01/08/2018

Navigating the world of business expenses can often feel like a complex journey, especially for self-employed taxi drivers in the UK. Understanding what you can claim to reduce your taxable income is paramount for financial efficiency. While many traditional business expenses require meticulous record-keeping of every receipt, HM Revenue & Customs (HMRC) introduced 'simplified expenses' to offer an alternative, particularly for vehicle costs. However, it's crucial to understand who qualifies and the specific nuances of these rules, especially if you drive a taxi.

The simplified expenses regime, specifically concerning vehicle costs, allows eligible businesses to use a fixed rate per business mile instead of tracking every single expenditure on their vehicle. This can significantly reduce the administrative burden of maintaining detailed records of fuel, servicing, and repairs. Introduced from the 2013-14 tax year onwards, this method aims to streamline the process for sole traders and partnerships. It's an optional approach, offering flexibility to businesses, whether they operate on a cash basis or not.

- Who Can Claim Simplified Mileage Expenses?

- The Mechanics of the Mileage Rate: What's Covered?

- Qualifying Journeys: The 'Wholly and Exclusively' Rule

- Mileage Rates at a Glance

- Simplified Expenses vs. Capital Allowances and Actual Costs

- Interaction with the Cash Basis

- Frequently Asked Questions for Taxi Drivers

- Can all taxi drivers use the simplified mileage rate?

- What records do I need to keep if I use the mileage rate?

- Can I switch between the mileage rate and claiming actual costs?

- Does the number of passengers affect the mileage rate I can claim?

- Are incidental expenses like tolls, congestion charges, and parking included in the mileage rate?

- What if my actual vehicle expenses are higher than what the mileage rate allows?

- Conclusion

Who Can Claim Simplified Mileage Expenses?

Not all taxi drivers can automatically benefit from the simplified mileage rate. The eligibility criteria are specific and vital to grasp:

- Sole Traders and Partnerships: This method is primarily available to sole traders and business partnerships, provided they do not have a corporate partner. This covers a large segment of the self-employed taxi driving community.

- Vehicle Type Exclusion: This is a critical point for taxi drivers. The fixed rate deduction covers cars, motorcycles, or goods vehicles. However, it explicitly excludes "cars designed for commercial use, for example black cabs or dual control driving instructor cars." This means if you operate a traditional London black cab or a similar purpose-built commercial taxi vehicle, you are unfortunately not eligible to use the simplified mileage rate for that vehicle. For such vehicles, you must revert to claiming the actual business proportion of your vehicle costs and potentially capital allowances.

- Consistency Rule: Once you choose to use the mileage rate basis for a particular vehicle, you must apply it consistently year after year for as long as that vehicle remains in your business. You cannot switch back and forth between the mileage rate and claiming actual expenditure or capital allowances for the same vehicle. A change in method is only permissible when you replace the vehicle.

Understanding these eligibility rules is the first step. If your vehicle falls within the excluded category, you will need to continue with traditional record-keeping for all vehicle-related expenses, ensuring you claim only the business proportion.

The Mechanics of the Mileage Rate: What's Covered?

The fixed mileage rate is designed to be comprehensive, covering a broad spectrum of vehicle-related costs. When you claim using this method, the rate is intended to encompass:

- Acquisition Costs: An element for the depreciation or cost of purchasing the vehicle.

- Ownership Costs: Such as Vehicle Excise Duty (VED).

- Hire or Leasing Costs: If you lease your vehicle.

- Running Costs: This is a significant part, including fuel, oil, servicing, and general repairs.

- Insurance: Your vehicle insurance premiums.

- MOT Costs: The annual cost of your vehicle's Ministry of Transport test.

Essentially, the mileage rate is an all-inclusive figure for the fundamental costs of having and operating your vehicle for business purposes.

What the Mileage Rate Does NOT Cover

While comprehensive, the simplified mileage rate does not cover every single expense associated with a business journey. There are specific incidental expenses that are not included in the flat rate and can, therefore, be claimed separately if they are incurred wholly and exclusively for business purposes:

- Tolls: Any charges incurred for using toll roads.

- Congestion Charges: Fees for entering congestion zones in cities like London.

- Parking Fees: Costs associated with parking your vehicle while on a business journey.

It is vital to keep accurate records for these separate expenses, as they can still be deducted from your profits.

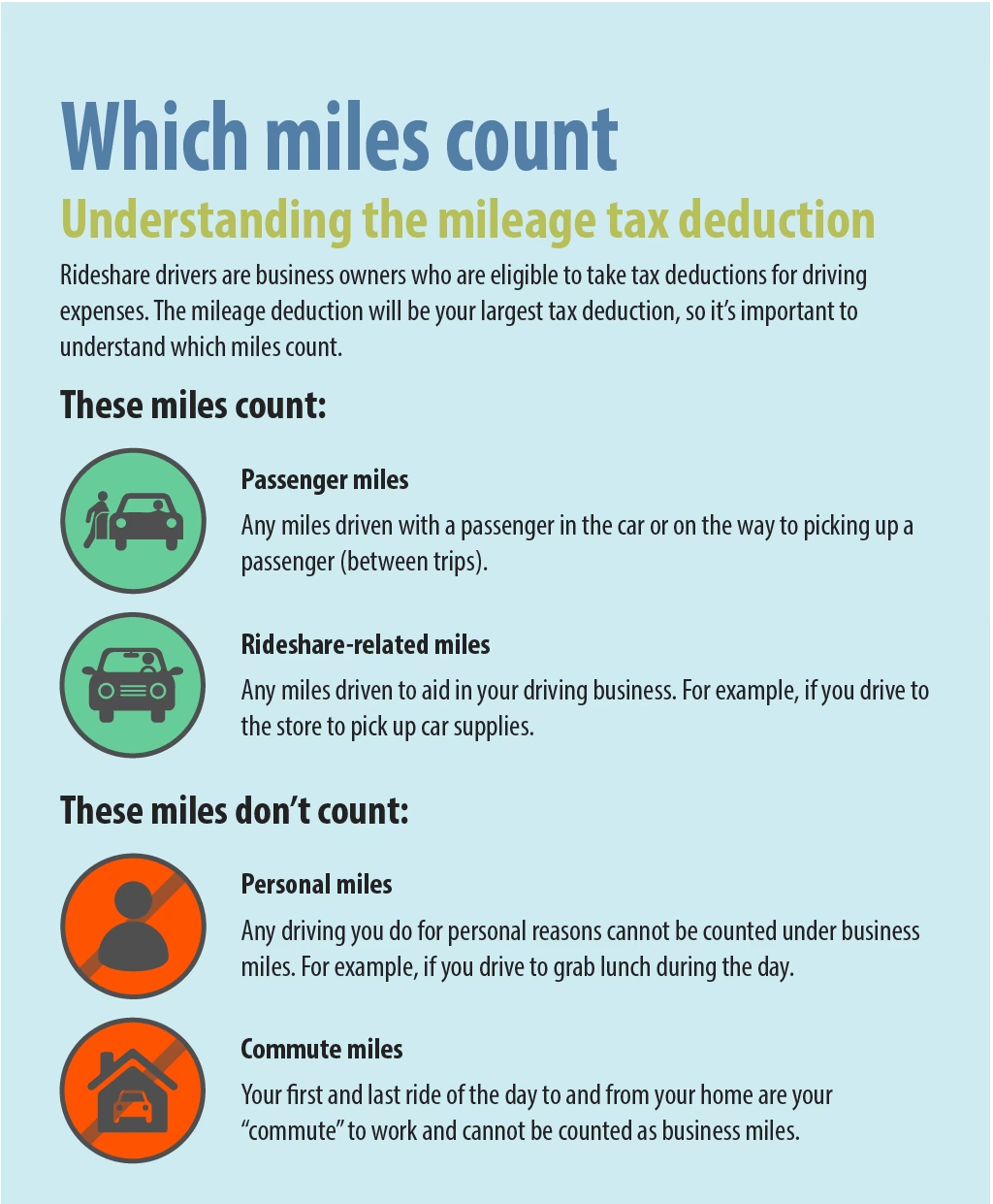

Qualifying Journeys: The 'Wholly and Exclusively' Rule

For any mileage to be claimed using the simplified rate, the journey, or any identifiable part of it, must be undertaken wholly and exclusively for business purposes. This is a fundamental principle of UK tax law for expense claims.

- Business Journeys: This includes trips to pick up fares, returning from a drop-off, travelling for vehicle maintenance directly related to your business, or visiting an accountant for business matters.

- Private Journeys: Travel from your home to your usual place of work (e.g., your first pick-up point if it's a regular starting location) is generally considered ordinary commuting and is not typically allowable. Journeys that serve both a business and a private purpose are also generally not claimable under this rule, unless a clear identifiable business portion can be separated.

To support your claim, maintaining a contemporaneous record of your business mileage is absolutely essential. This means logging your journeys as they happen, detailing the date, start and end points, purpose of the journey, and mileage covered. A simple logbook or a mileage tracking app can be invaluable for this.

Mileage Rates at a Glance

The rates per business mile that can be claimed are fixed by HMRC and apply regardless of the number of people in the vehicle. These rates are designed to factor in all the covered costs, including depreciation.

| Vehicle Type | Mileage Band | Flat Rate per Business Mile |

|---|---|---|

| Cars and Goods Vehicles | First 10,000 miles | 45p |

| Cars and Goods Vehicles | After 10,000 miles | 25p |

| Motorcycles | All miles | 24p |

It's important to note the tiered rate for cars and goods vehicles: the rate decreases significantly after the first 10,000 business miles in a tax year. This structure is designed to provide a higher relief for initial usage, accounting for the faster depreciation and higher fixed costs often incurred at the start of a vehicle's life in business.

Simplified Expenses vs. Capital Allowances and Actual Costs

The simplified mileage rate is an alternative, not an addition, to other forms of vehicle expense relief. This means you cannot 'double dip'.

- Capital Allowances: If you have ever claimed capital allowances in respect of a vehicle, you cannot then switch to using the mileage rate for that vehicle. This is because the mileage rate already incorporates an element for the depreciation of the vehicle. If you have claimed Capital Allowances, you must continue to claim the business proportion of the actual costs of running and maintaining the vehicle, alongside your Capital Allowances.

- Actual Costs: The simplified mileage rate is an alternative to keeping detailed records of your actual expenditure (fuel, servicing, insurance, etc.). If you choose the mileage rate, you forgo the ability to claim these actual costs for the covered items. This choice should be made carefully, considering which method would result in a greater deduction for your specific circumstances. For vehicles excluded from the mileage rate (like black cabs), claiming actual costs is the only option for vehicle expenses.

For many, the administrative simplicity of the mileage rate outweighs the potential for a slightly higher claim through actual costs, especially if their actual expenses are difficult to track or relatively low.

Interaction with the Cash Basis

For businesses that have elected to use the new cash basis for accounting – a simplified method of calculating profits where income and expenses are recognised when money is received or paid out, rather than when invoiced – the mileage rate can also be used.

- Cars: If you use the cash basis, you can use the mileage rate for cars, provided no Capital Allowances have previously been claimed on that specific vehicle.

- Goods Vehicles and Motorcycles: Under the cash basis rules, businesses can deduct the expenditure on acquiring goods vehicles and motorcycles (but not cars) in full as an expense in the year of purchase. If you have made such a deduction for a goods vehicle or motorcycle, you cannot then use the mileage rate for that vehicle. Instead, you can claim the business proportion of the actual costs of running and maintaining that specific vehicle.

This interaction highlights the importance of understanding the various accounting methods and their implications for expense claims.

Frequently Asked Questions for Taxi Drivers

Can all taxi drivers use the simplified mileage rate?

No. While many self-employed taxi drivers (sole traders or partnerships) can use it, vehicles specifically "designed for commercial use, for example black cabs or dual control driving instructor cars," are explicitly excluded. If you drive a traditional black cab, you must claim actual expenses for your vehicle.

What records do I need to keep if I use the mileage rate?

You must keep a contemporaneous record of all your business mileage. This should include dates, start and end locations, purpose of the journey, and the total business miles travelled. This record is crucial for supporting your claim in the event of an HMRC enquiry.

Can I switch between the mileage rate and claiming actual costs?

For a specific vehicle, once you adopt the mileage rate, you must stick with it consistently from year to year. You can only change to or from an 'actual' basis when that vehicle is replaced with a new one in your business.

Does the number of passengers affect the mileage rate I can claim?

No, the number of people in the vehicle does not affect the flat rates per business mile that can be claimed. The rates are fixed based on the vehicle type and mileage band.

Are incidental expenses like tolls, congestion charges, and parking included in the mileage rate?

No, these specific incidental expenses are not included in the flat mileage rate. However, if they are incurred solely for business purposes, you can claim them as separate allowable deductions in addition to your mileage claim. Remember to keep receipts for these.

What if my actual vehicle expenses are higher than what the mileage rate allows?

The simplified mileage rate is an optional alternative. If you believe your actual, properly documented business vehicle expenses (fuel, repairs, insurance, etc.) would result in a higher deduction than the simplified mileage rate, and you are eligible to claim actual costs (i.e., you haven't claimed Capital Allowances on that vehicle and it's not a new vehicle where you've chosen mileage), you can choose to claim actual costs instead. However, this requires diligent record-keeping of every expense.

Conclusion

For many self-employed taxi drivers operating standard cars, the simplified expenses method for mileage offers a practical and less burdensome way to claim vehicle costs. It streamlines accounting by removing the need to track every fuel receipt or repair bill, replacing it with a straightforward per-mile deduction. However, the crucial exclusion of purpose-built commercial vehicles like black cabs means that not all taxi drivers can utilise this simplified approach. Regardless of whether you opt for the simplified mileage rate or choose to claim actual expenses, maintaining accurate and contemporaneous records of your business journeys and any separately claimable incidental expenses remains paramount. Understanding these rules ensures you remain compliant with HMRC and effectively minimise your tax liability, allowing you to focus more on driving your business forward.

If you want to read more articles similar to Taxi Driver Expenses: Simplified Mileage Claims Unpacked, you can visit the Taxis category.