31/07/2019

- The Glittering Heights and Crashing Depths of NYC Taxi Medallions

- The Arrival of Disruption: Ride-Sharing Services

- Regulatory Scrutiny and the Credit Union Crisis

- The Boro Taxi Program: A Double-Edged Sword

- The Unravelling: Credit Union Failures

- Government and Industry Response

- The Current State and Future Outlook

- Frequently Asked Questions

The Glittering Heights and Crashing Depths of NYC Taxi Medallions

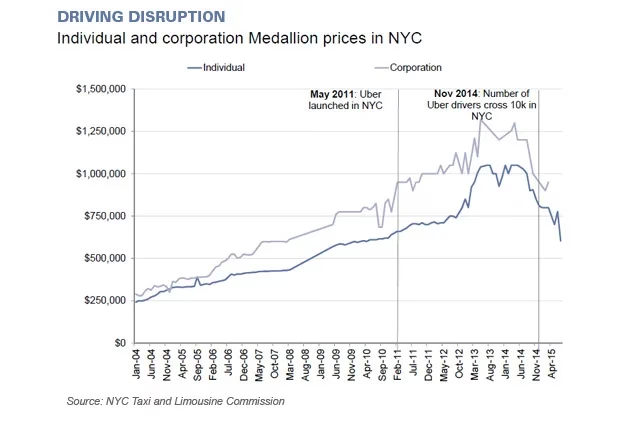

For decades, the New York City taxi medallion was more than just a permit to operate a yellow cab; it was a coveted, high-value asset, a symbol of a lucrative business. Many saw it as a secure investment, a ticket to a comfortable retirement. However, the period between 2006 and 2014 marked the zenith of the medallion's value, with prices soaring to staggering heights, exceeding $1.2 million at their peak. This era of prosperity was fueled by a combination of factors, including the limited supply of medallions, which created an artificial scarcity, and a market ripe for speculation. Investors and drivers alike poured money into acquiring these permits, often financed by loans, believing the value would only continue to climb.

This period of perceived stability and growth, however, masked underlying vulnerabilities. The influx of new technologies and business models began to disrupt the traditional taxi industry, setting the stage for a dramatic shift that would challenge the very foundation of the medallion's worth.

The Arrival of Disruption: Ride-Sharing Services

The landscape of urban transportation began to change irrevocably in May 2011 with the arrival of the first ride-sharing service in New York City. This marked the beginning of a profound disruption. These new platforms offered a seemingly more convenient and often cheaper alternative to traditional taxis, utilising smartphones for booking and payments, and employing a vast network of drivers using their personal vehicles. As more ride-sharing services entered the market by July 2014, the competitive pressure on the traditional taxi industry intensified significantly.

This competition directly impacted the demand for taxi medallions. As ridership shifted towards these new services, the income potential for medallion owners and drivers began to dwindle. Consequently, the market value of medallions, once thought to be an unsinkable asset, started to show signs of strain. The speculative bubble, inflated by years of steady growth and limited supply, was showing its first cracks.

Regulatory Scrutiny and the Credit Union Crisis

The changing dynamics of the taxi market did not go unnoticed by regulatory bodies. As early as October 2012, the National Credit Union Administration (NCUA) began discussions with other regulators to assess the evolving conditions and their potential impact on financial institutions that had heavily supported the taxi industry, particularly through medallion-secured lending. Many credit unions, especially those with a strong presence in New York, had significant portfolios of loans backed by taxi medallions as collateral.

The NCUA issued several letters to credit unions throughout this period, providing updated supervisory information and guidance on taxi-medallion secured lending. Letter to Credit Unions, 14-CU-06, in April 2014, and further clarifications in 15-CU-03 in May 2015, highlighted the growing concerns. These communications underscored the need for prudent risk management as the value of the collateral began to decline.

The Boro Taxi Program: A Double-Edged Sword

In an effort to revitalize the traditional taxi industry and expand service, the Boro Taxi Program was launched in June 2013. This initiative permitted street hails for green medallion holders in the outer boroughs of the Bronx, Brooklyn, Queens, Staten Island, and Northern Manhattan. While intended to increase business for yellow cab drivers, it also introduced a new layer of complexity and competition within the existing system, potentially impacting the perceived exclusivity and value of the traditional medallions.

The Unravelling: Credit Union Failures

The financial repercussions of the declining medallion values soon became starkly apparent. Several credit unions that had heavily invested in taxi-medallion loans began to face severe difficulties. The timeline of events paints a grim picture:

- September 2015: Montauk Credit Union was conserved by the State of New York’s Department of Financial Services.

- April 2016: Montauk Credit Union was merged into Bethpage Federal Credit Union.

- February 2017: The New York Department of Financial Services placed Melrose Credit Union into receivership, with the NCUA appointed as conservator.

- June 2017: The NCUA Board approved the conservatorship of LOMTO Federal Credit Union.

- February 2018: First Jersey Credit Union was liquidated by the New Jersey State Department of Banking and Insurance, with US Alliance Federal Credit Union assuming most of its assets.

- August 2018: The NCUA liquidated Melrose Credit Union, and Teachers Federal Credit Union assumed its members and assets. The NCUA also filed charges against Melrose's former CEO.

- September 2018: The NCUA liquidated LOMTO Federal Credit Union, with Teachers Federal Credit Union again assuming members and assets.

- November 2018: The NCUA disclosed that the failures of several credit unions, including St. Elizabeth’s, First Jersey, Louisville Metro Police Officers, Greater Christ Baptist Church, Melrose, and LOMTO, resulted in a staggering $744.9 million loss to the National Credit Union Share Insurance Fund.

- January 2019: Progressive Credit Union merged into PenFed.

These failures were a direct consequence of the plummeting value of taxi medallions, which served as collateral for a significant portion of their loan portfolios. As medallion values fell below the outstanding loan amounts, these credit unions experienced substantial losses, leading to their eventual collapse.

Government and Industry Response

In the face of this crisis, regulatory bodies and industry leaders worked to mitigate the damage and provide relief. NCUA Chairman Rodney E. Hood published an op-ed in the New York Daily News in July 2019, outlining the agency’s actions to assist borrowers affected by the credit union failures. Further actions included prohibiting the former CEO of Melrose Credit Union from participating in federally insured financial institutions and initiating a bidding process for the NCUA’s taxi-medallion loan holdings in September 2019. Chairman Hood also addressed questions about relief efforts before the House Financial Services Committee in December 2019.

The Current State and Future Outlook

The era of the taxi medallion as a million-dollar asset is firmly in the past. The collapse of the market has had devastating financial consequences for many who invested heavily in them, often relying on them for their livelihood and retirement. The rise of ride-sharing, coupled with regulatory challenges and the resulting credit union failures, has fundamentally reshaped the New York City taxi industry.

While the future of traditional yellow cabs remains uncertain, efforts are ongoing to find sustainable models. The focus has shifted from the high-value medallion to adapting to a new competitive landscape. For those who still hold medallions, the challenge is immense, and the path forward requires navigating a vastly different economic reality.

Frequently Asked Questions

Q1: What was the peak price of a New York City taxi medallion?

A1: At the market's peak, a single New York City taxi medallion could exceed $1.2 million.

Q2: What caused the drastic fall in taxi medallion values?

A2: The primary causes include the introduction and widespread adoption of ride-sharing services, increased competition, and a speculative market that eventually corrected.

Q3: How did ride-sharing services impact the taxi industry?

A3: Ride-sharing services provided a convenient and often cheaper alternative, diverting customers from traditional taxis and reducing the income potential for medallion owners and drivers.

Q4: Which financial institutions were most affected by the medallion collapse?

A4: Several credit unions that had significant portfolios of loans secured by taxi medallions experienced severe financial distress and failures, including Montauk Credit Union, Melrose Credit Union, LOMTO Federal Credit Union, and First Jersey Credit Union.

Q5: What has the NCUA done in response to the crisis?

A5: The NCUA has provided guidance on lending, managed the conservatorship and liquidation of affected credit unions, assisted borrowers, and initiated the sale of its taxi-medallion loan holdings.

If you want to read more articles similar to NYC Taxi Medallion: The Boom, The Bust, and The Future, you can visit the Transport category.