07/01/2026

Navigating the intricacies of payslips and P60 forms can often feel like deciphering a foreign language, especially when grappling with the nuances of pension contributions. Many individuals find themselves puzzled by discrepancies between what they expect their tax to be and the figures presented on their P60, particularly when pension schemes are involved. This is a common concern for those preparing their Self Assessment tax returns, as accurate reporting of income is paramount. This article aims to demystify the relationship between your P60, your pension contributions, and how these elements impact your overall tax liability, specifically addressing the query: “Will my P60 show a lower figure if I don't pay contributions?” The answer, as we'll explore, is not a simple yes or no, but rather a nuanced understanding of how different pension schemes and deduction methods can influence the figures you see.

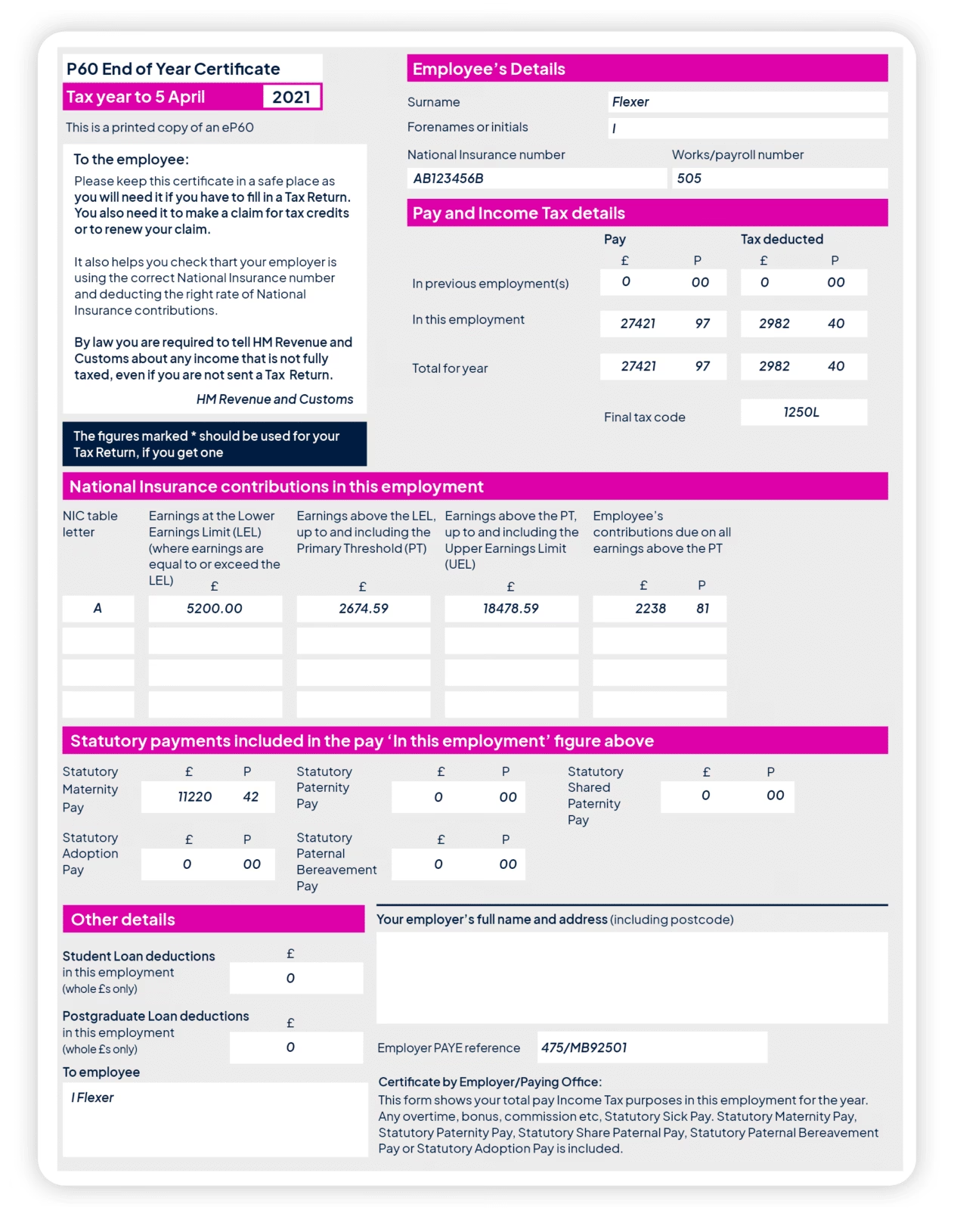

- Understanding Your P60: The Annual Summary

- How Pension Contributions Affect Your P60

- Employer Pension Schemes: NEST and TPT/Benpal

- Why the Difference in P60 Presentation?

- What if My P60 Doesn't Show My Full Gross Pay?

- Will Not Paying Contributions Lower My P60 Figure?

- Self Assessment and Pension Contributions: A Summary Table

- Common Pitfalls and How to Avoid Them

- Frequently Asked Questions

Understanding Your P60: The Annual Summary

Your P60, officially known as a 'Certificate of Earnings', is an annual summary of your pay and the tax deducted from it by your employer. It’s a crucial document for your Self Assessment. It details your total earnings, the tax paid, National Insurance contributions, and other deductions. The figures on your P60 are based on the information your employer has submitted to HMRC throughout the tax year (6 April to 5 April). It’s essential to ensure that the information on your P60 accurately reflects your earnings and tax paid.

How Pension Contributions Affect Your P60

Pension contributions are typically deducted from your gross pay before tax is calculated. This is known as 'tax relief at source' for many pension schemes. This means that the amount of tax you pay is reduced because your taxable income is lower. However, the way these contributions are displayed on your P60 can vary depending on the type of pension scheme and how your employer processes the deductions.

Gross Pay vs. Taxable Pay

The core of the confusion often lies in the distinction between 'gross pay' and 'taxable pay'.

- Gross Pay: This is your total earnings before any deductions, including pension contributions, National Insurance, or other voluntary deductions.

- Taxable Pay: This is the amount of your income that is subject to income tax. When you contribute to a pension scheme that benefits from tax relief at source, your taxable pay is usually your gross pay minus your pension contributions.

The scenario described, where one payslip shows 'Total gross pay' and 'Gross for tax' as the same, and the other’s 'Taxable pay to date' and P60 reflect amounts after deductions, highlights these differing reporting methods.

Employer Pension Schemes: NEST and TPT/Benpal

The specific pension arrangements you and your wife have with NEST and TPT/Benpal are relevant to understanding the P60 figures.

NEST (National Employment Savings Trust): In your case with NEST, your employer deducts 80% of your contribution, and NEST claims the remaining 20%. This is a common feature of relief at source schemes. Your contribution is effectively topped up by the government. The amount deducted from your salary is your net contribution, but for tax purposes, the gross contribution (your contribution plus the government's top-up) is what matters. Your P60 should ideally reflect your earnings before these deductions, with the pension contributions being a separate item or reflected in a way that shows the taxable income correctly.

TPT/Benpal: With your wife's scheme, the full amount is deducted by her employer. This is also a standard deduction. The key difference in reporting might stem from how the employer’s payroll system accounts for these deductions when generating the P60.

Why the Difference in P60 Presentation?

The fundamental reason for the difference in how your P60 and payslips are presented, even with similar pension arrangements, often comes down to the specific payroll software used by each employer and their chosen method of reporting to HMRC. Some systems might automatically adjust the 'gross for tax' figure to exclude pension contributions, while others might show the full gross pay and then detail pension deductions separately or implicitly through the lower tax deducted.

A P60 that shows 'Pay and income tax details: in this employment' as the amount after pension contributions have been deducted is likely reflecting your taxable income for that employment. This is the figure that HMRC uses to calculate your tax liability. The question then arises: does this mean the P60 is giving the wrong amount for Self Assessment under 'Pay from this employment - the total from your P45 or P60 - before tax was taken off'?

The wording on the Self Assessment form is critical here. It asks for your pay before tax was taken off. This typically refers to your gross earnings from that employment. If your P60 shows your taxable pay after pension deductions as the primary figure in the 'Pay and income tax details' box, you need to be careful.

The Importance of Gross Earnings

For Self Assessment purposes, when reporting employment income, you should generally use your gross earnings before any deductions, including pension contributions. This is because pension contributions made through 'relief at source' are a form of tax relief, and the tax system accounts for this relief separately. Your P60 should, in principle, provide you with the necessary information to determine your correct gross pay.

If your P60 explicitly states a figure as 'Total Gross Pay' or similar, that is the figure you should use for the 'Pay from this employment' section of your Self Assessment tax return. If the P60 only provides a 'taxable pay' figure that is lower than your actual gross pay due to pension deductions, you may need to refer to your payslips to ascertain your full gross earnings.

What if My P60 Doesn't Show My Full Gross Pay?

This is where meticulous record-keeping becomes vital. If your P60 doesn't clearly delineate your total gross pay before pension deductions, you should:

- Consult Your Payslips: Your payslips are designed to show your earnings breakdown. Look for a 'Total Gross Pay' or similar figure before any deductions are listed.

- Check Your P45: If you changed jobs during the tax year, your P45 from your previous employment will also show your gross pay and tax deducted for that period.

- Review Pension Statements: While not directly showing gross pay, your pension provider statements might offer insights into your contribution amounts.

- Contact Your Employer's Payroll Department: If you are still unsure, the most reliable course of action is to speak directly with your employer's payroll or HR department. They can clarify how your earnings are reported on your P60 and provide you with the correct gross pay figure.

Will Not Paying Contributions Lower My P60 Figure?

Let's directly address the initial question: "Will my P60 show a lower figure if I don't pay contributions?"

If you don't pay pension contributions, your gross pay will remain the same, and your taxable pay will also be higher (equal to your gross pay, assuming no other deductions). This means that your P60 would likely show a higher figure for 'Taxable Pay' or 'Gross for Tax' compared to if you *were* paying contributions. However, the 'Total Gross Pay' figure should, in theory, be the same regardless of whether you contribute to a pension or not, as it represents your earnings before any deductions. The impact of not paying contributions is primarily on the amount of tax you pay, not necessarily on the gross pay figure itself, although reporting variations can create confusion.

The confusion arises because pension contributions reduce your taxable income, which in turn reduces the tax deducted from your pay. Therefore, if your P60 explicitly shows your taxable income and this is lower due to pension contributions, then *not* paying contributions would result in a higher taxable income figure on your P60. But the fundamental gross pay figure should remain consistent.

Self Assessment and Pension Contributions: A Summary Table

To clarify the impact on your Self Assessment, consider this:

| Scenario | Impact on 'Total Gross Pay' on P60 | Impact on 'Taxable Pay' on P60 | Impact on Tax Liability (if reported correctly) |

|---|---|---|---|

| Paying Pension Contributions (Relief at Source) | (Your total earnings before deductions) | Lower (Gross Pay - Pension Contributions) | Lower (due to tax relief on contributions) |

| Not Paying Pension Contributions | (Your total earnings before deductions) | Higher (Equal to Gross Pay) | Higher (no tax relief) |

When completing your Self Assessment, you should declare your total gross earnings from employment. If you are a member of a relief-at-source pension scheme, you will typically declare this gross income and then claim the tax relief on your contributions through your Self Assessment. However, many people find that the tax deducted at source on their salary already reflects this relief. The P60 figure for 'Pay and income tax details' should ideally reflect the correct taxable income after statutory deductions. If your P60 shows your gross pay and then separately details pension contributions, you would use the gross pay figure for your Self Assessment.

Common Pitfalls and How to Avoid Them

1. Using Taxable Pay instead of Gross Pay: This is the most common error. Always ensure you are reporting your full gross earnings from employment as shown on your P60 or payslips.

2. Misinterpreting Pension Deductions: Understand whether the figure on your P60 is before or after pension deductions. If it's after, you need to find the pre-deduction gross figure.

3. Forgetting Other Income: Ensure your Self Assessment includes all sources of income, not just employment income.

Frequently Asked Questions

Q1: Does my P60 show my pay before or after pension deductions?

A1: This can vary. Some P60s will clearly state 'Gross Pay' before deductions, while others might show 'Taxable Pay' which is after pension deductions. Always check the specific wording on your P60 and refer to your payslips for clarity.

Q2: If I don't pay pension contributions, will my P60 be higher?

A2: The 'Total Gross Pay' figure should ideally remain the same. However, your 'Taxable Pay' or 'Gross for Tax' figure would be higher, as it wouldn't be reduced by pension contributions. This means more tax would have been deducted from your salary throughout the year.

Q3: Should I use the 'Gross for Tax' figure from my P60 for Self Assessment?

A3: Generally, you should use your total gross earnings from employment. If 'Gross for Tax' accurately reflects this, then yes. However, if 'Gross for Tax' is already reduced by pension contributions, you need to find your full gross pay figure.

Q4: My wife's P60 shows a lower figure than mine, but she earns more. Is this because of her pension?

A4: It's possible. If her P60 shows her taxable pay after significant pension contributions, it would indeed be lower than her gross pay. If your P60 shows your gross pay, a direct comparison might be misleading without understanding the deductions applied.

Q5: How do I claim tax relief on my pension contributions if my P60 isn't clear?

A5: If you are in a 'relief at source' scheme, the tax relief is usually applied automatically. If you need to claim additional relief (e.g., if you're a higher or additional rate taxpayer and your employer only deducts basic rate tax), you would do so on your Self Assessment tax return. Consult HMRC guidance or a tax professional for specific advice.

In conclusion, while your P60 is a vital document, understanding how it's presented, especially concerning pension contributions, is key to accurate Self Assessment. Always aim to report your total gross earnings from employment. If in doubt, don't hesitate to seek clarification from your employer or a qualified tax advisor to ensure you are correctly reporting your income and benefiting from all the tax reliefs you are entitled to.

If you want to read more articles similar to P60 and Pension Contributions: A Closer Look, you can visit the Taxis category.