11/12/2020

It's a common question for many in the UK: "Do I pay tax if my income is more than my personal allowance?" The straightforward answer is yes, if your total annual income exceeds your Personal Allowance, you will be liable to pay Income Tax. This fundamental concept underpins the UK's tax system, ensuring that those with higher earnings contribute more towards public services. But understanding the nuances of what constitutes taxable income, how your Personal Allowance works, and the specific rules around savings can be complex. This article aims to demystify these elements, providing you with the clarity needed to manage your tax obligations effectively.

Understanding Your Personal Allowance

Your Personal Allowance is a crucial element of the UK tax system. It represents the amount of income you can earn each tax year without having to pay any Income Tax on it. For the 2024/25 tax year, the standard Personal Allowance is £12,570. This allowance is effectively deducted from your total income before Income Tax is calculated. HMRC (His Majesty's Revenue and Customs) collects Income Tax on behalf of the government, and these funds are vital for financing essential public services such as the NHS, education, and the welfare system, as well as investing in infrastructure like roads and housing.

It's important to note that your Personal Allowance can be affected by various factors, including your income level and specific circumstances. For instance, for every £2 your income exceeds £100,000, your Personal Allowance is reduced by £1. If your income reaches £125,140 or more, you will not be entitled to a Personal Allowance.

What Income is Subject to Tax?

The scope of income that can be subject to Income Tax is broad and encompasses more than just your salary from employment. To determine if you need to pay tax, you must consider your total annual income, which can include a variety of sources:

- State Pension: Both the basic State Pension and the new State Pension are taxable.

- Additional State Pension: Any additional amounts received from the State Pension scheme are also included.

- Private Pensions: Income from workplace pensions or personal pensions is taxable. However, you typically have the option to take a portion of your private pension as a tax-free lump sum, up to certain allowances.

- Earnings from Employment or Self-Employment: This is often the most significant portion of income for many individuals.

- Taxable Benefits: Certain benefits provided by an employer, such as company car benefits or health insurance, may be taxable.

- Other Income: This category is wide-ranging and can include income from investments (like dividends), rental income from properties, and interest earned on savings.

If your combined income from all these sources surpasses your Personal Allowance, you will be required to pay Income Tax on the amount exceeding that threshold.

Tax on Pension Income: A Closer Look

When it comes to pensions, understanding your tax obligations is particularly important. To ascertain if you need to pay tax on your pension, you'll need to gather specific information:

- Whether you receive a State Pension, a private pension, or both.

- The total amount of State Pension and private pension income you expect to receive in the current tax year (6 April to 5 April).

- The amount of any other taxable income you anticipate, such as earnings from employment or state benefits.

There are online tools available that can help you check if you need to pay tax on your pension. However, these tools may not be suitable if you receive foreign income, or if you are eligible for specific allowances like the Marriage Allowance or Blind Person's Allowance.

Taking Pension as a Lump Sum

If you decide to take some or all of your private pension as a lump sum, tax implications arise. You will pay Income Tax on any part of the lump sum that exceeds your lump sum allowance and your lump sum and death benefit allowance. It's essential to be aware of these allowances, as exceeding them can result in a tax charge. In some cases, particularly if you withdraw a large amount from a private pension, you might have to pay Income Tax at a higher rate, and you may owe additional tax at the end of the tax year. It's advisable to check your specific lump sum allowances to understand your potential tax liability.

Inheriting a Pension

The rules surrounding the taxation of inherited pensions differ significantly depending on whether the pension is from the State Pension or a private pension scheme. If someone inherits your pension, different tax regulations will apply to the beneficiary.

Tax on Savings Interest

Many people earn interest on their savings, and understanding how this is taxed is crucial. The UK tax system offers a starting rate for savings, which is an additional £5,000 added to your Standard Personal Allowance. For the 2024/25 tax year, this means you could potentially earn up to £17,570 (£12,570 Standard Personal Allowance + £5,000 starting rate) in total income and still pay no tax on the savings interest earned within that £5,000 portion, provided your total income doesn't exceed £17,570.

However, there's a crucial interaction: for every £1 of income you earn above your Standard Personal Allowance (£12,570), your starting rate for savings is reduced by £1. This means that if your total income (from wages, pensions, etc.) exceeds £17,570, you will not qualify for the starting rate for savings. In such cases, the interest you earn above your Personal Allowance will be taxed at your marginal rate of Income Tax.

Beyond the starting rate for savings, there are also tax-free allowances for savings interest:

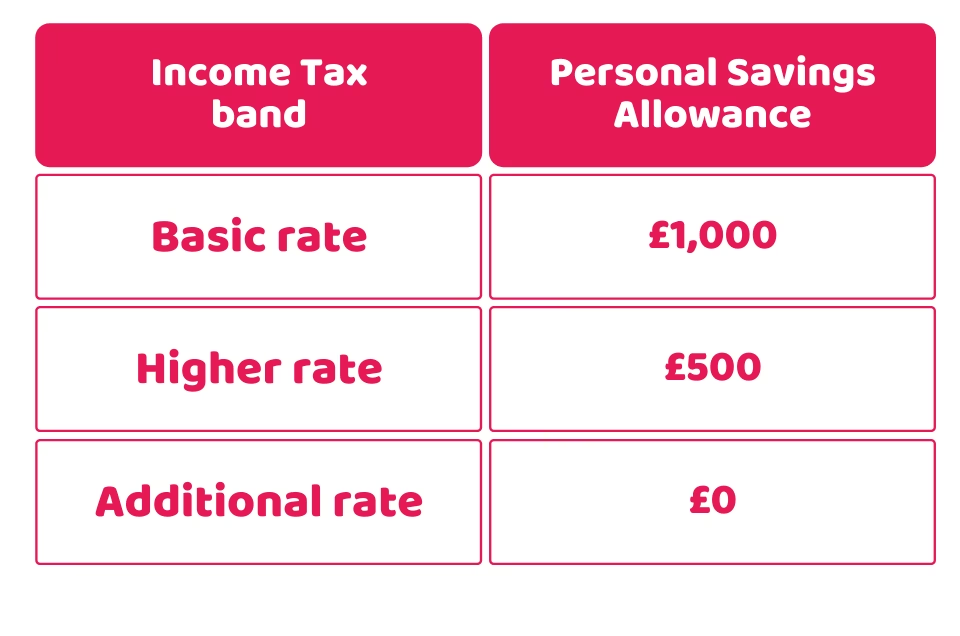

- Personal Savings Allowance (PSA): Basic-rate taxpayers can earn up to £1,000 in savings interest tax-free each year.

- Higher-rate taxpayers: Can earn up to £500 in savings interest tax-free each year.

It's important to note that savings held in tax-free accounts, such as Individual Savings Accounts (ISAs), do not count towards these allowances, as the interest earned within an ISA is already tax-free.

How HMRC Collects Tax on Savings:

If you exceed your savings interest allowance and are employed or receive a pension, HMRC may adjust your tax code to automatically collect the tax due. If you usually complete a Self Assessment tax return, you should report your savings interest earnings there. Alternatively, your bank or building society will report the interest you've received to HMRC at the end of the tax year. Resources like MoneyHelper offer more in-depth information on how tax on savings works.

Taxable Income vs. Non-Taxable Income

It's helpful to understand that not all income is subject to Income Tax. While the list of taxable income sources is extensive, some forms of income are exempt. For example, certain state benefits, such as Universal Credit or Attendance Allowance, are typically not taxable. Similarly, income from certain government-backed schemes or specific grants may also be tax-exempt. Always refer to official HMRC guidance or seek professional advice if you are unsure about the taxability of a particular income source.

Key Takeaways and Actionable Advice

Understanding your tax obligations in the UK revolves around the concept of your Personal Allowance and the total income you receive. Here's a summary of key points and advice:

- Know Your Allowance: Be aware of your standard Personal Allowance and any factors that might affect it.

- Track All Income: Keep a record of all your income sources, including earnings, pensions, benefits, and savings interest.

- Utilise Tax-Efficient Accounts: Make the most of tax-free savings vehicles like ISAs to minimise your tax liability on savings interest.

- Understand Pension Rules: If you have private pensions, familiarise yourself with the rules around lump sums and any associated tax implications.

- Seek Guidance: If your financial situation is complex, or you are unsure about your tax responsibilities, consult with HMRC or a qualified financial advisor.

By staying informed and organised, you can navigate the UK's Income Tax system with confidence, ensuring you meet your obligations while making the most of available tax reliefs and allowances.

Frequently Asked Questions

Q1: What happens if my income goes slightly over my Personal Allowance?

A1: If your total income exceeds your Personal Allowance, you will pay Income Tax on the amount that is over the allowance. For example, if your income is £13,000 and your Personal Allowance is £12,570, you will pay tax on £430 (£13,000 - £12,570).

Q2: Can I claim my Personal Allowance if I have a private pension?

A2: Yes, your Personal Allowance applies to all your taxable income, including income from a private pension, as long as your total income doesn't exceed the threshold where your allowance is reduced or eliminated.

Q3: Is all interest from my savings taxable?

A3: No, you have a Personal Savings Allowance (£1,000 for basic-rate taxpayers, £500 for higher-rate taxpayers). Interest earned up to this amount is tax-free. Additionally, the starting rate for savings allows you to earn up to £5,000 in interest tax-free, provided your total income is within certain limits.

Q4: Do I need to tell HMRC if my income changes?

A4: It's generally advisable to inform HMRC of any significant changes to your income, as this can affect your tax code and the amount of tax you pay. If your income increases significantly, you may need to pay more tax, and if it decreases, you might be due a refund.

Q5: What is the difference between Personal Allowance and tax-free savings allowance?

A5: The Personal Allowance is the amount of income you can earn from any source before paying Income Tax. The tax-free savings allowance (Personal Savings Allowance) specifically relates to the interest you earn on your savings and is a separate tax-free amount for that specific type of income.

If you want to read more articles similar to Navigating UK Income Tax: Your Personal Allowance Explained, you can visit the Taxis category.