27/01/2016

Becoming a licensed taxi driver in the United Kingdom offers a rewarding career path, providing flexibility, independence, and the opportunity to be your own boss. However, the initial hurdle for many aspiring drivers is the significant cost associated with acquiring a taxi licence. Unlike a standard car loan, financing a taxi licence involves specific considerations due to the nature of the asset and the regulatory environment of the taxi industry. This comprehensive guide will walk you through everything you need to know about securing a loan for your taxi licence, from understanding the financial landscape to meeting lender requirements.

The price of a taxi licence can vary dramatically across different regions of the UK, influenced by local demand, regulations, and market dynamics. Historically, these licences have been valuable assets, sometimes experiencing periods of significant price increases. More recently, factors such as the rise of ride-sharing apps (Private Hire Vehicles or PHVs, often referred to as VTCs in other countries) and economic shifts have introduced volatility into the market. Despite these changes, there remains a steady demand for taxi services, making a taxi licence a viable and often profitable investment. However, securing the necessary funding has become more stringent, making expert guidance more crucial than ever.

- Understanding the Cost of a UK Taxi Licence

- Financing Options: Two Main Approaches

- Comparative Overview of Loan Options

- Essential Requirements for Your Loan Application

- The Role of Financial Intermediaries

- Frequently Asked Questions (FAQs)

- What exactly is a taxi licence loan?

- Why are taxi licences so expensive in the UK?

- Can I get a taxi licence loan without a large deposit?

- What if I don't have a fixed job history?

- What collateral is required for a taxi licence loan?

- How long does it take to get a taxi licence loan approved?

- Do I need prior experience as a taxi driver to get a loan?

- What if my credit history isn't perfect?

- Conclusion

Understanding the Cost of a UK Taxi Licence

The cost of a taxi licence is a primary concern for anyone entering the industry. While exact figures fluctuate, a licence can typically range from tens of thousands to well over £100,000, depending on the local authority and market conditions. For example, a licence in a high-demand urban area might command a price upwards of £150,000. This substantial investment necessitates external financing for most individuals.

When considering a loan, lenders primarily focus on two fundamental aspects: your ability to generate sufficient income from your taxi business to repay the loan, and the security you can offer against the borrowed amount. The good news is that the taxi industry has a well-established earning potential, and importantly, the taxi licence itself often serves as a primary form of collateral for the loan. This makes it a more attractive proposition for lenders compared to unsecured personal loans.

Another critical factor is your personal contribution, often referred to as a deposit or down payment. While it might be tempting to seek 100% financing, lenders nearly always require a significant upfront investment from the applicant. This demonstrates your commitment to the venture and reduces the lender's risk. Currently, a minimum personal contribution of around £30,000 is often expected, though this can vary based on the total cost of the licence and your financial profile.

Financing Options: Two Main Approaches

When seeking a loan for a taxi licence, you'll generally find two primary financing structures offered by lenders, each with distinct advantages and requirements:

- Financing 70% of the Licence Value: This is a common approach where you contribute a larger upfront deposit.

- Financing up to 90% of the Licence Value: This option requires a smaller personal contribution but typically involves additional costs or requirements, such as a guarantor.

Option 1: The 70% Loan – Higher Upfront, Lower Costs

This financing model is ideal if you have a substantial amount of capital saved for your deposit. Lenders may offer to finance up to 70% of the taxi licence's purchase price, often with a maximum loan amount of around £100,000. These loans typically come with a fixed interest rate, for example, 4.25%, over a repayment period of up to 12 years (144 months).

Under this scenario, you would be responsible for providing the remaining 30% of the licence cost, plus any associated loan expenses. Let's look at an example:

- Licence Purchase Price: £150,000

- Loan Amount (70%): £105,000 (Note: If the loan amount exceeds the typical maximum of £100,000, the loan will be capped, and your contribution will increase.)

- Your Required Contribution (30%): £45,000

- Additional Loan Expenses: Approximately £7,000

- Total Upfront Capital Needed: £45,000 (deposit) + £7,000 (expenses) = £52,000

This option generally results in lower overall borrowing costs due to the smaller loan amount and potentially more favourable terms, but it demands a significant initial investment from you.

Option 2: The 90% Loan – Less Upfront, More Expensive

For aspiring taxi drivers who have less capital available for a deposit, the 90% financing option can be a game-changer. This structure allows you to borrow a larger proportion of the licence's value, often up to a maximum of £125,000. The key difference here is that to mitigate the increased risk for the lender, this option often involves a guarantor or a specialist financial arrangement that provides additional security.

A guarantor is an individual who agrees to repay the loan if you are unable to. This provides the bank with an extra layer of security. While you contribute less upfront, the overall costs associated with the loan, including fees for the guarantor arrangement or specialist finance, can be significantly higher. These additional costs might double, potentially reaching around £13,000.

Using the same example as above:

- Licence Purchase Price: £150,000

- Loan Amount (90%): £135,000 (Note: This might be capped at £125,000, meaning your contribution would adjust accordingly.)

- Your Required Contribution (10%): £15,000

- Additional Loan Expenses (higher due to guarantor/specialist finance): Approximately £13,000

- Total Upfront Capital Needed: £15,000 (deposit) + £13,000 (expenses) = £28,000

This option significantly reduces your initial cash outlay, making the dream of owning a taxi licence more accessible, but it comes with higher total costs over the life of the loan and the requirement of a suitable guarantor.

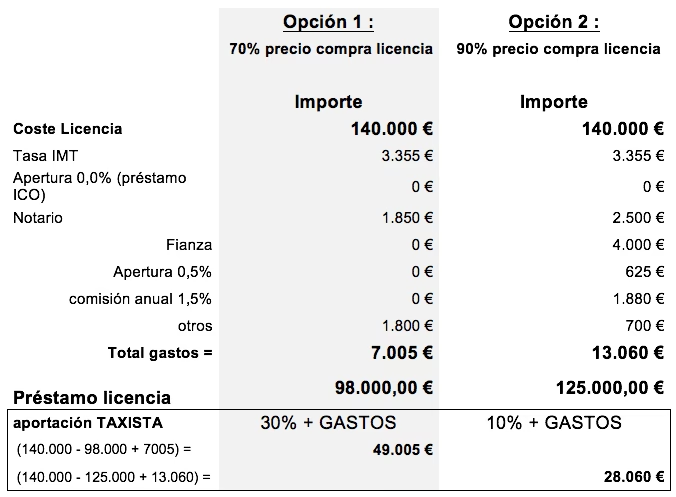

Comparative Overview of Loan Options

Let's compare these two common scenarios for a hypothetical taxi licence purchase of £140,000 (excluding expenses, for simplicity of comparison):

| Feature | 70% Financing Option | 90% Financing Option |

|---|---|---|

| Licence Cost (Example) | £140,000 | £140,000 |

| Maximum Loan Amount | £98,000 (capped at £100,000) | £125,000 |

| Your Required Deposit | £42,000 | £15,000 |

| Typical Loan Term | Up to 12 years (144 months) | Up to 12 years (144 months) |

| Interest Rate (Fixed) | Approx. 4.25% | Varies, potentially higher |

| Approx. Additional Loan Costs | £7,000 | £13,000 |

| Total Upfront Cash Needed | £42,000 (deposit) + £7,000 (costs) = £49,000 | £15,000 (deposit) + £13,000 (costs) = £28,000 |

| Key Requirement | Higher personal deposit | Lower personal deposit, usually requires a guarantor |

This table highlights the trade-off between upfront capital and overall loan costs. Your choice will depend on your personal financial situation and access to a suitable guarantor.

Essential Requirements for Your Loan Application

Regardless of the financing option you choose, lenders will require a comprehensive set of documents and meet specific criteria to assess your eligibility and creditworthiness. While these can vary slightly between lenders, here are the typical requirements:

Applicant Requirements:

- Experience in the Taxi Sector: Many lenders prefer applicants to have a minimum of 1.5 years of experience in the taxi or private hire industry. This demonstrates your understanding of the business and your ability to generate income.

- Financial Stability: Lenders look for stability in your work history and financial affairs.

- UK Residency: Applicants must be UK citizens or hold a long-term residency permit.

Guarantor Requirements (if applicable for 90% loan):

If you opt for a loan requiring a guarantor, that individual will also need to meet stringent criteria:

- Stable, Recurring Income: The guarantor must have a minimum recurring monthly income, often around £1,250, from a source outside the taxi sector.

- Indefinite Employment Contract: They should ideally be a salaried employee with an indefinite contract, having been with their current employer for at least two years.

- Financial Stability: Similar to the applicant, the guarantor's financial history and employment stability will be thoroughly assessed.

- Not in the Taxi Sector: Typically, the guarantor cannot be involved in the taxi industry themselves.

Required Documentation for Both Applicant and Guarantor:

Preparing these documents in advance will significantly streamline your application process:

- Proof of Identity: Valid UK Passport or Driving Licence.

- Proof of Address: Utility bills or bank statements from the last three months.

- Financial Statements:

- Your latest Self Assessment Tax Return (SA302).

- Your last three months' payslips (if employed).

- Your full employment history (e.g., National Insurance Contributions record).

- Statements for the last three months from all bank accounts.

- Proof of savings (e.g., bank statements showing your minimum £30,000 contribution).

- Existing Loan/Mortgage Information:

- Your last three months' statements or receipts for any existing mortgages or loans.

- Deeds for any properties you own (residential or commercial).

- Your current tenancy agreement, if you rent your home.

- Taxi-Specific Documentation:

- Proof of your taxi driving experience.

- Accreditation or provisional licence from your local authority (e.g., a PCO licence in London).

- Any 'contract of arras' (pre-agreement/deposit contract) if you have already put a deposit down on a specific licence.

It might seem like a lot of paperwork, especially if you're transitioning into taxi driving and don't have a traditional employment history. This is precisely where professional assistance becomes invaluable.

The Role of Financial Intermediaries

Navigating the complex world of commercial finance and securing a loan for a taxi licence can be daunting, particularly if you approach banks directly. Traditional banks often have rigid criteria that can be difficult for aspiring taxi drivers to meet, especially if you're leaving a fixed job to pursue this career.

This is where specialist financial intermediaries, like ourselves, come into play. We act as a bridge between you and the lenders, simplifying the entire process. Here's how we can help:

- Expert Guidance: We understand the specific nuances of taxi finance and know which lenders are most likely to approve your application.

- Streamlined Applications: We help you gather and present all necessary documentation in the correct format, saving you time and reducing the chances of delays.

- Addressing Unique Circumstances: If you don't have a conventional employment history, or if your income is variable, we can help build a strong case for your loan, highlighting the stable earning potential of a taxi business.

- Access to Specialist Lenders: We work with a network of banks and specialist finance providers who are familiar with the taxi sector and more flexible in their lending criteria for this specific asset.

- Free Case Study: Many intermediaries offer a free initial assessment of your financial situation and eligibility, providing clear advice without obligation.

By leveraging our expertise, you can significantly increase your chances of securing the necessary funding, even if your circumstances don't perfectly align with standard bank requirements. We aim to make the process as smooth and stress-free as possible, allowing you to focus on getting your taxi business off the ground.

Frequently Asked Questions (FAQs)

What exactly is a taxi licence loan?

A taxi licence loan is a specific type of commercial finance designed to help individuals purchase a taxi operating licence from a local authority or an existing licence holder. It's distinct from a car loan as it finances the right to operate, rather than just the vehicle itself.

Why are taxi licences so expensive in the UK?

The high cost is primarily due to their scarcity and the regulated nature of the industry. Local authorities often limit the number of licences issued, creating a high demand that drives up prices. The licence represents a valuable asset and a right to earn a living in a regulated market.

Can I get a taxi licence loan without a large deposit?

Yes, it's possible to get a loan with a lower deposit (e.g., 10% of the licence value), but this often requires a guarantor to provide additional security to the lender. This option typically incurs higher overall costs.

What if I don't have a fixed job history?

While traditional banks might find this challenging, specialist lenders and intermediaries understand that many aspiring taxi drivers are transitioning careers. They will focus on the projected income from your taxi business and may require a guarantor or a more detailed business plan to assess your repayment capability.

What collateral is required for a taxi licence loan?

The taxi licence itself is typically used as the primary collateral for the loan. In some cases, especially for higher loan-to-value options, a personal guarantor or other assets may be required as additional security.

How long does it take to get a taxi licence loan approved?

The approval time can vary. If all your documentation is in order and you meet the criteria, it could be a few weeks. However, if there are complexities or missing documents, it could take longer. Working with an intermediary can significantly speed up the process.

Do I need prior experience as a taxi driver to get a loan?

Many lenders prefer applicants to have some experience (e.g., 1.5 years) in the taxi or private hire sector. This demonstrates an understanding of the industry's earning potential and challenges. If you lack direct experience, you might need a stronger financial profile or a robust business plan.

What if my credit history isn't perfect?

A less-than-perfect credit history can make it more challenging but isn't necessarily a deal-breaker. Specialist lenders may be more flexible than high street banks, especially if you can provide a strong guarantor or a larger deposit. It's best to discuss your specific situation with a financial intermediary.

Conclusion

Acquiring a taxi licence is a significant investment and a pivotal step towards a fulfilling career. While the financial barrier can seem daunting, various loan options and professional support are available to help you navigate the process. Understanding the different financing models, preparing the necessary documentation, and meeting the specific requirements are crucial for a successful application.

Remember, the taxi sector, despite evolving challenges from ride-sharing platforms, remains a robust and regulated industry with consistent demand. By partnering with experienced financial professionals, you can confidently secure the funding needed to purchase your taxi licence and embark on your journey as a respected driver in the UK. Don't let the initial cost deter your ambition – expert assistance is just a call away.

If you want to read more articles similar to Securing a Taxi Licence Loan in the UK, you can visit the Taxis category.