicle Leasing a Tax Deductible Expense in the UK?

- Reporting Vehicle Leasing Costs to HMRC

- Frequently Asked Questions (FAQs)

- Q: What exactly is an 'allowable expense' for tax purposes?

- Q: Can I claim 100% of my vehicle leasing costs?

- Q: How do I calculate the personal use proportion of my leased vehicle?

- Q: Where can I find the most up-to-date HMRC guidance on vehicle expenses?

- Q: Is Business Contract Hire (BCH) always the best option for a sole trader from a tax perspective?

The Surging Popularity of Vehicle Leasing in the UK

The remarkable growth in vehicle leasing isn't just a fleeting trend; it represents a fundamental change in how individuals and businesses approach their transport needs. The figure of over five million leased vehicles underscores how deeply integrated this option has become within the UK's automotive sector. While businesses and large corporations were the early adopters, the shift towards personal leasing highlights a broader appeal, extending to individual consumers and, critically for this guide, the self-employed.

Several factors contribute to this surge. The rising costs associated with outright car ownership, including significant upfront capital, depreciation, and maintenance, make leasing an attractive alternative. Furthermore, changes in company car taxation have nudged many employees towards personal leasing, and this sentiment has permeated the self-employed sector. The concept of 'usership' – enjoying the benefits of a vehicle without the long-term commitment and financial burdens of ownership – resonates strongly with those seeking flexibility and predictable budgeting.

Understanding Vehicle Leasing: Pros and Cons for the Self-Employed

Before delving into the specifics of tax deductibility, it's essential to grasp the broader advantages and disadvantages of vehicle leasing from the perspective of a self-employed individual. A balanced view will help you determine if leasing is the right financial and operational choice for your business.

Advantages of Leasing a Vehicle

- Access to Newer, Higher-Spec Vehicles: Leasing often enables you to drive a newer, perhaps more luxurious or technically advanced vehicle than you might otherwise be able to afford if purchasing outright. This can project a more professional image for your business and offer a more comfortable driving experience.

- Enhanced Reliability and Reduced Hassle: Newer cars are inherently less prone to mechanical breakdowns, which translates to less time off the road and fewer unexpected repair costs. For a self-employed individual, a reliable vehicle is crucial for maintaining business operations and client commitments.

- Predictable Monthly Payments: Leasing typically involves a relatively small upfront payment followed by fixed monthly repayments. This predictability greatly assists with cash flow management, allowing you to budget effectively without large, unforeseen expenses impacting your business finances.

- No Depreciation Worries: When you lease, you're essentially renting the vehicle, meaning you don't bear the burden of depreciation. New vehicles can lose a significant portion of their value, sometimes up to 40% in the first year alone. With leasing, you simply hand the vehicle back at the end of the contract, avoiding this financial hit.

- Affordable Access to Environmentally Friendly Vehicles: As environmental regulations tighten and charges for high-emission vehicles in some UK cities increase (e.g., Clean Air Zones), leasing offers an affordable pathway to drive newer, more fuel-efficient, or electric vehicles. This can save you money on charges and align with a more sustainable business image.

- Included Benefits: Many leasing deals include benefits such as free breakdown recovery and Vehicle Excise Duty (VED), commonly known as vehicle tax. These inclusions simplify your vehicle management and reduce additional out-of-pocket expenses.

Disadvantages of Leasing a Vehicle

- No Asset Ownership: The most significant drawback is that the vehicle will never be your asset. You don't build equity, nor do you have a vehicle to sell at the end of the contract term, unlike with purchasing.

- Mileage Restrictions: Leasing agreements come with an agreed annual mileage limit (e.g., 36,000 miles over three years). Exceeding this limit will incur additional mileage payments at the end of the contract, which can be costly. It's vital to accurately estimate your business and personal mileage upfront.

- Early Termination Costs: Should your circumstances change and you need to end the lease contract before its term is up, the cost can be substantial. Furthermore, early termination isn't always permitted by the lessor.

- Ongoing Costs: While VED and breakdown recovery might be included, you are still responsible for routine maintenance, servicing, and, of course, your own vehicle insurance. These are essential costs to factor into your budget.

- Credit Check Requirements: When applying for a lease, a credit check will almost certainly be carried out. Approval is not guaranteed, and a strong credit history is usually required.

It's important to note: leasing may not be the best solution for everyone. Before making a decision, carefully weigh up the pros and cons and crunch the numbers to see if leasing or buying aligns better with your business model and financial situation.

How Does Vehicle Leasing Actually Work?

At its core, vehicle leasing can be thought of as a long-term rental contract or agreement. As the 'lessee,' you make an initial down payment, followed by a series of fixed monthly payments to the vehicle provider, known as the 'lessor.' Contract terms typically range from two years (24 months) to five years (60 months), with three-year contracts being a common choice due to their balance of flexibility and cost-effectiveness.

Key Vehicle Leasing Contract Options

Understanding the different types of leasing contracts is crucial, as they each offer varying degrees of flexibility and ownership potential at the end of the term:

- Personal Contract Hire (PCH): This is a straightforward long-term rental agreement. You make an initial payment, followed by fixed monthly payments for an agreed period. At the end of the contract, you simply hand the car back to the leasing company. There is no option to buy the vehicle, making it ideal if you always want to drive a new car and aren't interested in ownership.

- Personal Contract Purchase (PCP): While often marketed as a leasing option, PCP offers a path to ownership. You pay a deposit, followed by monthly payments, similar to PCH. However, at the end of the contract, you have three choices: you can hand the car back, use any accumulated equity towards a new PCP deal, or make a final 'balloon payment' to buy the car outright. Interestingly, only a small percentage (around 20%) of individuals choose to make this final payment.

- Business Contract Hire (BCH): This is essentially a version of Personal Contract Hire (PCH) specifically tailored for businesses, including sole traders, partnerships, and limited companies. BCH is a popular choice due to its potential tax efficiencies and the ability to reclaim VAT on lease payments (if VAT registered). Like PCH, the vehicle is returned at the end of the contract, and there is no option to buy.

Is Vehicle Leasing a Tax Deductible Expense in the UK?

For self-employed individuals, the good news is that leasing (or hiring) a car for business purposes is generally considered an allowable expense. This means you can deduct the cost of leasing from your taxable profits, thereby reducing your income tax and National Insurance contributions. However, there are crucial considerations, particularly concerning the vehicle's CO2 emissions, that can impact how much of the cost you can claim.

The Critical Role of CO2 Emissions

HMRC's rules on claiming hire charges for leased cars are directly tied to the vehicle's CO2 emissions. This is a vital point that many self-employed individuals overlook, potentially leading to incorrect claims. As HMRC guidance explains, in certain situations, you cannot claim the full hire charges or rental payments.

Specifically, if you leased a car:

- On or after 6 April 2020 and its CO2 emissions were more than 110g/km: You had to disallow 15% of the hire charge or rental cost. This means you could only claim 85% of the leasing expense.

However, the rules have since changed, becoming stricter:

- From 1 April 2021 (for businesses) or 6 April 2021 (for individuals, including sole traders, for tax purposes): You must disallow 15% of hire charges or rental costs if your vehicle's CO2 emissions are more than 50g/km. This significantly lower threshold means that a much wider range of conventionally fuelled vehicles now fall into the category where 15% of the leasing cost cannot be claimed.

For clarity, here's a summary of the CO2 emission thresholds for disallowance:

| Lease Start Date | CO2 Emissions Threshold | Disallowance Rate |

|---|---|---|

| Before 1 April 2021 | Over 110g/km | 15% of hire charge |

| From 1 April 2021 (or 6 April 2021 for individuals) | Over 50g/km | 15% of hire charge |

It is paramount that when speaking to vehicle lessors, you specifically inquire about the vehicle's CO2 emissions and the potential tax implications for your self-employed status. Neglecting this could lead to an incorrect tax calculation.

Furthermore, if you use a leased or hired vehicle for personal use, you cannot claim the proportion of the leasing cost attributable to personal journeys as an allowable expense. You must calculate and deduct this personal element from your overall claim. HMRC expects a reasonable and consistent method for apportioning business and personal use, often based on mileage records.

Reporting Vehicle Leasing Costs to HMRC

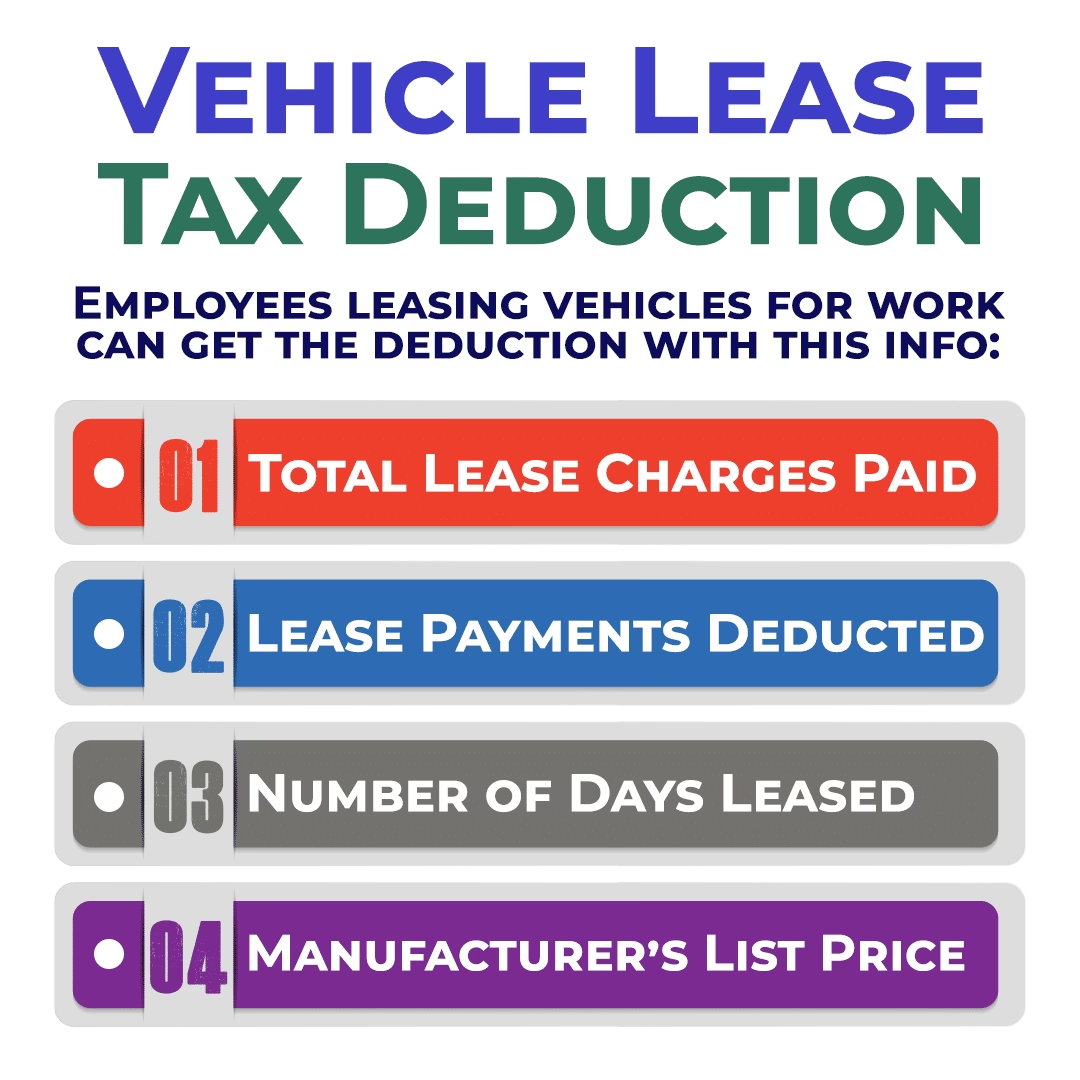

As a sole trader, self-employed contractor, or freelancer, you report your business income and expenses annually via your Self Assessment tax return. The specific form for this is the SA100, accompanied by supplementary pages relevant to your business (e.g., SA103S for self-employment). When completing your Self Assessment, you will declare your total business income and then list your allowable expenses.

Your vehicle leasing costs, after any necessary disallowances for CO2 emissions or personal use, will be entered as a business expense. These allowable expenses are then deducted from your gross earnings, along with other reliefs and allowances you are entitled to. The resulting figure is your taxable profit, on which you will pay Income Tax and any due National Insurance Contributions. Accurate record-keeping of your lease agreements, monthly payments, and mileage logs (if apportioning personal use) is essential to support your claims should HMRC ever query them.

Frequently Asked Questions (FAQs)

Q: What exactly is an 'allowable expense' for tax purposes?

A: An allowable expense is a cost that HMRC considers to have been incurred 'wholly and exclusively' for the purposes of your trade or business. These expenses can be deducted from your business income before calculating your taxable profit, thereby reducing your tax liability.

Q: Can I claim 100% of my vehicle leasing costs?

A: Not always. You generally cannot claim 100% if the vehicle's CO2 emissions exceed the current threshold (50g/km for leases from April 2021), in which case you must disallow 15% of the hire charge. Additionally, any portion of the vehicle's use that is for personal journeys must also be disallowed and cannot be claimed as a business expense.

Q: How do I calculate the personal use proportion of my leased vehicle?

A: To calculate the personal use proportion, you need to keep accurate records of your total mileage and the mileage specifically for business purposes. For example, if you drive 10,000 miles in a year, and 7,000 of those miles were for business, then 70% of your allowable leasing costs (after any CO2 disallowance) could be claimed. HMRC expects a reasonable and consistent method of apportionment.

Q: Where can I find the most up-to-date HMRC guidance on vehicle expenses?

A: For the latest and most detailed official guidance, you should always refer to the GOV.UK website. Search for 'HMRC expenses if you're self-employed' or 'car, van and travel expenses' to find the relevant sections.

Q: Is Business Contract Hire (BCH) always the best option for a sole trader from a tax perspective?

A: While Business Contract Hire (BCH) is often popular among sole traders due to its direct business-focused structure and potential VAT reclaim benefits (if VAT registered), it's not universally the 'best' option. The optimal choice depends on your specific business circumstances, whether you are VAT registered, your expected mileage, and your long-term vehicle needs. It's always wise to compare BCH with Personal Contract Hire (PCH) and even outright purchase options, considering all financial and tax implications for your unique situation.

In conclusion, vehicle leasing presents a compelling option for many self-employed individuals in the UK, offering access to modern vehicles with predictable costs and reduced depreciation worries. Crucially, it can also be a tax-efficient choice, as leasing costs are generally allowable expenses. However, the intricacies of HMRC rules, particularly regarding CO2 emissions and the need to accurately apportion business versus personal use, cannot be overstated. By understanding these key factors and maintaining meticulous records, you can confidently navigate the world of vehicle leasing, potentially reducing your tax bill and ensuring your business remains mobile and financially sound.

If you want to read more articles similar to Leasing a Car: UK Tax Deductible for Self-Employed?, you can visit the Taxis category.