03/01/2018

As a self-employed individual in the United Kingdom, navigating the complexities of tax and expenses can feel like a full-time job in itself. Among the various deductions you can claim, mileage expenses often represent a significant opportunity to reduce your taxable income. Understanding how HM Revenue & Customs (HMRC) approaches mileage claims is not just about compliance; it's about ensuring you're not leaving legitimate tax relief unclaimed. This comprehensive guide will walk you through everything you need to know about claiming mileage for your business, from what qualifies to the different methods available and the crucial record-keeping practices that will keep you on the right side of HMRC.

- Understanding Mileage Claims for the Self-Employed

- HMRC Mileage Rates: The Foundation of Your Claim

- Choosing Your Method: Simplified Expenses vs. Actual Costs

- Making Your Claim: Mileage Allowance Relief (MAR)

- Meticulous Record-Keeping: Your Essential Guide

- Comparison: Simplified Expenses vs. Actual Vehicle Costs

- Frequently Asked Questions (FAQs)

- Q: Can I claim mileage for commuting from my home to my regular business premises?

- Q: Are parking fines or speeding tickets covered by mileage claims?

- Q: What if my actual vehicle expenses are significantly higher than the HMRC mileage rates?

- Q: Do I need to keep every fuel receipt if I use the Simplified Expenses method?

- Q: How long should I keep my mileage records and receipts?

- Q: Can I switch between the Simplified Expenses and Actual Costs methods?

Understanding Mileage Claims for the Self-Employed

A mileage claim essentially allows you to be reimbursed for the costs incurred when using your personal vehicle for business purposes. For the self-employed, this means claiming a deduction against your profits for the wear and tear, fuel, and other associated costs of your vehicle's business use. Unlike employees who might receive tax-free Mileage Allowance Payments (MAPs) from an employer, self-employed individuals directly claim these expenses to reduce their taxable profit.

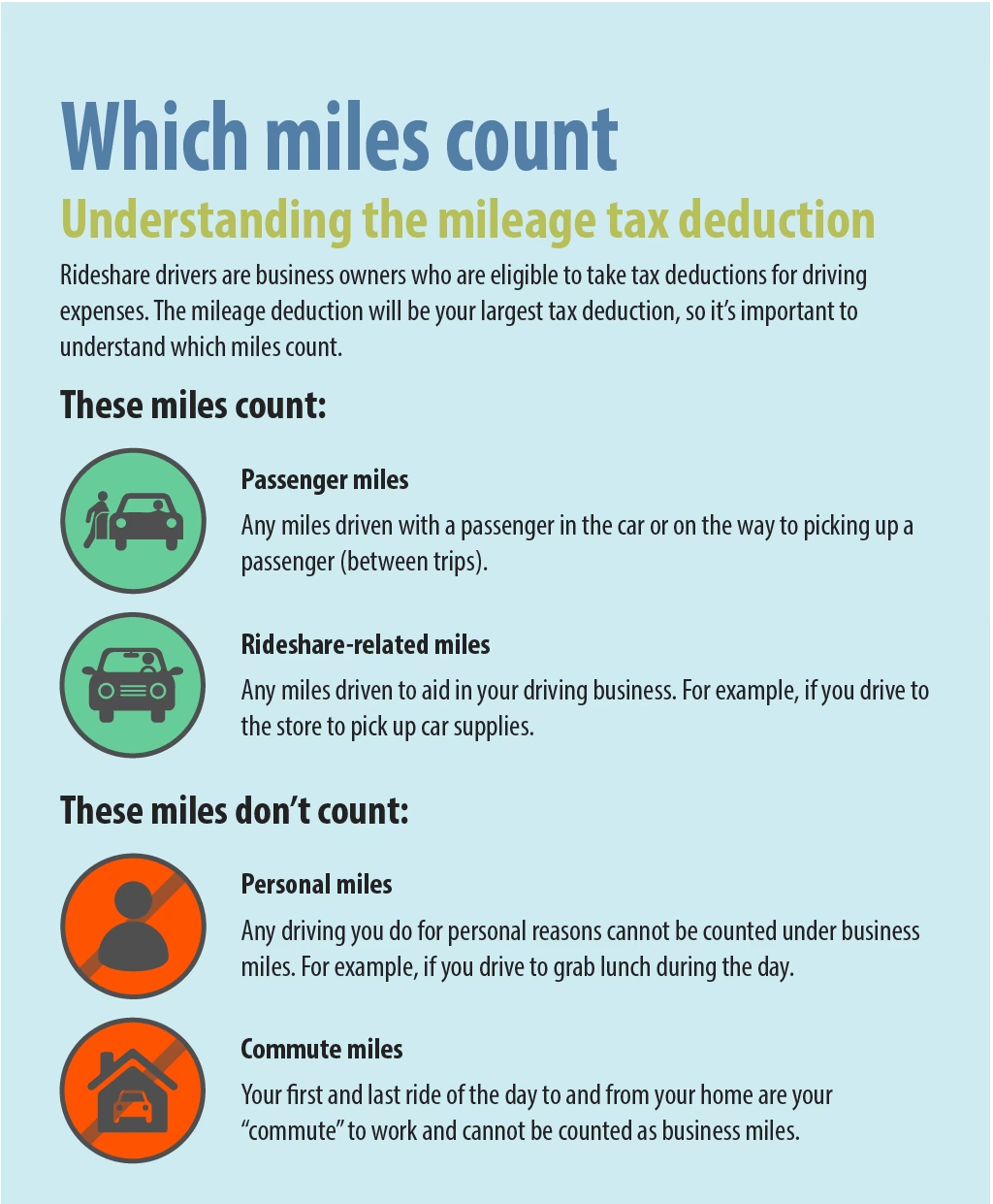

What Qualifies as Business Mileage?

It's straightforward: if your journey was undertaken purely for business, it generally qualifies. HMRC defines business travel as:

- Travel between your permanent workplace and a temporary work location (e.g., visiting clients, suppliers, or a temporary project site).

- Travel between different temporary workplaces.

- Travel between two workplaces if you have more than one in the same employment (less common for traditional self-employment, but relevant if you operate from multiple fixed business locations).

- Travel from your home to another workplace if your home is considered your permanent workplace due to the nature of your job (e.g., a home-based consultant travelling to a client's office).

Crucially, travel from your home to a regular, fixed place of work (your usual business premises, if not your home) is generally considered 'commuting' and does not qualify as business mileage. Similarly, any trips that are purely personal and have no business purpose cannot be claimed.

Eligible Vehicles for HMRC Mileage Claims

HMRC's rules are inclusive when it comes to the types of vehicles you can claim mileage for. This includes:

- Cars

- Vans

- Motorcycles

- Bicycles

Each vehicle type has its own specific HMRC mileage rates, which we will detail shortly.

HMRC Mileage Rates: The Foundation of Your Claim

The HMRC mileage rates are standard allowances that you can claim for each business mile driven. These rates are designed to cover the general running costs of your vehicle, including fuel, servicing, maintenance, depreciation, insurance, and road tax. It's important to note that these advisory rates have remained consistent since 2011, providing a stable framework for your claims.

Current HMRC Mileage Rates (2024/2025 Tax Year)

The rates are calculated per business mile:

| Vehicle Type | Rate for First 10,000 Business Miles | Rate for Miles Over 10,000 |

|---|---|---|

| Cars and Vans | 45p per mile | 25p per mile |

| Motorcycles | 24p per mile | 24p per mile |

| Bicycles | 20p per mile | 20p per mile |

What the Mileage Rates Cover (and Don't Cover)

The HMRC mileage rates are designed to be an all-encompassing figure for your vehicle's running costs. This means they cover:

- Fuel expenses

- Routine servicing and repairs

- General maintenance (e.g., tyres, oil changes)

- Depreciation (the reduction in your vehicle's value over time)

- Vehicle insurance and road tax (Vehicle Excise Duty)

However, it's crucial to understand what these rates do not cover:

- Road, bridge, and tunnel tolls

- Parking fees

- Congestion charges

- Speeding fines, parking fines, or other road offences (these are penalties, not business expenses)

The good news for self-employed individuals is that while the mileage rates themselves don't cover these specific items, you can often claim them separately, depending on the method you choose for your mileage claims. This leads us to the two primary methods for self-employed mileage claims.

Choosing Your Method: Simplified Expenses vs. Actual Costs

For self-employed individuals, HMRC offers two distinct methods for claiming vehicle expenses: the Simplified Expenses method and the Actual Vehicle Costs method. Your choice can significantly impact the amount you claim and the level of record-keeping required.

The Simplified Expenses Method

This method is, as its name suggests, designed for simplicity. It allows you to claim a flat rate per mile for your business journeys, using the official HMRC mileage rates mentioned above. The benefit here is that you don't need to meticulously track every single vehicle-related expense like fuel receipts, repair invoices, or insurance premiums for the portion covered by the rate.

The Simplified Expenses method presumes that the per-mile rate covers all typical costs associated with owning and maintaining your vehicle for its business use. This means you won't claim separate deductions for fuel, servicing, or depreciation if you opt for this method.

However, a key advantage of the simplified method for self-employed individuals is that you can supplement your claim with additional expenses that are not covered by the flat rate. These include:

- Parking fees incurred on business trips

- Road, bridge, or tunnel tolls paid for business journeys

- Congestion charges for business travel

- The cost of travelling on other vehicles for business, such as bus or train tickets, if you use public transport for a portion of a business trip.

- Car hire fees for business purposes.

This makes the simplified method attractive for those who prefer less administrative burden, as it streamlines the process of claiming vehicle-related expenses.

The Actual Vehicle Costs Method

The Actual Vehicle Costs method offers a more granular approach. Instead of a flat rate per mile, you claim the precise costs associated with using your personal vehicle for business purposes. This requires you to keep detailed records and receipts for every eligible expense. This method can potentially lead to a higher claim if your actual vehicle running costs are substantial, perhaps due to high fuel consumption, frequent expensive repairs, or a high road tax category.

Under this method, you can claim for a wide range of specific expenses, including:

- Fuel costs

- Vehicle insurance premiums

- All repairs and maintenance

- Regular servicing costs

- Breakdown cover subscriptions

- Parking fees (which are also claimable under simplified, but here as part of the total vehicle costs)

- Vehicle licence fees (road tax)

- Depreciation of the vehicle (claimed through capital allowances)

The main challenge with this method arises if you use your vehicle for both business and personal driving. In such cases, you cannot claim 100% of all your vehicle expenses. Instead, you must accurately determine the percentage of your total mileage that was for business purposes throughout the year. You then claim only that percentage of your actual vehicle costs. For example, if 70% of your annual mileage was for business, you can claim 70% of your fuel, insurance, repairs, etc.

While more labour-intensive due to the need for meticulous record-keeping (every receipt, every invoice), the Actual Vehicle Costs method is worth considering if your vehicle expenses consistently exceed what you would claim using the simplified rates, especially if you have a high-mileage vehicle or significant maintenance costs.

Making Your Claim: Mileage Allowance Relief (MAR)

For self-employed individuals, claiming mileage from HMRC is done at tax time when you complete your Self Assessment tax return. The deduction you make for your business mileage is known as Mileage Allowance Relief (MAR). It effectively reduces your taxable profits, thereby lowering your overall tax liability.

To calculate your MAR, you'll need your total business mileage for the tax year. If you're using the Simplified Expenses method, you multiply your total business miles by the applicable HMRC mileage rates. If you're using the Actual Vehicle Costs method, you'll sum up all your relevant, apportioned expenses (e.g., 70% of fuel, 70% of insurance, etc.).

Regardless of the method chosen, the cornerstone of a successful claim is robust documentation. Without proper records, HMRC may disallow your claim, leading to potential penalties.

Meticulous Record-Keeping: Your Essential Guide

Whether you choose the simplified or actual costs method, maintaining comprehensive and accurate records of your business mileage is paramount. HMRC requires documented proof to substantiate any mileage claim. While an employer might set specific requirements for their employees, for self-employed individuals, adherence to HMRC's general requirements is non-negotiable.

According to HMRC, your mileage log should include the following details for each journey:

- The date of your journey.

- Whether it was a personal or business-related journey.

- The start and end addresses, including postcodes.

- The total number of miles driven for that specific journey.

For self-employed individuals, you will typically need a year's worth of this data to accurately calculate and claim your Mileage Allowance Relief at the end of the tax year. Modern mileage tracking apps can automate much of this process, using GPS to log trips and often categorising them automatically, ensuring your records are compliant and easily accessible for your Self Assessment.

Beyond the mileage log itself, if you opt for the Actual Vehicle Costs method, you must also diligently retain all receipts and invoices for fuel purchases, servicing, repairs, insurance, and any other vehicle-related expenses you wish to claim. These documents serve as direct evidence of your expenditure and are vital for justifying your claim if HMRC requests further information.

Comparison: Simplified Expenses vs. Actual Vehicle Costs

To help you decide which method is best for your self-employed business, here's a comparative overview:

| Feature | Simplified Expenses Method | Actual Vehicle Costs Method |

|---|---|---|

| Ease of Use | Generally simpler, less administrative burden. | More complex, requires meticulous record-keeping. |

| Record Keeping | Mileage log required; no need for individual fuel/repair receipts. | Detailed mileage log PLUS all receipts/invoices for vehicle expenses. |

| What it Covers | Flat rate covers fuel, maintenance, insurance, depreciation, road tax. | Specific costs like fuel, insurance, repairs, servicing, breakdown cover, depreciation, road tax. |

| Additional Claims | Can claim parking, tolls, congestion charges, and public transport fares separately. | All eligible costs are claimed as part of the vehicle expenses (including parking/tolls if business-related). |

| Potential Claim | Fixed by mileage rates. Good for average-cost vehicles. | Potentially higher if actual vehicle costs (fuel, repairs) are significantly above average. |

| Best For... | Individuals with lower vehicle running costs, or those prioritising simplicity. | Individuals with high vehicle running costs, or those who meticulously track all expenses. |

It's important to note that you generally choose one method for a vehicle and stick with it for that vehicle as long as you use it in your business. However, you can choose different methods for different vehicles or if you acquire a new vehicle.

Frequently Asked Questions (FAQs)

Q: Can I claim mileage for commuting from my home to my regular business premises?

A: No, HMRC considers regular journeys between your home and your permanent workplace as commuting, which is not a tax-deductible expense. Mileage can only be claimed for business trips, such as visiting clients, suppliers, or temporary workplaces.

Q: Are parking fines or speeding tickets covered by mileage claims?

A: Absolutely not. Fines and penalties, including parking fines and speeding tickets, are never tax-deductible expenses, regardless of whether they occurred during a business journey. They are considered personal liabilities and cannot be claimed.

Q: What if my actual vehicle expenses are significantly higher than the HMRC mileage rates?

A: If your actual costs for fuel, maintenance, and other vehicle-related expenses genuinely exceed what you would claim using the simplified HMRC mileage rates, then the Actual Vehicle Costs method might be more beneficial for you. This is often the case for high-mileage drivers, vehicles with poor fuel efficiency, or those that have incurred significant repair bills during the tax year. Remember, this method requires meticulous record-keeping of all receipts.

Q: Do I need to keep every fuel receipt if I use the Simplified Expenses method?

A: No, if you choose the Simplified Expenses method, you do not need to keep individual fuel receipts, nor receipts for servicing, maintenance, or insurance, as these costs are covered by the flat rate per mile. You only need to maintain an accurate mileage log and receipts for additional claims like parking, tolls, or congestion charges.

Q: How long should I keep my mileage records and receipts?

A: HMRC generally requires you to keep your business records, including mileage logs and expense receipts, for at least 5 years after the 31 January submission deadline for the relevant tax year. For example, for the 2024-2025 tax year (ending 5 April 2025), you should keep records until at least 31 January 2031.

Q: Can I switch between the Simplified Expenses and Actual Costs methods?

A: Once you start using a particular method for a specific vehicle, HMRC generally expects you to stick with it for as long as you use that vehicle in your business. However, if you acquire a new vehicle, you can choose the method for that new vehicle independently. It's usually advisable to select the method that best suits your expected costs and administrative capacity at the start of each tax year or when you first begin using a vehicle for business.

Understanding and correctly applying HMRC's rules for mileage claims can lead to substantial tax savings for self-employed individuals. By meticulously tracking your business miles and choosing the method that best aligns with your vehicle's usage and costs, you can ensure you're claiming everything you're legitimately entitled to. Don't underestimate the power of good record-keeping – it's your best ally when it comes to navigating your Self Assessment tax return and maximising your Mileage Allowance Relief.

If you want to read more articles similar to Mastering HMRC Mileage Claims for UK Self-Employed, you can visit the Taxis category.